Advertisement

JW (Cayman) Therapeutics Co. Ltd (HKG:2126) Screens Well But There Might Be A Catch

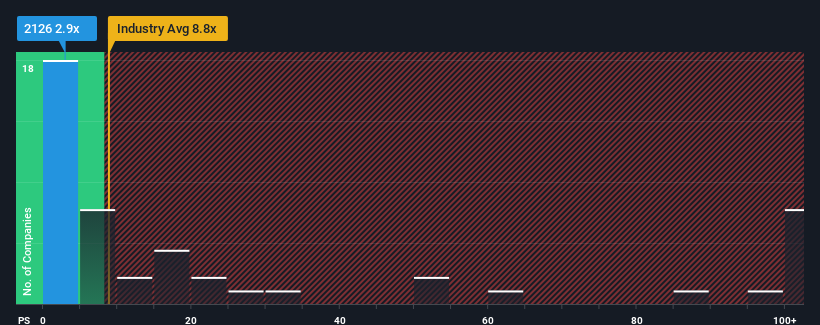

You may think that with a price-to-sales (or "P/S") ratio of 2.9x JW (Cayman) Therapeutics Co. Ltd (HKG:2126) is definitely a stock worth checking out, seeing as almost half of all the Biotechs companies in Hong Kong have P/S ratios greater than 8.8x and even P/S above 53x aren't out of the ordinary. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so limited.

View our latest analysis for JW (Cayman) Therapeutics

What Does JW (Cayman) Therapeutics' P/S Mean For Shareholders?

JW (Cayman) Therapeutics could be doing better as it's been growing revenue less than most other companies lately. Perhaps the market is expecting the current trend of poor revenue growth to continue, which has kept the P/S suppressed. If you still like the company, you'd be hoping revenue doesn't get any worse and that you could pick up some stock while it's out of favour.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on JW (Cayman) Therapeutics.What Are Revenue Growth Metrics Telling Us About The Low P/S?

The only time you'd be truly comfortable seeing a P/S as depressed as JW (Cayman) Therapeutics' is when the company's growth is on track to lag the industry decidedly.

Retrospectively, the last year delivered a decent 3.3% gain to the company's revenues. However, due to its less than impressive performance prior to this period, revenue growth is practically non-existent over the last three years overall. Therefore, it's fair to say that revenue growth has been inconsistent recently for the company.

Shifting to the future, estimates from the dual analysts covering the company suggest revenue should grow by 65% each year over the next three years. Meanwhile, the rest of the industry is forecast to only expand by 52% per annum, which is noticeably less attractive.

With this in consideration, we find it intriguing that JW (Cayman) Therapeutics' P/S sits behind most of its industry peers. Apparently some shareholders are doubtful of the forecasts and have been accepting significantly lower selling prices.

The Bottom Line On JW (Cayman) Therapeutics' P/S

Typically, we'd caution against reading too much into price-to-sales ratios when settling on investment decisions, though it can reveal plenty about what other market participants think about the company.

To us, it seems JW (Cayman) Therapeutics currently trades on a significantly depressed P/S given its forecasted revenue growth is higher than the rest of its industry. There could be some major risk factors that are placing downward pressure on the P/S ratio. While the possibility of the share price plunging seems unlikely due to the high growth forecasted for the company, the market does appear to have some hesitation.

Having said that, be aware JW (Cayman) Therapeutics is showing 3 warning signs in our investment analysis, and 1 of those shouldn't be ignored.

If you're unsure about the strength of JW (Cayman) Therapeutics' business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2126

JW (Cayman) Therapeutics

A clinical stage cell therapy company, engages in the research and development, manufacturing, and marketing of anti-tumor drugs in the People’s Republic of China.

Undervalued with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.2% undervalued

TO

Community Contributor