Advertisement

Is Precious Dragon Technology Holdings (HKG:1861) A Risky Investment?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. Importantly, Precious Dragon Technology Holdings Limited (HKG:1861) does carry debt. But the more important question is: how much risk is that debt creating?

What Risk Does Debt Bring?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more common (but still painful) scenario is that it has to raise new equity capital at a low price, thus permanently diluting shareholders. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

Check out our latest analysis for Precious Dragon Technology Holdings

What Is Precious Dragon Technology Holdings's Debt?

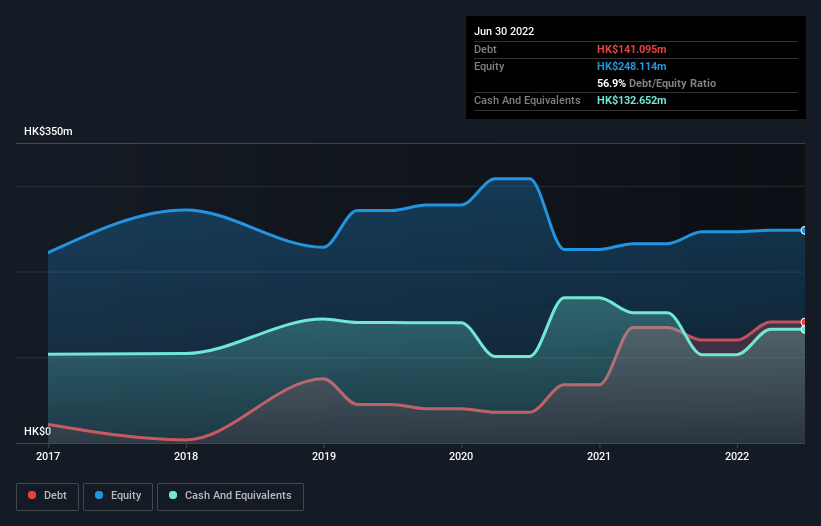

As you can see below, at the end of June 2022, Precious Dragon Technology Holdings had HK$141.1m of debt, up from HK$134.7m a year ago. Click the image for more detail. However, it also had HK$132.7m in cash, and so its net debt is HK$8.44m.

How Healthy Is Precious Dragon Technology Holdings' Balance Sheet?

According to the last reported balance sheet, Precious Dragon Technology Holdings had liabilities of HK$162.3m due within 12 months, and liabilities of HK$137.8m due beyond 12 months. Offsetting these obligations, it had cash of HK$132.7m as well as receivables valued at HK$42.0m due within 12 months. So its liabilities total HK$125.5m more than the combination of its cash and short-term receivables.

This deficit isn't so bad because Precious Dragon Technology Holdings is worth HK$299.4m, and thus could probably raise enough capital to shore up its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We use two main ratios to inform us about debt levels relative to earnings. The first is net debt divided by earnings before interest, tax, depreciation, and amortization (EBITDA), while the second is how many times its earnings before interest and tax (EBIT) covers its interest expense (or its interest cover, for short). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Precious Dragon Technology Holdings has a low net debt to EBITDA ratio of only 0.14. And its EBIT covers its interest expense a whopping 13.4 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. Fortunately, Precious Dragon Technology Holdings grew its EBIT by 7.4% in the last year, making that debt load look even more manageable. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Precious Dragon Technology Holdings's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. In the last three years, Precious Dragon Technology Holdings created free cash flow amounting to 5.1% of its EBIT, an uninspiring performance. That limp level of cash conversion undermines its ability to manage and pay down debt.

Our View

Both Precious Dragon Technology Holdings's ability to to cover its interest expense with its EBIT and its net debt to EBITDA gave us comfort that it can handle its debt. In contrast, our confidence was undermined by its apparent struggle to convert EBIT to free cash flow. When we consider all the factors mentioned above, we do feel a bit cautious about Precious Dragon Technology Holdings's use of debt. While we appreciate debt can enhance returns on equity, we'd suggest that shareholders keep close watch on its debt levels, lest they increase. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. Be aware that Precious Dragon Technology Holdings is showing 2 warning signs in our investment analysis , and 1 of those doesn't sit too well with us...

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1861

Precious Dragon Technology Holdings

Engages in the design, development, manufacturing, and sale of aerosol and non-aerosol products for applications in automotive beauty and maintenance products in the Mainland China, Japan, Asia, the Middle East, the Americas, and internationally.

Excellent balance sheet slight.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|45.0% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|47.8% undervalued

TO

Community Contributor