Stock Analysis

- Hong Kong

- /

- Food and Staples Retail

- /

- SEHK:241

SEHK Growth Companies With High Insider Ownership And Up To 35% Earnings Growth

Reviewed by Simply Wall St

Amidst a backdrop of global economic fluctuations and mixed market signals, the Hong Kong market has shown resilience with the Hang Seng Index marking a modest gain in a holiday-shortened week. This stability offers an intriguing environment for investors interested in growth companies with high insider ownership, which can signal strong confidence in the company's future from those who know it best.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| iDreamSky Technology Holdings (SEHK:1119) | 20.2% | 104.1% |

| Pacific Textiles Holdings (SEHK:1382) | 11.2% | 37.7% |

| Fenbi (SEHK:2469) | 32.8% | 43% |

| Tian Tu Capital (SEHK:1973) | 34% | 70.5% |

| Adicon Holdings (SEHK:9860) | 22.4% | 28.3% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 15% | 73.4% |

| Zylox-Tonbridge Medical Technology (SEHK:2190) | 18.7% | 79.3% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 13.9% | 100.1% |

| Ocumension Therapeutics (SEHK:1477) | 23.1% | 93.7% |

| Beijing Airdoc Technology (SEHK:2251) | 28.7% | 83.9% |

Here we highlight a subset of our preferred stocks from the screener.

BYD (SEHK:1211)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: BYD Company Limited operates in the automobile and battery sectors across China, Hong Kong, Macau, Taiwan, and internationally, with a market capitalization of approximately HK$749.77 billion.

Operations: The company generates revenue primarily from its automobile and battery sectors across various regions including China, Hong Kong, Macau, Taiwan, and internationally.

Insider Ownership: 30.1%

Earnings Growth Forecast: 14.9% p.a.

BYD, a growth-oriented company with significant insider ownership in Hong Kong, is trading at 48.8% below its estimated fair value, indicating potential undervaluation. While its revenue growth of 13.9% per year outpaces the Hong Kong market average of 7.7%, its earnings growth forecast at 14.9% annually is robust but not exceptional compared to high-growth benchmarks. Recent substantial increases in production and sales volumes highlight operational scalability and market penetration, supporting a positive outlook despite slower-than-ideal revenue acceleration rates.

- Click here and access our complete growth analysis report to understand the dynamics of BYD.

- According our valuation report, there's an indication that BYD's share price might be on the expensive side.

Dongyue Group (SEHK:189)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Dongyue Group Limited is an investment holding company that operates in the production and distribution of polymers, organic silicone, refrigerants, and other chemical products, boasting a market capitalization of approximately HK$14.10 billion.

Operations: Dongyue Group's revenue is primarily generated from polymers (CN¥4.55 billion), refrigerants (CN¥5.48 billion), organic silicon (CN¥4.86 billion), and dichloromethane PVC along with liquid alkali (CN¥1.21 billion).

Insider Ownership: 15.4%

Earnings Growth Forecast: 35.7% p.a.

Dongyue Group, a Hong Kong-based company, exhibits strong growth potential with earnings expected to rise by 35.73% annually, outpacing the local market's 11.3%. Although its revenue growth at 15.4% yearly also exceeds the Hong Kong average of 7.7%, it falls short of high-growth benchmarks. The recent dividend reduction to HK$0.10 reflects some financial caution amidst this expansion phase. Furthermore, its forecasted return on equity is relatively low at 12.9%, suggesting challenges in maintaining profitability as it scales.

- Click here to discover the nuances of Dongyue Group with our detailed analytical future growth report.

- Our comprehensive valuation report raises the possibility that Dongyue Group is priced higher than what may be justified by its financials.

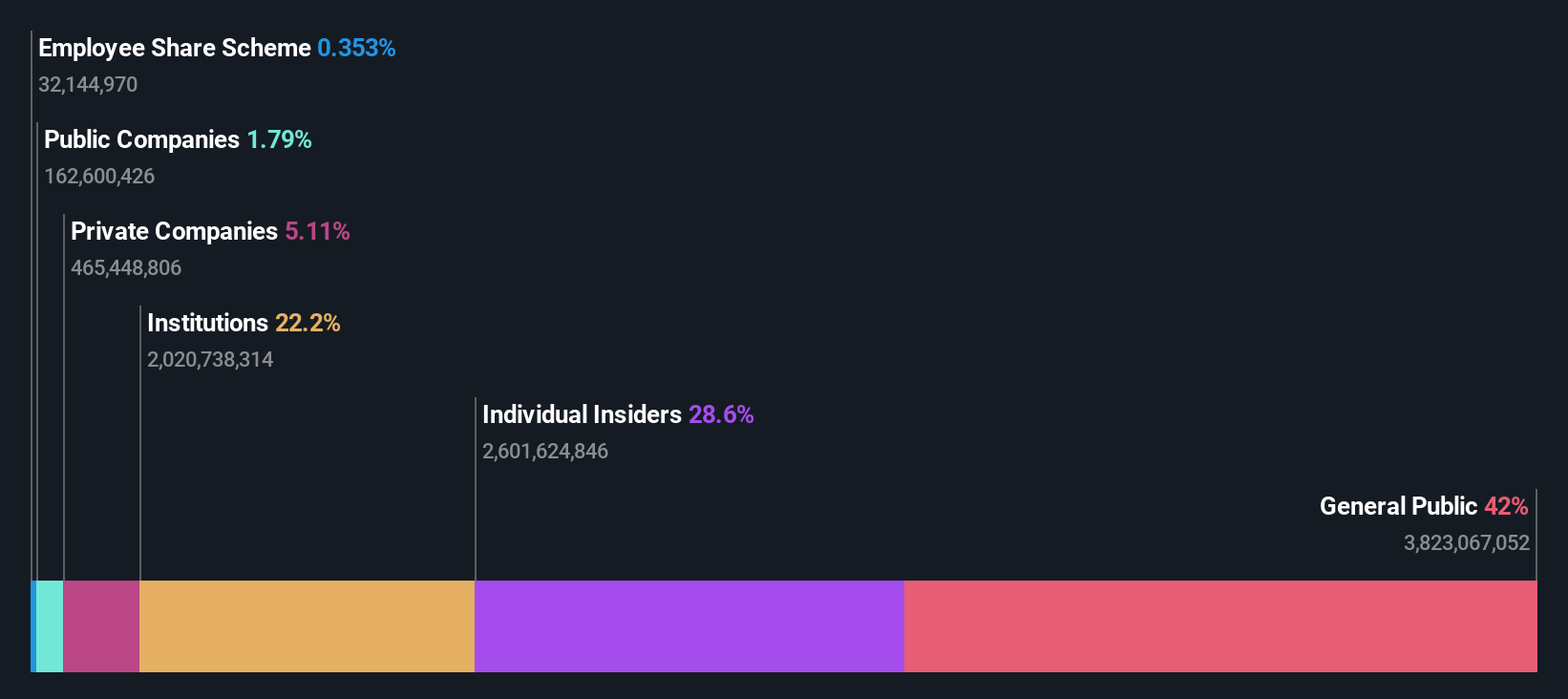

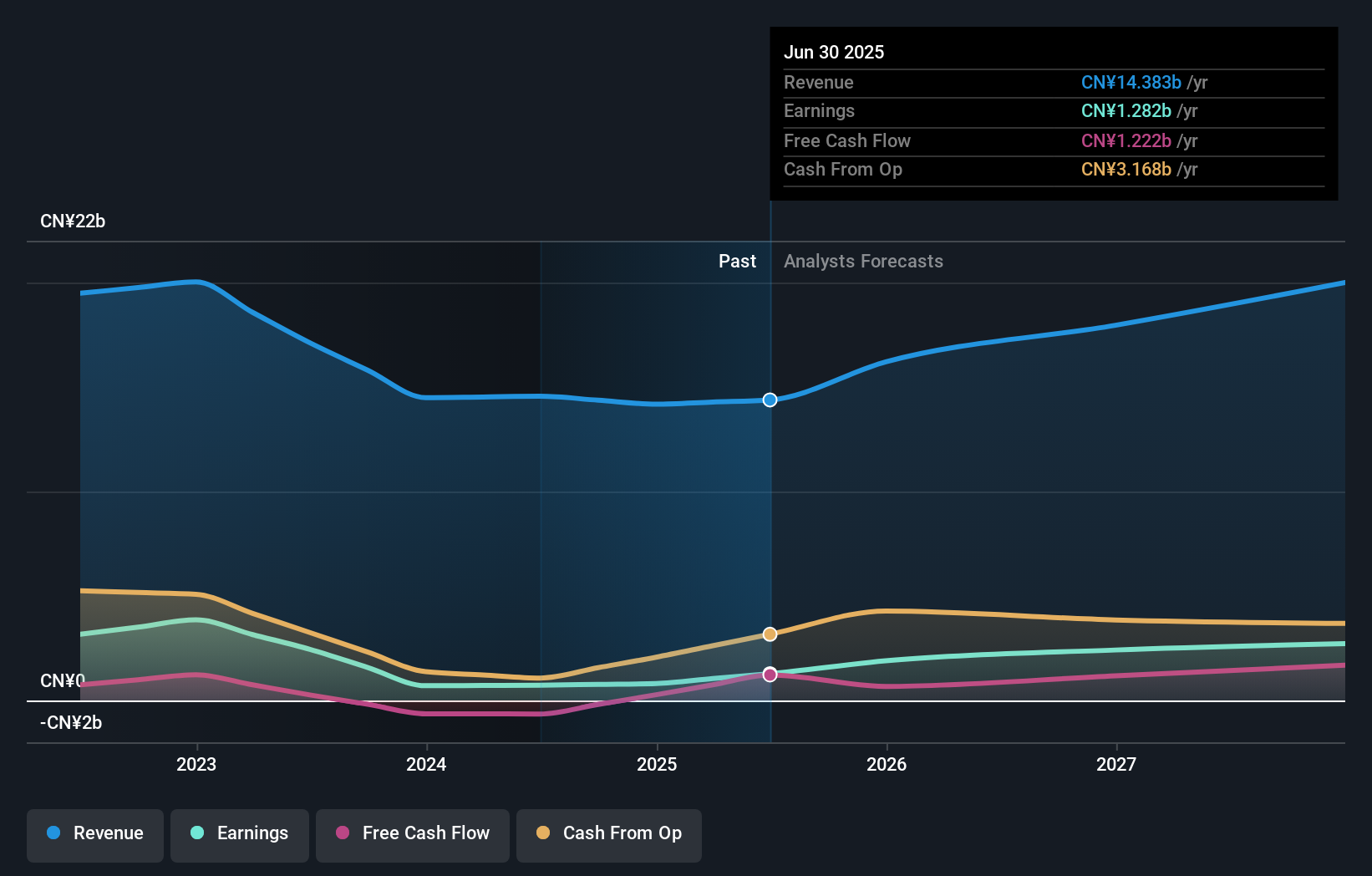

Alibaba Health Information Technology (SEHK:241)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Alibaba Health Information Technology Limited operates in Mainland China and Hong Kong, focusing on pharmaceutical direct sales, e-commerce platforms, and healthcare and digital services, with a market capitalization of approximately HK$50.17 billion.

Operations: The company generates revenue primarily through the distribution and development of pharmaceutical and healthcare products, totaling CN¥27.03 billion.

Insider Ownership: 24.2%

Earnings Growth Forecast: 23.2% p.a.

Alibaba Health Information Technology, despite trading at 64.1% below its estimated fair value, shows promising financial trends with a significant earnings growth forecast of 23.25% annually. Recent financials revealed a substantial year-over-year net income increase from CNY 535.65 million to CNY 883.48 million, underscoring robust profitability improvements. However, revenue growth projections are modest at 11% per year, slightly above the Hong Kong market average but below high-growth benchmarks. Insider transactions have not been substantial in volume over the past three months, suggesting cautious optimism among insiders about the company’s trajectory.

- Get an in-depth perspective on Alibaba Health Information Technology's performance by reading our analyst estimates report here.

- Our valuation report here indicates Alibaba Health Information Technology may be overvalued.

Summing It All Up

- Take a closer look at our Fast Growing SEHK Companies With High Insider Ownership list of 54 companies by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:241

Alibaba Health Information Technology

An investment holding company, engages in the pharmaceutical direct sales, pharmaceutical e-commerce platform, and healthcare and digital services businesses in Mainland China and Hong Kong.

Flawless balance sheet with reasonable growth potential.