Advertisement

AIA Group's (HKG:1299) Upcoming Dividend Will Be Larger Than Last Year's

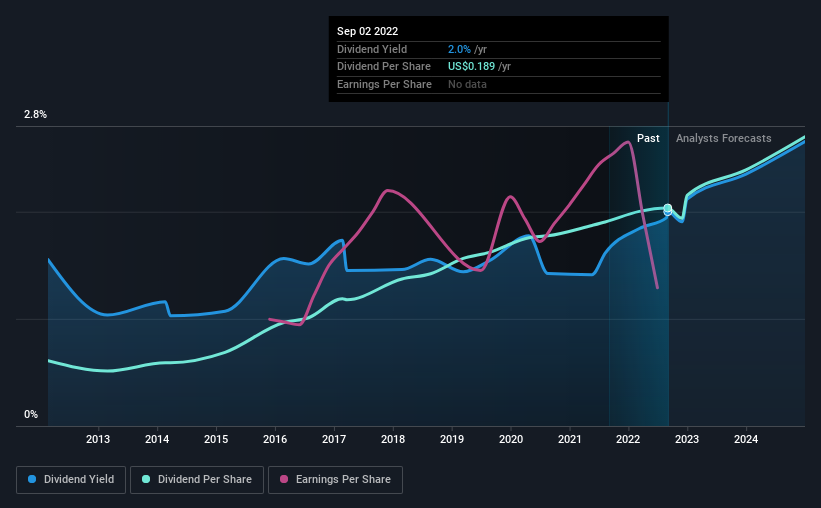

AIA Group Limited (HKG:1299) will increase its dividend from last year's comparable payment on the 29th of September to $0.4028. Even though the dividend went up, the yield is still quite low at only 2.0%.

Check out our latest analysis for AIA Group

AIA Group Doesn't Earn Enough To Cover Its Payments

While yield is important, another factor to consider about a company's dividend is whether the current payout levels are feasible. Based on the last payment, AIA Group was quite comfortably earning enough to cover the dividend. This means that a large portion of its earnings are being retained to grow the business.

Earnings per share is forecast to rise by 154.3% over the next year. Assuming the dividend continues along recent trends, we think the payout ratio could get very high, which probably can't continue without starting to put some pressure on the balance sheet.

AIA Group Has A Solid Track Record

Even over a long history of paying dividends, the company's distributions have been remarkably stable. Since 2012, the dividend has gone from $0.0566 total annually to $0.189. This works out to be a compound annual growth rate (CAGR) of approximately 13% a year over that time. So, dividends have been growing pretty quickly, and even more impressively, they haven't experienced any notable falls during this period.

Dividend Growth Is Doubtful

Investors could be attracted to the stock based on the quality of its payment history. However, initial appearances might be deceiving. Over the past five years, it looks as though AIA Group's EPS has declined at around 6.3% a year. If the company is making less over time, it naturally follows that it will also have to pay out less in dividends. Earnings are forecast to grow over the next 12 months and if that happens we could still be a little bit cautious until it becomes a pattern.

Our Thoughts On AIA Group's Dividend

Overall, it's great to see the dividend being raised and that it is still in a sustainable range. With shrinking earnings, the company may see some issues maintaining the dividend even though they look pretty sustainable for now. The dividend looks okay, but there have been some issues in the past, so we would be a little bit cautious.

It's important to note that companies having a consistent dividend policy will generate greater investor confidence than those having an erratic one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. Without at least some growth in earnings per share over time, the dividend will eventually come under pressure either from competition or inflation. See if the 23 analysts are forecasting a turnaround in our free collection of analyst estimates here. Looking for more high-yielding dividend ideas? Try our collection of strong dividend payers.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1299

Proven track record average dividend payer.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.9% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.3% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor