- Taiwan

- /

- Electronic Equipment and Components

- /

- TWSE:2368

Asian Value Stocks: Three Companies That May Be Trading At A Discount

Reviewed by Simply Wall St

As global markets navigate a landscape marked by trade negotiations and economic uncertainty, Asian equities have shown resilience, with key indices in China and Japan posting gains amid positive sentiment from trade discussions. In this context, identifying undervalued stocks can be particularly appealing for investors seeking opportunities to capitalize on market inefficiencies.

Top 10 Undervalued Stocks Based On Cash Flows In Asia

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| Aidma Holdings (TSE:7373) | ¥1893.00 | ¥3727.32 | 49.2% |

| Shenzhen KSTAR Science and Technology (SZSE:002518) | CN¥23.12 | CN¥45.45 | 49.1% |

| Alexander Marine (TWSE:8478) | NT$148.50 | NT$291.28 | 49% |

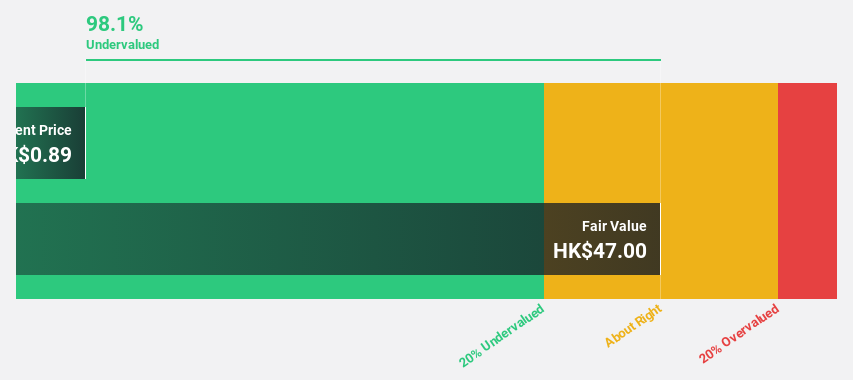

| Lingbao Gold Group (SEHK:3330) | HK$9.44 | HK$18.21 | 48.1% |

| Newborn Town (SEHK:9911) | HK$8.39 | HK$16.46 | 49% |

| GEM (SZSE:002340) | CN¥6.21 | CN¥12.14 | 48.8% |

| World Fitness Services (TWSE:2762) | NT$82.70 | NT$164.43 | 49.7% |

| Seegene (KOSDAQ:A096530) | ₩27250.00 | ₩52999.15 | 48.6% |

| Bloks Group (SEHK:325) | HK$129.60 | HK$255.66 | 49.3% |

| BrightGene Bio-Medical Technology (SHSE:688166) | CN¥50.36 | CN¥98.57 | 48.9% |

Underneath we present a selection of stocks filtered out by our screen.

Lingbao Gold Group (SEHK:3330)

Overview: Lingbao Gold Group Company Ltd. operates in the mining, processing, smelting, refining, and sale of gold products in China and has a market capitalization of approximately HK$12.15 billion.

Operations: The company's revenue primarily comes from its smelting operations, which generated CN¥12.04 billion, followed by mining activities in the People's Republic of China at CN¥2.31 billion, with additional contributions from mining in the Kyrgyz Republic and retailing at CN¥257.32 million and CN¥8.53 million respectively.

Estimated Discount To Fair Value: 48.1%

Lingbao Gold Group is trading at a significant discount to its estimated fair value, presenting an opportunity for investors focused on cash flow valuation. The company reported strong earnings growth, with net income reaching RMB 698 million in 2024, driven by increased gold output and improved operational efficiency. Despite high debt levels and recent share price volatility, its revenue is expected to grow faster than the Hong Kong market average.

- Our comprehensive growth report raises the possibility that Lingbao Gold Group is poised for substantial financial growth.

- Click here and access our complete balance sheet health report to understand the dynamics of Lingbao Gold Group.

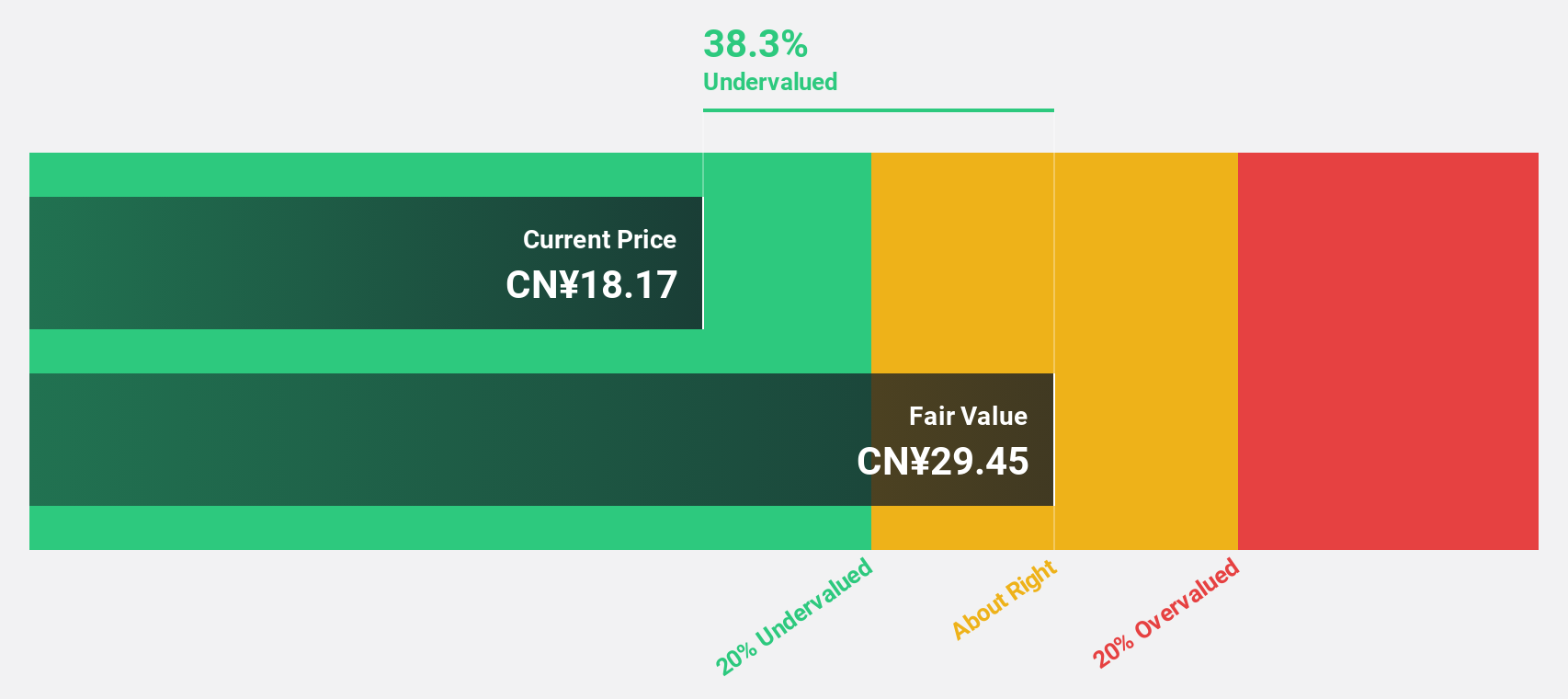

MeHow Innovative (SZSE:301363)

Overview: MeHow Innovative Ltd. specializes in the design, development, manufacturing, and sale of precision medical device components and products both in China and internationally, with a market cap of CN¥10.24 billion.

Operations: The company's revenue is derived from its operations in the design, development, manufacturing, and sale of precision medical device components and products across domestic and international markets.

Estimated Discount To Fair Value: 32.6%

MeHow Innovative is trading at a significant 32.6% discount to its estimated fair value of CN¥37.57, highlighting potential undervaluation based on cash flows. The company's earnings have grown by 36% over the past year, with future revenue and earnings expected to grow faster than the Chinese market averages at 22.1% and 23.61% per year, respectively. Despite this growth, recent quarterly results showed a decline in net income compared to the previous year.

- In light of our recent growth report, it seems possible that MeHow Innovative's financial performance will exceed current levels.

- Navigate through the intricacies of MeHow Innovative with our comprehensive financial health report here.

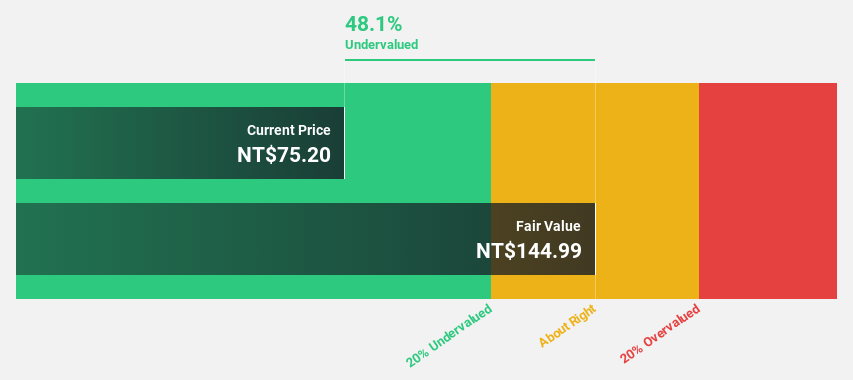

Gold Circuit Electronics (TWSE:2368)

Overview: Gold Circuit Electronics Ltd. is a Taiwanese company that designs, manufactures, processes, and distributes multilayer printed circuit boards with a market cap of NT$109.99 billion.

Operations: The company generates revenue of NT$38.95 billion from its operations in the manufacturing and sales of printed circuit boards.

Estimated Discount To Fair Value: 38.6%

Gold Circuit Electronics is trading at a 38.6% discount to its fair value of NT$368.17, indicating potential undervaluation based on cash flows. Earnings grew by 59.1% last year, with future earnings expected to grow significantly faster than the Taiwan market average at 21.9% per year. However, the dividend yield of 2.65% is not well covered by free cash flows, and the stock has experienced high volatility recently despite strong financial performance in 2024.

- Upon reviewing our latest growth report, Gold Circuit Electronics' projected financial performance appears quite optimistic.

- Click to explore a detailed breakdown of our findings in Gold Circuit Electronics' balance sheet health report.

Seize The Opportunity

- Reveal the 270 hidden gems among our Undervalued Asian Stocks Based On Cash Flows screener with a single click here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Seeking Other Investments?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TWSE:2368

Gold Circuit Electronics

Designs, manufactures, processes, and distributes multilayer printed circuit boards in Taiwan.

Flawless balance sheet with high growth potential.

Similar Companies

Market Insights

Community Narratives