Advertisement

- Hong Kong

- /

- Household Products

- /

- SEHK:6601

With EPS Growth And More, Cheerwin Group (HKG:6601) Makes An Interesting Case

Investors are often guided by the idea of discovering 'the next big thing', even if that means buying 'story stocks' without any revenue, let alone profit. But as Peter Lynch said in One Up On Wall Street, 'Long shots almost never pay off.' A loss-making company is yet to prove itself with profit, and eventually the inflow of external capital may dry up.

If this kind of company isn't your style, you like companies that generate revenue, and even earn profits, then you may well be interested in Cheerwin Group (HKG:6601). Now this is not to say that the company presents the best investment opportunity around, but profitability is a key component to success in business.

See our latest analysis for Cheerwin Group

Cheerwin Group's Improving Profits

Even with very modest growth rates, a company will usually do well if it improves earnings per share (EPS) year after year. So it's no surprise that some investors are more inclined to invest in profitable businesses. In impressive fashion, Cheerwin Group's EPS grew from CN¥0.084 to CN¥0.16, over the previous 12 months. It's a rarity to see 95% year-on-year growth like that.

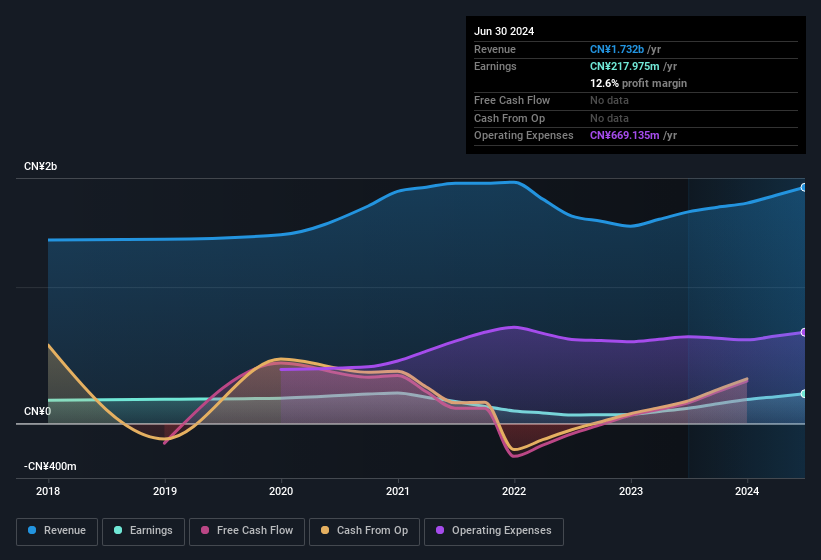

One way to double-check a company's growth is to look at how its revenue, and earnings before interest and tax (EBIT) margins are changing. The good news is that Cheerwin Group is growing revenues, and EBIT margins improved by 7.3 percentage points to 9.3%, over the last year. That's great to see, on both counts.

You can take a look at the company's revenue and earnings growth trend, in the chart below. To see the actual numbers, click on the chart.

Fortunately, we've got access to analyst forecasts of Cheerwin Group's future profits. You can do your own forecasts without looking, or you can take a peek at what the professionals are predicting.

Are Cheerwin Group Insiders Aligned With All Shareholders?

It's said that there's no smoke without fire. For investors, insider buying is often the smoke that indicates which stocks could set the market alight. Because often, the purchase of stock is a sign that the buyer views it as undervalued. However, small purchases are not always indicative of conviction, and insiders don't always get it right.

Cheerwin Group top brass are certainly in sync, not having sold any shares, over the last year. But the real excitement comes from the CN¥405k that Chairman of the Board & CEO Danxia Chen spent buying shares (at an average price of about CN¥1.35). It seems at least one insider has seen potential in the company's future - and they're willing to put money on the line.

Does Cheerwin Group Deserve A Spot On Your Watchlist?

Cheerwin Group's earnings per share have been soaring, with growth rates sky high. Growth-minded people will be intrigued by the incredible movement in EPS growth. And in fact, it could well signal a fundamental shift in the business economics. If this is the case, then keeping a watch over Cheerwin Group could be in your best interest. It's still necessary to consider the ever-present spectre of investment risk. We've identified 2 warning signs with Cheerwin Group (at least 1 which is potentially serious) , and understanding them should be part of your investment process.

The good news is that Cheerwin Group is not the only stock with insider buying. Here's a list of small cap, undervalued companies in HK with insider buying in the last three months!

Please note the insider transactions discussed in this article refer to reportable transactions in the relevant jurisdiction.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:6601

Cheerwin Group

An investment holding company, manufactures and trades household insecticides and repellents, household cleaning, air care, personal care, pet stores and pet products, and other products in the People’s Republic of China.

Very undervalued with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60.00|98.5% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|2.3% undervalued

TI

Community Contributor