Advertisement

- Hong Kong

- /

- Metals and Mining

- /

- SEHK:1380

Is China Kingstone Mining Holdings (HKG:1380) Using Too Much Debt?

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, China Kingstone Mining Holdings Limited (HKG:1380) does carry debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for China Kingstone Mining Holdings

How Much Debt Does China Kingstone Mining Holdings Carry?

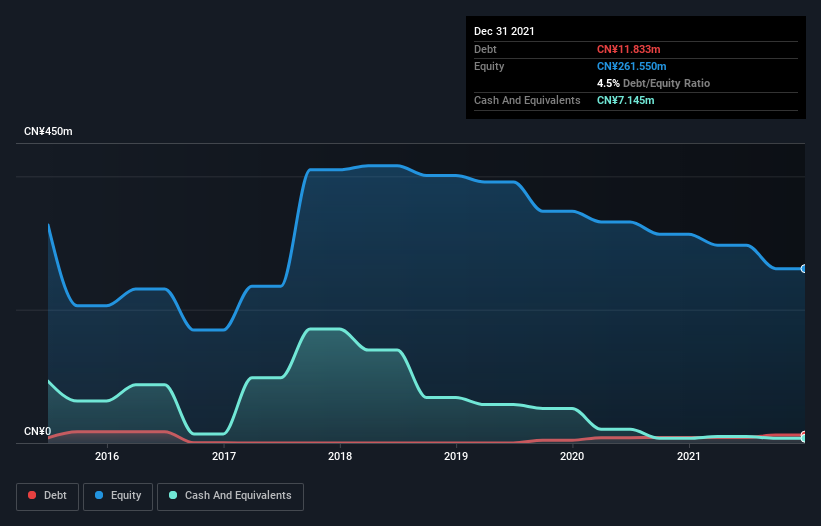

As you can see below, at the end of December 2021, China Kingstone Mining Holdings had CN¥11.8m of debt, up from CN¥8.31m a year ago. Click the image for more detail. On the flip side, it has CN¥7.15m in cash leading to net debt of about CN¥4.69m.

How Strong Is China Kingstone Mining Holdings' Balance Sheet?

We can see from the most recent balance sheet that China Kingstone Mining Holdings had liabilities of CN¥49.2m falling due within a year, and liabilities of CN¥2.78m due beyond that. On the other hand, it had cash of CN¥7.15m and CN¥71.3m worth of receivables due within a year. So it can boast CN¥26.4m more liquid assets than total liabilities.

This luscious liquidity implies that China Kingstone Mining Holdings' balance sheet is sturdy like a giant sequoia tree. On this view, lenders should feel as safe as the beloved of a black-belt karate master. When analysing debt levels, the balance sheet is the obvious place to start. But you can't view debt in total isolation; since China Kingstone Mining Holdings will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Over 12 months, China Kingstone Mining Holdings reported revenue of CN¥74m, which is a gain of 2.0%, although it did not report any earnings before interest and tax. We usually like to see faster growth from unprofitable companies, but each to their own.

Caveat Emptor

Importantly, China Kingstone Mining Holdings had an earnings before interest and tax (EBIT) loss over the last year. Indeed, it lost a very considerable CN¥50m at the EBIT level. On a more positive note, the company does have liquid assets, so it has a bit of time to improve its operations before the debt becomes an acute problem. But a profit would do more to inspire us to research the business more closely. So it seems too risky for our taste. There's no doubt that we learn most about debt from the balance sheet. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 1 warning sign for China Kingstone Mining Holdings you should know about.

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1380

China Kingstone Mining Holdings

An investment holding company, engages in the mining, processing, and trading of marble stones and marble-related products in the People’s Republic of China.

Adequate balance sheet with slight risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value US$300.00|8.5% undervalued

OS

Community Contributor

Flowers Foods Pays A Fair Price For Health

Fair Value US$16.12|24.6% undervalued

NV

Community Contributor

TMX Group will thrive with 33.3% profit margin and enduring market moat

Fair Value CA$49.90|0.1% undervalued

LI

Community Contributor