Advertisement

- Hong Kong

- /

- Entertainment

- /

- SEHK:1132

Orange Sky Golden Harvest Entertainment (Holdings) (HKG:1132) Has Debt But No Earnings; Should You Worry?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Orange Sky Golden Harvest Entertainment (Holdings) Limited (HKG:1132) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt is a tool to help businesses grow, but if a business is incapable of paying off its lenders, then it exists at their mercy. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

What Is Orange Sky Golden Harvest Entertainment (Holdings)'s Debt?

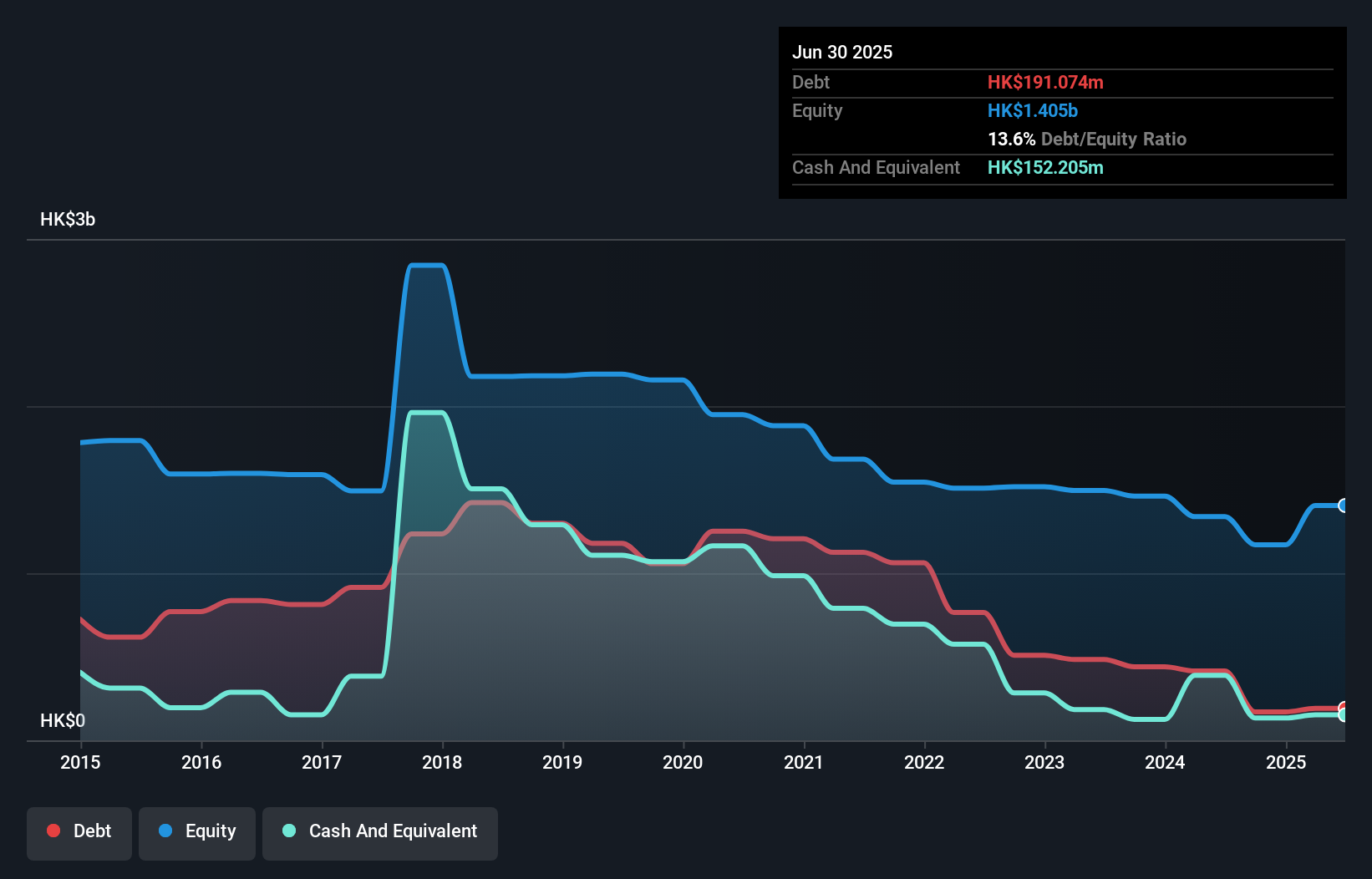

As you can see below, Orange Sky Golden Harvest Entertainment (Holdings) had HK$191.1m of debt at June 2025, down from HK$414.9m a year prior. However, it also had HK$152.2m in cash, and so its net debt is HK$38.9m.

How Strong Is Orange Sky Golden Harvest Entertainment (Holdings)'s Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Orange Sky Golden Harvest Entertainment (Holdings) had liabilities of HK$443.3m due within 12 months and liabilities of HK$248.5m due beyond that. On the other hand, it had cash of HK$152.2m and HK$53.7m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$485.9m.

This deficit casts a shadow over the HK$201.6m company, like a colossus towering over mere mortals. So we'd watch its balance sheet closely, without a doubt. At the end of the day, Orange Sky Golden Harvest Entertainment (Holdings) would probably need a major re-capitalization if its creditors were to demand repayment. The balance sheet is clearly the area to focus on when you are analysing debt. But you can't view debt in total isolation; since Orange Sky Golden Harvest Entertainment (Holdings) will need earnings to service that debt. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

See our latest analysis for Orange Sky Golden Harvest Entertainment (Holdings)

In the last year Orange Sky Golden Harvest Entertainment (Holdings) had a loss before interest and tax, and actually shrunk its revenue by 5.0%, to HK$728m. We would much prefer see growth.

Caveat Emptor

Importantly, Orange Sky Golden Harvest Entertainment (Holdings) had an earnings before interest and tax (EBIT) loss over the last year. Its EBIT loss was a whopping HK$57m. When we look at that alongside the significant liabilities, we're not particularly confident about the company. It would need to improve its operations quickly for us to be interested in it. It's fair to say the loss of HK$14m didn't encourage us either; we'd like to see a profit. And until that time we think this is a risky stock. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Case in point: We've spotted 2 warning signs for Orange Sky Golden Harvest Entertainment (Holdings) you should be aware of.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1132

Orange Sky Golden Harvest Entertainment (Holdings)

An investment holding company, operates as an integrated film entertainment company in Hong Kong, Mainland China, Singapore, and Taiwan.

Excellent balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|10.8% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|22.0% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|3.8% overvalued

LI

Community Contributor