Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. As with many other companies Genscript Biotech Corporation (HKG:1548) makes use of debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. While that is not too common, we often do see indebted companies permanently diluting shareholders because lenders force them to raise capital at a distressed price. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Genscript Biotech

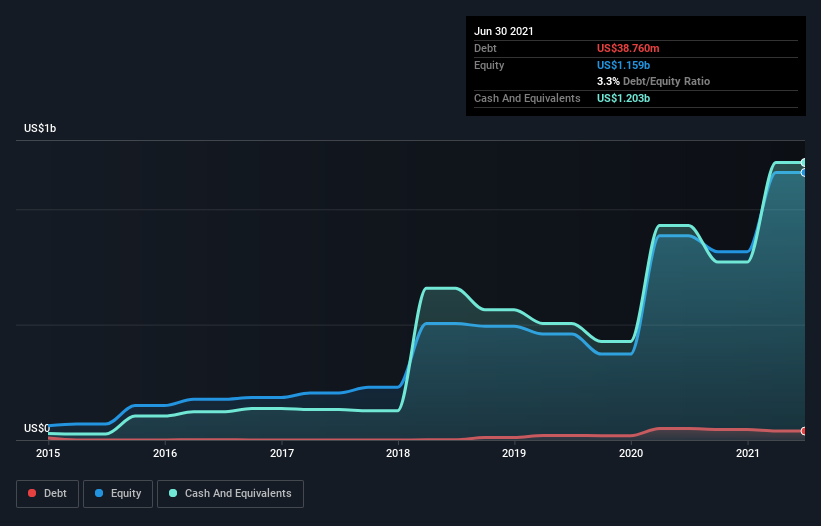

How Much Debt Does Genscript Biotech Carry?

The image below, which you can click on for greater detail, shows that Genscript Biotech had debt of US$38.8m at the end of June 2021, a reduction from US$50.1m over a year. But it also has US$1.20b in cash to offset that, meaning it has US$1.16b net cash.

A Look At Genscript Biotech's Liabilities

We can see from the most recent balance sheet that Genscript Biotech had liabilities of US$421.3m falling due within a year, and liabilities of US$307.4m due beyond that. Offsetting this, it had US$1.20b in cash and US$94.8m in receivables that were due within 12 months. So it can boast US$568.5m more liquid assets than total liabilities.

This short term liquidity is a sign that Genscript Biotech could probably pay off its debt with ease, as its balance sheet is far from stretched. Simply put, the fact that Genscript Biotech has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Genscript Biotech can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

In the last year Genscript Biotech wasn't profitable at an EBIT level, but managed to grow its revenue by 43%, to US$454m. Shareholders probably have their fingers crossed that it can grow its way to profits.

So How Risky Is Genscript Biotech?

Statistically speaking companies that lose money are riskier than those that make money. And in the last year Genscript Biotech had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of US$256m and booked a US$183m accounting loss. With only US$1.16b on the balance sheet, it would appear that its going to need to raise capital again soon. With very solid revenue growth in the last year, Genscript Biotech may be on a path to profitability. Pre-profit companies are often risky, but they can also offer great rewards. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. For example, we've discovered 3 warning signs for Genscript Biotech that you should be aware of before investing here.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1548

Genscript Biotech

An investment holding company, engages in the manufacture and sale of life science research products and services in the United States of America, Europe, Mainland China, Europe, Asia Pacific, and internationally.

Reasonable growth potential with adequate balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|35.7% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|20.5% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|25.2% overvalued

DA

Community Contributor