Advertisement

Asian Undervalued Small Caps With Insider Activity To Watch In March 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets grapple with ongoing trade tensions and economic uncertainties, Asian small-cap stocks present intriguing opportunities for investors seeking growth potential amidst volatility. In the current climate, identifying promising small-cap companies often involves examining those with strong fundamentals and notable insider activity, which can signal confidence in their long-term prospects.

Top 10 Undervalued Small Caps With Insider Buying In Asia

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Security Bank | 4.8x | 1.1x | 30.93% | ★★★★★★ |

| Atturra | 28.2x | 1.2x | 39.15% | ★★★★★☆ |

| Hansen Technologies | 276.5x | 2.7x | 29.96% | ★★★★★☆ |

| Puregold Price Club | 8.6x | 0.4x | 18.98% | ★★★★☆☆ |

| Collins Foods | 19.3x | 0.7x | 0.71% | ★★★★☆☆ |

| Dicker Data | 19.2x | 0.7x | -44.05% | ★★★★☆☆ |

| Sing Investments & Finance | 7.3x | 3.7x | 36.12% | ★★★★☆☆ |

| Viva Energy Group | NA | 0.1x | 12.91% | ★★★★☆☆ |

| Integral Diagnostics | 144.4x | 1.7x | 44.36% | ★★★☆☆☆ |

| Manawa Energy | NA | 2.7x | 36.88% | ★★★☆☆☆ |

Let's take a closer look at a couple of our picks from the screened companies.

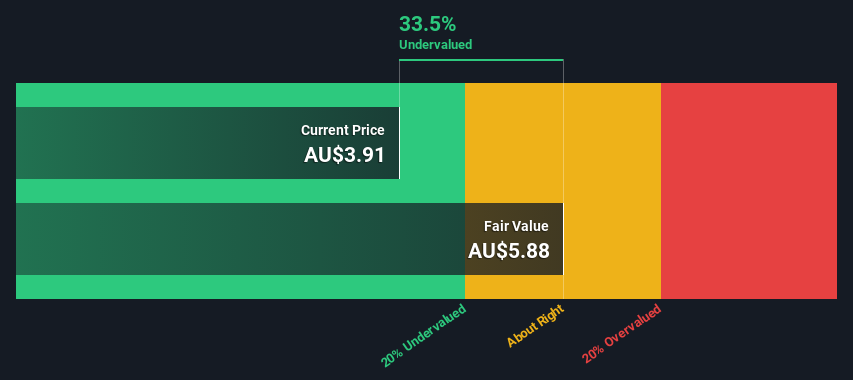

Arena REIT (ASX:ARF)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Arena REIT is a real estate investment trust focused on investing in social infrastructure properties, with a market cap of A$2.47 billion.

Operations: Arena REIT's revenue primarily stems from its investment in real estate, with the latest reported revenue at A$102.45 million. The company has shown a gross profit margin of 91.83%, reflecting efficient cost management relative to its revenue generation. Operating expenses are minimal compared to gross profit, indicating effective control over operational costs. The net income margin has varied, recently recorded at 0.73%, impacted by non-operating expenses such as interest and other financial costs.

PE: 19.0x

Arena REIT, a smaller player in the Asian market, recently reported impressive earnings for the half year ending December 31, 2024. Sales rose to A$50.99 million from A$47.03 million, while net income surged to A$36.27 million from A$19.39 million year-on-year. Basic earnings per share increased significantly to A$0.0932 from A$0.055 in the previous period, reflecting strong operational performance despite relying solely on external borrowing for funding—a riskier strategy than customer deposits typically offer. Insider confidence is evident with recent purchases by management in early 2025, signaling potential growth prospects as earnings are forecasted to grow annually by 8%.

- Delve into the full analysis valuation report here for a deeper understanding of Arena REIT.

Gain insights into Arena REIT's past trends and performance with our Past report.

Bravura Solutions (ASX:BVS)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Bravura Solutions is a software company that provides comprehensive technology solutions for the wealth management, life insurance, and funds administration industries, with a market cap of A$0.22 billion.

Operations: Bravura Solutions generates revenue primarily through its core business operations, with recent figures showing a gross profit margin of 28.72%. The company has experienced fluctuations in net income, with the latest data indicating a net income of A$71.68 million and a net income margin of 28.15%. Operating expenses have been significant, including general and administrative expenses amounting to A$18.62 million in the most recent period.

PE: 13.9x

Bravura Solutions, a smaller player in the tech sector, is catching attention with recent insider confidence shown through share purchases. For the half-year ending December 31, 2024, Bravura reported A$127.51 million in sales and a significant turnaround to A$61.24 million net income from a net loss previously. The company has revised its 2025 revenue guidance upwards to A$248-252 million. Despite being funded entirely by external borrowing, it announced both ordinary and special dividends payable in April 2025.

- Get an in-depth perspective on Bravura Solutions' performance by reading our valuation report here.

Explore historical data to track Bravura Solutions' performance over time in our Past section.

China XLX Fertiliser (SEHK:1866)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: China XLX Fertiliser is a company engaged in the production and distribution of various chemical products including urea, methanol, and compound fertilisers, with a market capitalisation of CN¥7.57 billion.

Operations: The company's primary revenue streams include Urea, Compound Fertiliser, and Methanol. Over the years, its gross profit margin has shown fluctuations, reaching 24.92% in mid-2021 before declining to 18.83% by mid-2024. Operating expenses have consistently impacted profitability with significant allocations towards sales and marketing as well as general and administrative costs.

PE: 4.2x

China XLX Fertiliser, a smaller player in the Asian market, shows potential for growth despite its high debt levels. The company relies entirely on external borrowing, which adds risk but also indicates a strategic approach to funding. Insider confidence is evident as Qingjin Zhang recently purchased 270,000 shares valued at approximately US$1.09 million, marking a 169% increase in their holdings. Earnings are projected to grow by 8% annually, offering promising prospects amidst financial challenges.

- Unlock comprehensive insights into our analysis of China XLX Fertiliser stock in this valuation report.

Assess China XLX Fertiliser's past performance with our detailed historical performance reports.

Seize The Opportunity

- Discover the full array of 62 Undervalued Asian Small Caps With Insider Buying right here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Bravura Solutions might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About ASX:BVS

Bravura Solutions

Develops, licenses, and maintains administration and management software applications for the wealth management and funds administration sectors in Australia, the United Kingdom, New Zealand, and internationally.

Flawless balance sheet and good value.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.2% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.1% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|12.7% undervalued

MA

Community Contributor