Advertisement

China Resources Gas Group And 2 Other Prominent Dividend Stocks

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate a mixed economic landscape marked by fluctuating consumer confidence and manufacturing data, investors are keenly observing the performance of major indices like the Nasdaq Composite and S&P 500, which have shown moderate gains despite recent volatility. In this context, dividend stocks such as China Resources Gas Group offer potential stability and income generation, appealing to those looking for consistent returns amidst uncertain market conditions.

Top 10 Dividend Stocks

| Name | Dividend Yield | Dividend Rating |

| Tsubakimoto Chain (TSE:6371) | 4.09% | ★★★★★★ |

| Wuliangye YibinLtd (SZSE:000858) | 3.33% | ★★★★★★ |

| CAC Holdings (TSE:4725) | 4.84% | ★★★★★★ |

| Guangxi LiuYao Group (SHSE:603368) | 3.36% | ★★★★★★ |

| Padma Oil (DSE:PADMAOIL) | 7.42% | ★★★★★★ |

| GakkyushaLtd (TSE:9769) | 4.38% | ★★★★★★ |

| Nihon Parkerizing (TSE:4095) | 3.83% | ★★★★★★ |

| China South Publishing & Media Group (SHSE:601098) | 3.66% | ★★★★★★ |

| E J Holdings (TSE:2153) | 3.82% | ★★★★★★ |

| Banque Cantonale Vaudoise (SWX:BCVN) | 5.15% | ★★★★★★ |

Click here to see the full list of 1949 stocks from our Top Dividend Stocks screener.

We're going to check out a few of the best picks from our screener tool.

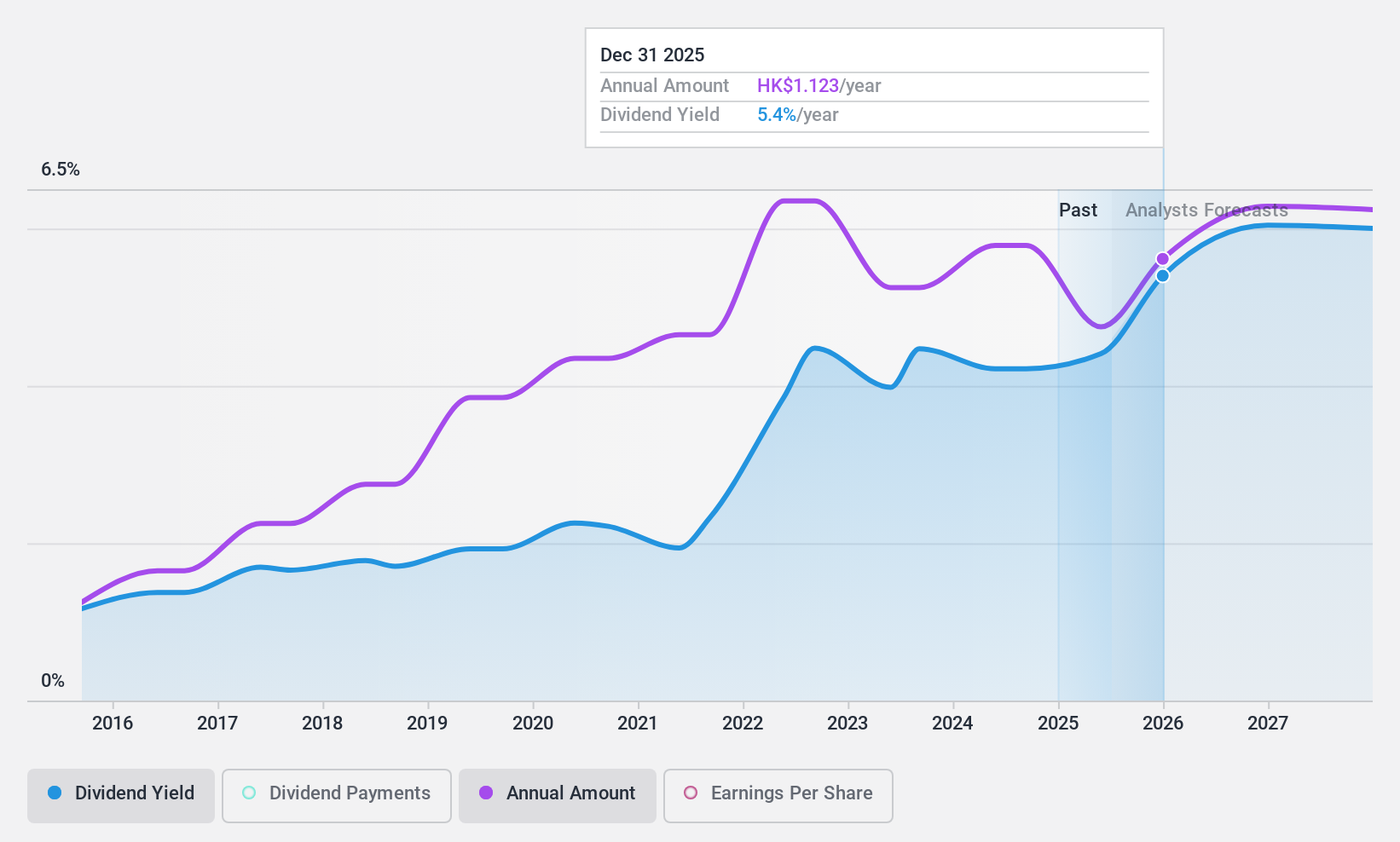

China Resources Gas Group (SEHK:1193)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: China Resources Gas Group Limited is an investment holding company involved in the sale of natural and liquefied gas and the connection of gas pipelines, with a market cap of approximately HK$69.99 billion.

Operations: China Resources Gas Group Limited generates revenue primarily from the sale and distribution of gas fuel and related products (excluding gas stations) at HK$87.31 billion, followed by gas connection services at HK$9.65 billion, comprehensive services at HK$4.34 billion, gas stations at HK$3.23 billion, and design and construction services at HK$444.11 million.

Dividend Yield: 3.8%

China Resources Gas Group's dividend payments are supported by earnings and cash flows, with payout ratios of 55.5% and 61.6%, respectively. However, the dividend yield is relatively low at 3.76% compared to top-tier payers in Hong Kong, and its dividend history has been volatile over the past decade despite some growth. Recent leadership changes, including appointing Ms. Qin Yan as CEO, may influence future strategic directions impacting dividends.

- Click here and access our complete dividend analysis report to understand the dynamics of China Resources Gas Group.

- The analysis detailed in our China Resources Gas Group valuation report hints at an deflated share price compared to its estimated value.

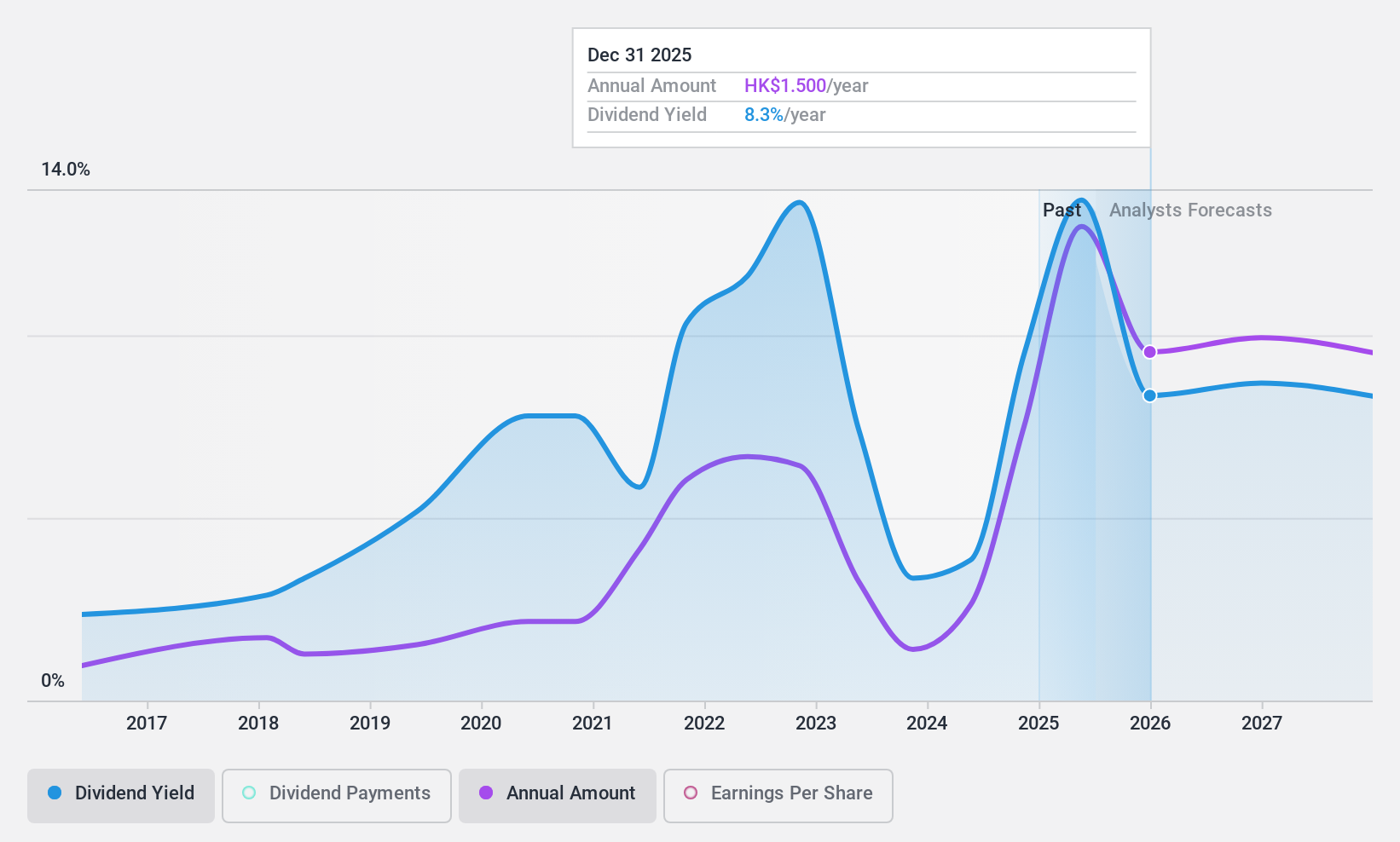

China Hongqiao Group (SEHK:1378)

Simply Wall St Dividend Rating: ★★★★★☆

Overview: China Hongqiao Group Limited is an investment holding company that manufactures and sells aluminum products in the People's Republic of China and Indonesia, with a market cap of approximately HK$109.92 billion.

Operations: China Hongqiao Group Limited generates revenue primarily through the manufacture and sale of aluminum products, amounting to CN¥141.48 billion.

Dividend Yield: 9.6%

China Hongqiao Group's dividend payments are well-supported by earnings and cash flows, with payout ratios of 42.3% and 48.6%, respectively. Despite a top-tier dividend yield of 9.62%, its track record has been volatile over the past decade, affecting reliability perceptions. Recent guidance suggests a potential net profit increase due to higher aluminium prices and lower raw material costs, which could positively impact future dividends if sustained profitability continues amidst competitive valuations in the market.

- Delve into the full analysis dividend report here for a deeper understanding of China Hongqiao Group.

- Our expertly prepared valuation report China Hongqiao Group implies its share price may be lower than expected.

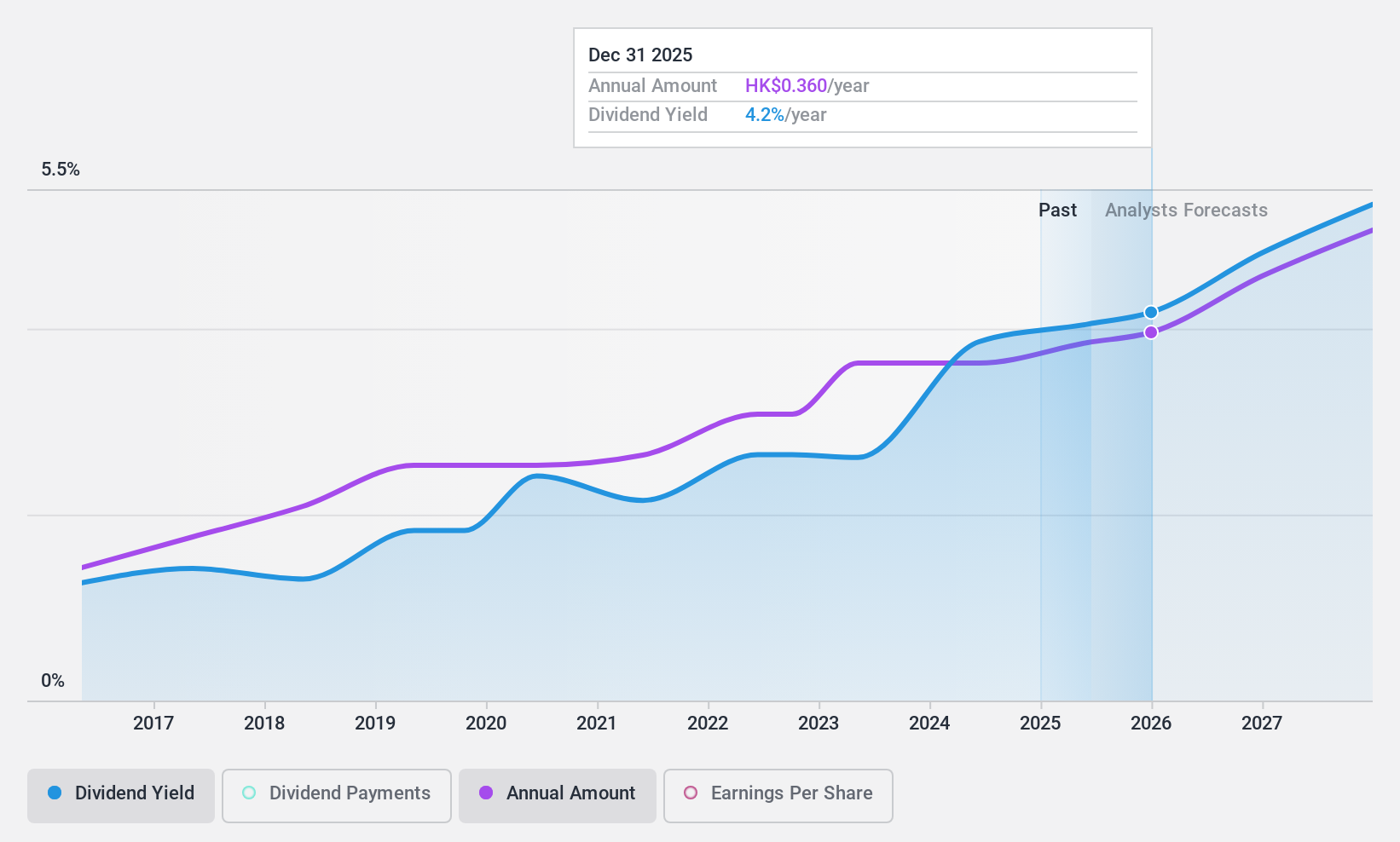

Beijing Tong Ren Tang Chinese Medicine (SEHK:3613)

Simply Wall St Dividend Rating: ★★★★☆☆

Overview: Beijing Tong Ren Tang Chinese Medicine Company Limited, with a market cap of HK$7.19 billion, operates in the manufacture, retail, and wholesale of healthcare products and Chinese medicine to both wholesalers and individuals.

Operations: Beijing Tong Ren Tang Chinese Medicine Company Limited generates its revenue from three primary segments: Overseas (HK$429.03 million), Hong Kong (HK$979.91 million), and Mainland China (HK$240.56 million).

Dividend Yield: 3.8%

Beijing Tong Ren Tang Chinese Medicine's dividends have been stable and growing over the past decade, supported by a reasonable payout ratio of 55.9%. However, the dividend yield of 3.76% is modest compared to top dividend payers in Hong Kong. The company's dividends are not well-covered by free cash flows, raising sustainability concerns despite trading below estimated fair value. Earnings growth forecasts suggest potential for future improvement if profitability aligns with expectations.

- Click to explore a detailed breakdown of our findings in Beijing Tong Ren Tang Chinese Medicine's dividend report.

- Our valuation report unveils the possibility Beijing Tong Ren Tang Chinese Medicine's shares may be trading at a premium.

Taking Advantage

- Get an in-depth perspective on all 1949 Top Dividend Stocks by using our screener here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Beijing Tong Ren Tang Chinese Medicine might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:3613

Beijing Tong Ren Tang Chinese Medicine

Engages in the manufacture, retail, and wholesale of healthcare products and Chinese medicine to wholesalers and individuals.

Flawless balance sheet established dividend payer.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.6% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|92.1% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|25.6% undervalued

GM

Community Contributor