- Hong Kong

- /

- Metals and Mining

- /

- SEHK:1029

Shareholders May Not Be So Generous With IRC Limited's (HKG:1029) CEO Compensation And Here's Why

Performance at IRC Limited (HKG:1029) has been reasonably good and CEO Yury V. Makarov has done a decent job of steering the company in the right direction. In light of this performance, CEO compensation will probably not be the main focus for shareholders as they go into the AGM on 24 June 2021. However, some shareholders will still be cautious of paying the CEO excessively.

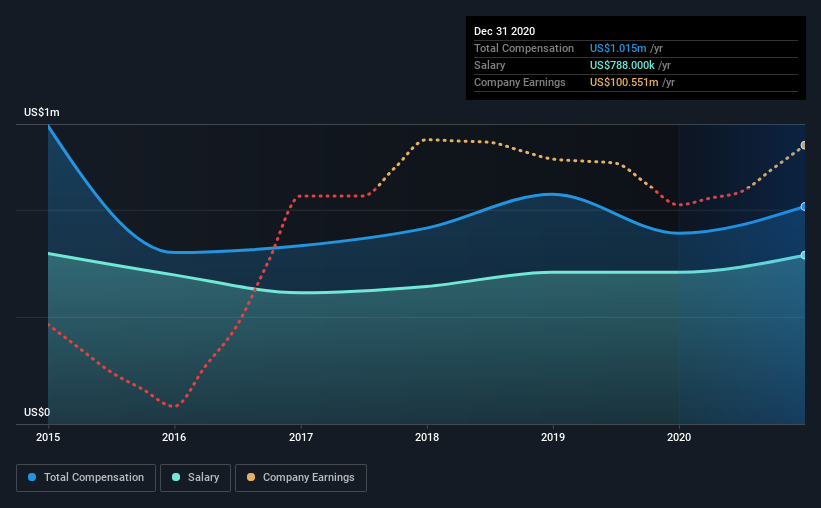

View our latest analysis for IRC

How Does Total Compensation For Yury V. Makarov Compare With Other Companies In The Industry?

At the time of writing, our data shows that IRC Limited has a market capitalization of HK$2.1b, and reported total annual CEO compensation of US$1.0m for the year to December 2020. Notably, that's an increase of 14% over the year before. We note that the salary portion, which stands at US$788.0k constitutes the majority of total compensation received by the CEO.

For comparison, other companies in the same industry with market capitalizations ranging between HK$776m and HK$3.1b had a median total CEO compensation of US$167k. Hence, we can conclude that Yury V. Makarov is remunerated higher than the industry median. What's more, Yury V. Makarov holds HK$9.0m worth of shares in the company in their own name, indicating that they have a lot of skin in the game.

| Component | 2020 | 2019 | Proportion (2020) |

| Salary | US$788k | US$708k | 78% |

| Other | US$227k | US$182k | 22% |

| Total Compensation | US$1.0m | US$890k | 100% |

On an industry level, around 84% of total compensation represents salary and 16% is other remuneration. There isn't a significant difference between IRC and the broader market, in terms of salary allocation in the overall compensation package. If salary dominates total compensation, it suggests that CEO compensation is leaning less towards the variable component, which is usually linked with performance.

A Look at IRC Limited's Growth Numbers

Over the last three years, IRC Limited has shrunk its earnings per share by 3.9% per year. It achieved revenue growth of 27% over the last year.

Investors would be a bit wary of companies that have lower EPS On the other hand, the strong revenue growth suggests the business is growing. In conclusion we can't form a strong opinion about business performance yet; but it's one worth watching. While we don't have analyst forecasts for the company, shareholders might want to examine this detailed historical graph of earnings, revenue and cash flow.

Has IRC Limited Been A Good Investment?

Boasting a total shareholder return of 112% over three years, IRC Limited has done well by shareholders. As a result, some may believe the CEO should be paid more than is normal for companies of similar size.

In Summary...

Some shareholders will be pleased by the relatively good results, however, the results could still be improved. Until EPS growth picks back up, we think shareholders may find it hard to justify increasing CEO pay given that they are already paid above industry average.

We can learn a lot about a company by studying its CEO compensation trends, along with looking at other aspects of the business. In our study, we found 3 warning signs for IRC you should be aware of, and 1 of them makes us a bit uncomfortable.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1029

IRC

Operates as an investment holding company that develops, produces, and sells industrial commodities products in the Russia, People’s Republic of China, and internationally.

Flawless balance sheet with very low risk.

Similar Companies

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion