Advertisement

- Hong Kong

- /

- Metals and Mining

- /

- SEHK:826

Should You Be Impressed By Tiangong International's (HKG:826) Returns on Capital?

Did you know there are some financial metrics that can provide clues of a potential multi-bagger? Firstly, we'd want to identify a growing return on capital employed (ROCE) and then alongside that, an ever-increasing base of capital employed. This shows us that it's a compounding machine, able to continually reinvest its earnings back into the business and generate higher returns. With that in mind, the ROCE of Tiangong International (HKG:826) looks decent, right now, so lets see what the trend of returns can tell us.

Return On Capital Employed (ROCE): What is it?

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. To calculate this metric for Tiangong International, this is the formula:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

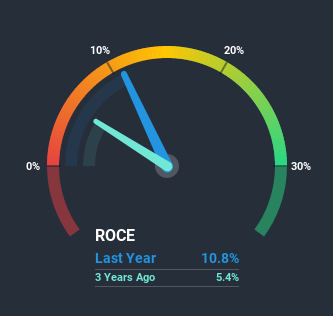

0.11 = CN¥667m ÷ (CN¥10b - CN¥4.2b) (Based on the trailing twelve months to June 2020).

Therefore, Tiangong International has an ROCE of 11%. In absolute terms, that's a satisfactory return, but compared to the Metals and Mining industry average of 7.5% it's much better.

View our latest analysis for Tiangong International

In the above chart we have measured Tiangong International's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free report on analyst forecasts for the company.

How Are Returns Trending?

The trend of ROCE doesn't stand out much, but returns on a whole are decent. The company has consistently earned 11% for the last five years, and the capital employed within the business has risen 46% in that time. Since 11% is a moderate ROCE though, it's good to see a business can continue to reinvest at these decent rates of return. Over long periods of time, returns like these might not be too exciting, but with consistency they can pay off in terms of share price returns.

On a side note, Tiangong International has done well to reduce current liabilities to 41% of total assets over the last five years. Effectively suppliers now fund less of the business, which can lower some elements of risk. Although because current liabilities are still 41%, some of that risk is still prevalent.

The Bottom Line

In the end, Tiangong International has proven its ability to adequately reinvest capital at good rates of return. And long term investors would be thrilled with the 646% return they've received over the last five years. So even though the stock might be more "expensive" than it was before, we think the strong fundamentals warrant this stock for further research.

If you'd like to know more about Tiangong International, we've spotted 2 warning signs, and 1 of them is concerning.

While Tiangong International isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

When trading Tiangong International or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

Valuation is complex, but we're here to simplify it.

Discover if Tiangong International might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisThis article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:826

Tiangong International

Manufactures and sells alloy steel, cutting tools, titanium alloys, and related products in the People’s Republic of China, North America, Europe, other Asian countries, and internationally.

Excellent balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor