- Hong Kong

- /

- Paper and Forestry Products

- /

- SEHK:2314

3 Undervalued Small Caps In Hong Kong With Insider Action

Reviewed by Simply Wall St

In recent weeks, the Hong Kong market has experienced fluctuations, with the Hang Seng Index declining by 1.03% as global economic conditions and local monetary policies continue to impact investor sentiment. Amid these dynamics, investors are increasingly interested in small-cap stocks that may be undervalued but show potential for growth due to insider activity, which can be an indicator of confidence in a company's future prospects. Identifying such stocks requires careful consideration of market conditions and company fundamentals to gauge their potential resilience and growth opportunities in a volatile environment.

Top 10 Undervalued Small Caps With Insider Buying In Hong Kong

| Name | PE | PS | Discount to Fair Value | Value Rating |

|---|---|---|---|---|

| Vesync | 7.0x | 1.0x | 0.08% | ★★★★★☆ |

| Ferretti | 11.1x | 0.7x | 46.56% | ★★★★★☆ |

| Edianyun | NA | 0.7x | 37.54% | ★★★★★☆ |

| Lion Rock Group | 5.6x | 0.4x | 48.79% | ★★★★☆☆ |

| Gemdale Properties and Investment | NA | 0.2x | 45.79% | ★★★★☆☆ |

| Cheerwin Group | 11.8x | 1.5x | 44.01% | ★★★☆☆☆ |

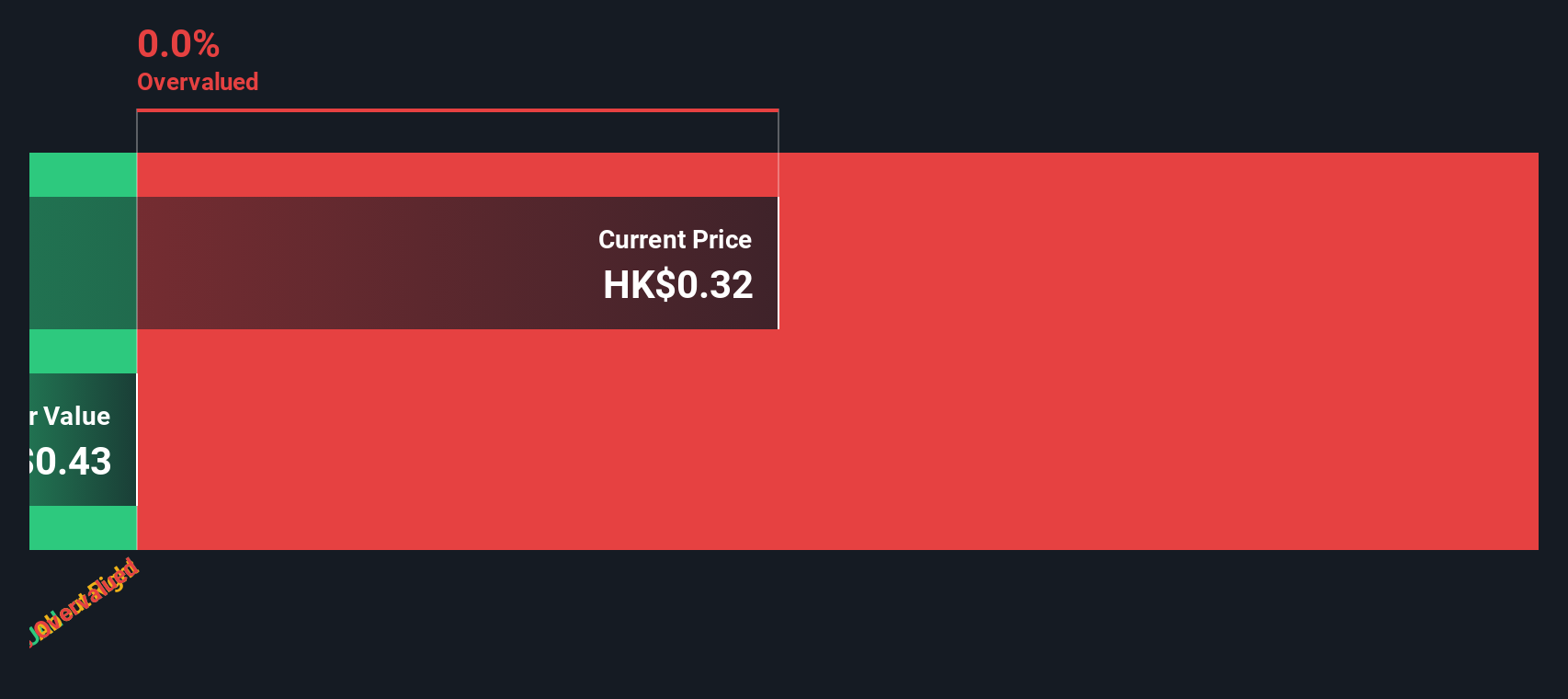

| China Lesso Group Holdings | 5.7x | 0.4x | -498.10% | ★★★☆☆☆ |

| Lee & Man Paper Manufacturing | 7.0x | 0.4x | -43.98% | ★★★☆☆☆ |

| Guangdong Kanghua Healthcare Group | 13.0x | 0.3x | 10.44% | ★★★☆☆☆ |

| Emperor International Holdings | NA | 0.8x | 29.45% | ★★★☆☆☆ |

Below we spotlight a couple of our favorites from our exclusive screener.

Lee & Man Paper Manufacturing (SEHK:2314)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Lee & Man Paper Manufacturing operates in the production of pulp, tissue paper, and packaging paper with a market capitalization of HK$14.5 billion.

Operations: The company generates revenue primarily from packaging paper and tissue paper, with packaging paper contributing significantly to its total income. The cost of goods sold (COGS) is a major expenditure, impacting the gross profit margin, which has shown variability over time, peaking at 29.08% in late 2017 before declining to 12.49% by mid-2024. Operating expenses include sales and marketing as well as general and administrative costs, which together form a substantial part of the company's financial structure.

PE: 7.0x

Lee & Man Paper Manufacturing, a smaller player in Hong Kong's market, shows signs of being undervalued with recent insider confidence as Ho Chung Lee acquired 483,000 shares for approximately HK$1.1 million in 2024. Despite relying on higher-risk external borrowing, the company reported notable earnings growth for the first half of 2024, with net income rising to HK$805.69 million from HK$359.9 million last year. Additionally, they completed a share repurchase program and increased their dividend payout to HK$0.062 per share.

Gemdale Properties and Investment (SEHK:535)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Gemdale Properties and Investment focuses on property development and property investment and management, with a market cap of approximately CN¥4.35 billion.

Operations: The company's primary revenue streams are from Property Development, generating CN¥17.26 billion, and Property Investment and Management, contributing CN¥1.23 billion. The gross profit margin has shown fluctuations over recent periods, with a notable figure of 10.57% as of December 2023.

PE: -1.8x

Gemdale Properties and Investment, a smaller player in Hong Kong's market, has seen its share price fluctuate significantly over the past three months. Despite this volatility, insider confidence is evident with Lian Huat Loh acquiring 10 million shares recently for approximately RMB 2.6 million. However, the company faces challenges; earnings have declined by 29.5% annually over five years and interest payments aren't well covered by earnings. Recent sales figures show contracted sales of RMB 14.18 billion from January to September 2024 across over one million square meters at an average price of RMB 18,000 per square meter. The financial position remains precarious due to reliance on external borrowing without customer deposits as security.

- Unlock comprehensive insights into our analysis of Gemdale Properties and Investment stock in this valuation report.

Learn about Gemdale Properties and Investment's historical performance.

Cheerwin Group (SEHK:6601)

Simply Wall St Value Rating: ★★★☆☆☆

Overview: Cheerwin Group is a company engaged in the production and distribution of household care, personal care, and pet products, with a focus on the Chinese market.

Operations: The company generates revenue primarily from Household Care, contributing significantly to its total income, followed by Pets and Pet Products and Personal Care. Over the periods analyzed, the gross profit margin has shown a notable increase from 35.94% in December 2017 to 47.89% in October 2024. The company's operating expenses are largely driven by sales and marketing costs, with general and administrative expenses also playing a significant role.

PE: 11.8x

Cheerwin Group, a smaller player in Hong Kong's market, recently showcased insider confidence when their Chairman and CEO acquired 300,000 shares for approximately HK$405,059. This move suggests belief in the company's potential. For the first half of 2024, Cheerwin reported sales of CNY 1.25 billion and net income of CNY 179 million, reflecting solid growth from the previous year. While earnings are projected to grow annually by around 3.92%, reliance on external borrowing poses some risk.

- Dive into the specifics of Cheerwin Group here with our thorough valuation report.

Explore historical data to track Cheerwin Group's performance over time in our Past section.

Next Steps

- Gain an insight into the universe of 11 Undervalued SEHK Small Caps With Insider Buying by clicking here.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2314

Lee & Man Paper Manufacturing

An investment holding company, engages in the manufacture and trading of packaging papers, pulps, and tissue papers in the People’s Republic of China, Vietnam, Malaysia, Macau, and Hong Kong.

Proven track record and fair value.