Advertisement

- Hong Kong

- /

- Metals and Mining

- /

- SEHK:826

We Think Tiangong International (HKG:826) Is Taking Some Risk With Its Debt

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Tiangong International Company Limited (HKG:826) makes use of debt. But is this debt a concern to shareholders?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for Tiangong International

What Is Tiangong International's Debt?

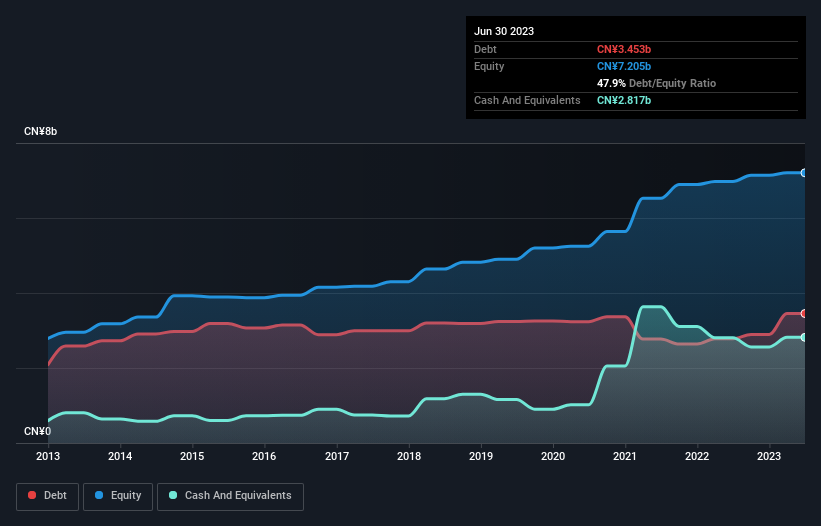

You can click the graphic below for the historical numbers, but it shows that as of June 2023 Tiangong International had CN¥3.45b of debt, an increase on CN¥2.78b, over one year. On the flip side, it has CN¥2.82b in cash leading to net debt of about CN¥635.6m.

How Healthy Is Tiangong International's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Tiangong International had liabilities of CN¥6.30b due within 12 months and liabilities of CN¥845.7m due beyond that. On the other hand, it had cash of CN¥2.82b and CN¥2.85b worth of receivables due within a year. So its liabilities total CN¥1.48b more than the combination of its cash and short-term receivables.

Tiangong International has a market capitalization of CN¥6.06b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). Thus we consider debt relative to earnings both with and without depreciation and amortization expenses.

While Tiangong International's low debt to EBITDA ratio of 0.79 suggests only modest use of debt, the fact that EBIT only covered the interest expense by 3.2 times last year does give us pause. So we'd recommend keeping a close eye on the impact financing costs are having on the business. Importantly, Tiangong International's EBIT fell a jaw-dropping 44% in the last twelve months. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Tiangong International's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Tiangong International's free cash flow amounted to 22% of its EBIT, less than we'd expect. That's not great, when it comes to paying down debt.

Our View

Mulling over Tiangong International's attempt at (not) growing its EBIT, we're certainly not enthusiastic. But at least it's pretty decent at managing its debt, based on its EBITDA,; that's encouraging. Looking at the balance sheet and taking into account all these factors, we do believe that debt is making Tiangong International stock a bit risky. That's not necessarily a bad thing, but we'd generally feel more comfortable with less leverage. Given our hesitation about the stock, it would be good to know if Tiangong International insiders have sold any shares recently. You click here to find out if insiders have sold recently.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Tiangong International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:826

Tiangong International

Manufactures and sells alloy steel, cutting tools, titanium alloys, and related products.

High growth potential with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

100% Patient Improvement in trial puts this $16M Biotech on the radar

Fair Value US$5.30|69.8% undervalued

JO

Community Contributor

Exxon Mobil's 17.5% Upside Promises Industry-Leading Returns in Energy Transition

Fair Value US$132.00|15.0% undervalued

HE

Community Contributor

NHC Analysis: Quality at a Good Price. A Golden Opportunity?

Fair Value US$179.80|36.1% undervalued

DA

Community Contributor

Product Refresh And Global Expansion Will Empower Future Market Leadership

Fair Value US$202.60|21.1% undervalued

AN

Based on Analyst Price Targets