- Hong Kong

- /

- Basic Materials

- /

- SEHK:1323

These 4 Measures Indicate That Huasheng International Holding (HKG:1323) Is Using Debt Reasonably Well

David Iben put it well when he said, 'Volatility is not a risk we care about. What we care about is avoiding the permanent loss of capital.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Huasheng International Holding Limited (HKG:1323) does have debt on its balance sheet. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. If things get really bad, the lenders can take control of the business. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Huasheng International Holding

What Is Huasheng International Holding's Debt?

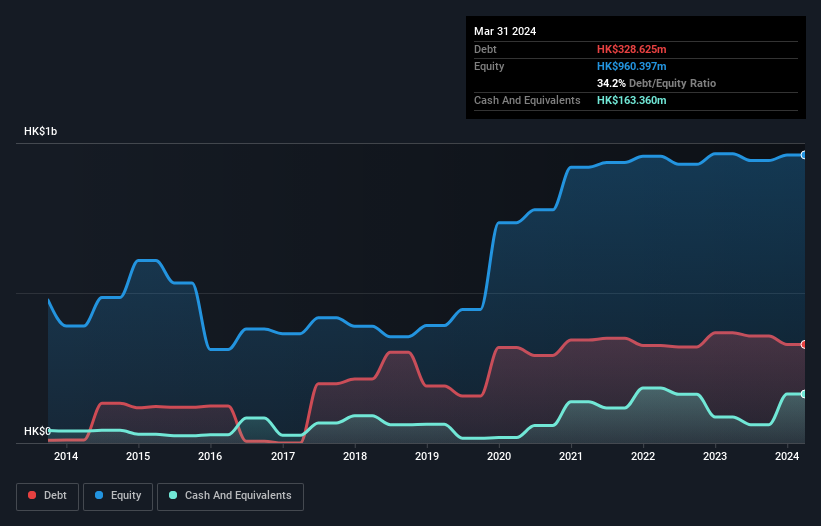

You can click the graphic below for the historical numbers, but it shows that Huasheng International Holding had HK$328.6m of debt in March 2024, down from HK$367.8m, one year before. However, it also had HK$163.4m in cash, and so its net debt is HK$165.3m.

A Look At Huasheng International Holding's Liabilities

The latest balance sheet data shows that Huasheng International Holding had liabilities of HK$460.8m due within a year, and liabilities of HK$214.8m falling due after that. Offsetting this, it had HK$163.4m in cash and HK$875.8m in receivables that were due within 12 months. So it actually has HK$363.6m more liquid assets than total liabilities.

This excess liquidity is a great indication that Huasheng International Holding's balance sheet is almost as strong as Fort Knox. On this view, lenders should feel as safe as the beloved of a black-belt karate master.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Huasheng International Holding's net debt is sitting at a very reasonable 2.5 times its EBITDA, while its EBIT covered its interest expense just 2.7 times last year. While these numbers do not alarm us, it's worth noting that the cost of the company's debt is having a real impact. The bad news is that Huasheng International Holding saw its EBIT decline by 14% over the last year. If that sort of decline is not arrested, then the managing its debt will be harder than selling broccoli flavoured ice-cream for a premium. The balance sheet is clearly the area to focus on when you are analysing debt. But it is Huasheng International Holding's earnings that will influence how the balance sheet holds up in the future. So when considering debt, it's definitely worth looking at the earnings trend. Click here for an interactive snapshot.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Huasheng International Holding recorded free cash flow worth a fulsome 98% of its EBIT, which is stronger than we'd usually expect. That positions it well to pay down debt if desirable to do so.

Our View

Happily, Huasheng International Holding's impressive conversion of EBIT to free cash flow implies it has the upper hand on its debt. But the stark truth is that we are concerned by its EBIT growth rate. When we consider the range of factors above, it looks like Huasheng International Holding is pretty sensible with its use of debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. The balance sheet is clearly the area to focus on when you are analysing debt. However, not all investment risk resides within the balance sheet - far from it. These risks can be hard to spot. Every company has them, and we've spotted 2 warning signs for Huasheng International Holding (of which 1 is concerning!) you should know about.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

Valuation is complex, but we're here to simplify it.

Discover if Huasheng International Holding might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1323

Huasheng International Holding

An investment holding company, engages in the production and sale of ready-mixed commercial concrete in the People’s Republic of China.

Flawless balance sheet and good value.

Market Insights

Community Narratives