Advertisement

- Hong Kong

- /

- Household Products

- /

- SEHK:6601

3 Undervalued Small Caps In Hong Kong With Insider Buying

Simply Wall St

Reviewed by Simply Wall St

In recent weeks, the Hong Kong market has faced challenges as the Hang Seng Index fell by 2.11%, reflecting broader deflationary pressures in China's economy despite new support measures from the central bank. Amidst this backdrop, small-cap stocks in Hong Kong present intriguing opportunities for investors, especially those with insider buying activity that may signal confidence in their potential value and growth prospects.

Top 10 Undervalued Small Caps With Insider Buying In Hong Kong

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Vesync | 7.0x | 1.0x | 0.25% | ★★★★★☆ |

| Ferretti | 10.8x | 0.7x | 48.35% | ★★★★★☆ |

| Edianyun | NA | 0.7x | 38.24% | ★★★★★☆ |

| Cheerwin Group | 11.6x | 1.5x | 45.12% | ★★★★☆☆ |

| Lion Rock Group | 5.6x | 0.4x | 48.83% | ★★★★☆☆ |

| Gemdale Properties and Investment | NA | 0.2x | 46.80% | ★★★★☆☆ |

| China Lesso Group Holdings | 5.7x | 0.4x | -491.43% | ★★★☆☆☆ |

| Skyworth Group | 5.6x | 0.1x | -293.45% | ★★★☆☆☆ |

| Lee & Man Paper Manufacturing | 6.9x | 0.4x | -42.22% | ★★★☆☆☆ |

| Emperor International Holdings | NA | 0.8x | 29.45% | ★★★☆☆☆ |

We're going to check out a few of the best picks from our screener tool.

Lee & Man Paper Manufacturing (SEHK:2314)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Lee & Man Paper Manufacturing is engaged in the production and sale of pulp, tissue paper, and packaging paper, with a market capitalization of HK$10.23 billion.

Operations: The company generates revenue primarily from packaging paper, followed by tissue paper and pulp. Over time, its gross profit margin has shown fluctuations, peaking at 29.08% in late 2017 before declining to 12.49% by mid-2024. Operating expenses are a significant cost component, with general and administrative expenses consistently forming a substantial part of these costs.

PE: 6.9x

Lee & Man Paper Manufacturing, a smaller player in Hong Kong's market, has shown significant insider confidence with Ho Chung Lee purchasing 483,000 shares valued at approximately HK$1.1 million between January and May 2024. This move aligns with the company's strategic share repurchase of over 14 million shares for HK$29.65 million during the same period, suggesting potential undervaluation. Despite relying on higher-risk external borrowing for funding, their earnings surged to HK$805.69 million in H1 2024 from HK$359.9 million a year earlier, signaling growth potential amidst financial challenges.

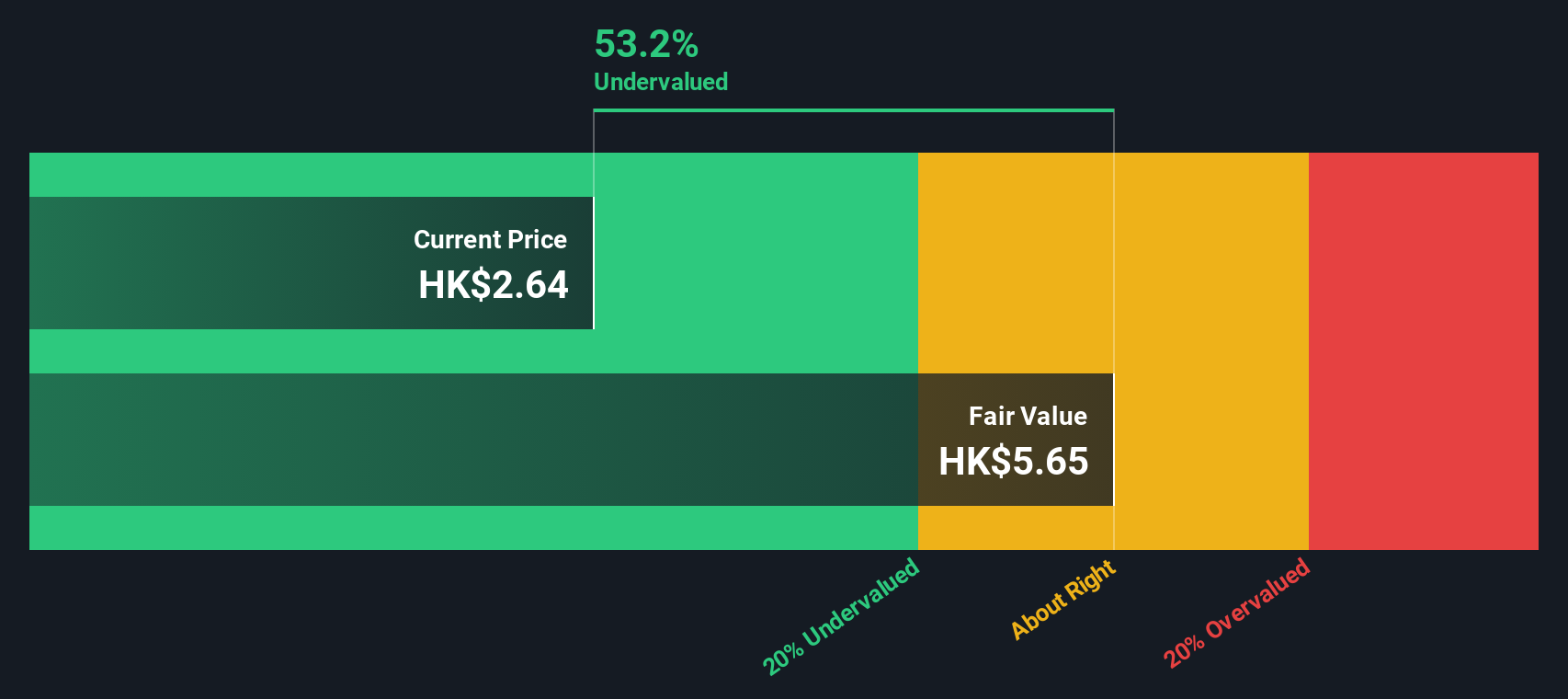

Cheerwin Group (SEHK:6601)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Cheerwin Group is a company primarily engaged in the production and distribution of household care, personal care, and pet products, with a market capitalization of CN¥3.95 billion.

Operations: The primary revenue streams for the company include Household Care, Personal Care, and Pets and Pet Products, with Household Care being the most significant contributor. Over recent periods, the gross profit margin has shown an upward trend, reaching 47.89% by mid-2024. Operating expenses are primarily driven by sales and marketing efforts alongside general administrative costs.

PE: 11.6x

Cheerwin Group, a player in the consumer goods sector, has been attracting attention for its potential value. With earnings growing to CNY 179.46 million from CNY 136.5 million year-on-year by June 2024, the company shows promising financial health. Insider confidence is evident as Danxia Chen acquired 300,000 shares worth approximately RMB 405,059 in August 2024. Despite relying solely on external borrowing for funding, Cheerwin's forecasted annual earnings growth of about 3.92% suggests resilience and potential future gains in this dynamic market segment.

- Unlock comprehensive insights into our analysis of Cheerwin Group stock in this valuation report.

Assess Cheerwin Group's past performance with our detailed historical performance reports.

Skyworth Group (SEHK:751)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Skyworth Group is a diversified technology company engaged in smart household appliances, smart systems technology, modern services, and new energy businesses with a market capitalization of approximately CN¥7.67 billion.

Operations: Skyworth Group's primary revenue streams include the Smart Household Appliances Business and New Energy Business, generating CN¥32.51 billion and CN¥20.21 billion, respectively. The company's gross profit margin has shown fluctuations, reaching 14.36% in recent periods.

PE: 5.6x

Skyworth Group, a smaller player in Hong Kong's market, has caught attention with significant insider confidence. CEO & Executive Director Chi Shi recently purchased 2.19 million shares for HK$6.3 million, increasing their stake by 16.5%. Such moves often signal belief in the company's potential despite challenges like reliance on external borrowing and cash flow issues covering debt inadequately. Skyworth's strategic expansion into Russia showcases its commitment to innovation and growth, aiming to enhance its international footprint with advanced technology offerings.

- Navigate through the intricacies of Skyworth Group with our comprehensive valuation report here.

Understand Skyworth Group's track record by examining our Past report.

Where To Now?

- Gain an insight into the universe of 11 Undervalued SEHK Small Caps With Insider Buying by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:6601

Cheerwin Group

An investment holding company, manufactures and trades household insecticides and repellents, household cleaning, air care, personal care, pet stores and pet products, and other products in the People’s Republic of China.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|8.7% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor