We're Hopeful That Besunyen Holdings (HKG:926) Will Use Its Cash Wisely

We can readily understand why investors are attracted to unprofitable companies. For example, biotech and mining exploration companies often lose money for years before finding success with a new treatment or mineral discovery. But the harsh reality is that very many loss making companies burn through all their cash and go bankrupt.

So should Besunyen Holdings (HKG:926) shareholders be worried about its cash burn? In this article, we define cash burn as its annual (negative) free cash flow, which is the amount of money a company spends each year to fund its growth. The first step is to compare its cash burn with its cash reserves, to give us its 'cash runway'.

When Might Besunyen Holdings Run Out Of Money?

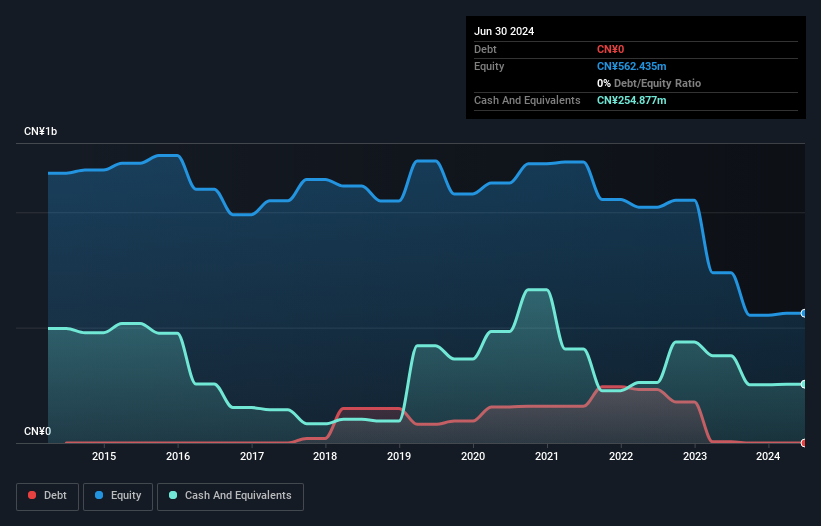

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. When Besunyen Holdings last reported its June 2024 balance sheet in August 2024, it had zero debt and cash worth CN¥255m. Importantly, its cash burn was CN¥70m over the trailing twelve months. That means it had a cash runway of about 3.6 years as of June 2024. A runway of this length affords the company the time and space it needs to develop the business. You can see how its cash balance has changed over time in the image below.

View our latest analysis for Besunyen Holdings

Is Besunyen Holdings' Revenue Growing?

Given that Besunyen Holdings actually had positive free cash flow last year, before burning cash this year, we'll focus on its operating revenue to get a measure of the business trajectory. Regrettably, the company's operating revenue moved in the wrong direction over the last twelve months, declining by 39%. In reality, this article only makes a short study of the company's growth data. You can take a look at how Besunyen Holdings has developed its business over time by checking this visualization of its revenue and earnings history.

How Hard Would It Be For Besunyen Holdings To Raise More Cash For Growth?

Given its problematic fall in revenue, Besunyen Holdings shareholders should consider how the company could fund its growth, if it turns out it needs more cash. Generally speaking, a listed business can raise new cash through issuing shares or taking on debt. Many companies end up issuing new shares to fund future growth. By comparing a company's annual cash burn to its total market capitalisation, we can estimate roughly how many shares it would have to issue in order to run the company for another year (at the same burn rate).

Besunyen Holdings' cash burn of CN¥70m is about 30% of its CN¥236m market capitalisation. That's fairly notable cash burn, so if the company had to sell shares to cover the cost of another year's operations, shareholders would suffer some costly dilution.

Is Besunyen Holdings' Cash Burn A Worry?

Even though its falling revenue makes us a little nervous, we are compelled to mention that we thought Besunyen Holdings' cash runway was relatively promising. Cash burning companies are always on the riskier side of things, but after considering all of the factors discussed in this short piece, we're not too worried about its rate of cash burn. On another note, we conducted an in-depth investigation of the company, and identified 4 warning signs for Besunyen Holdings (2 are significant!) that you should be aware of before investing here.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of companies with significant insider holdings, and this list of stocks growth stocks (according to analyst forecasts)

Valuation is complex, but we're here to simplify it.

Discover if Besunyen Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:926

Besunyen Holdings

Engages in the research and development, production, promotion, and sale of therapeutic tea products and pharmaceuticals in the People's Republic of China and internationally.

Flawless balance sheet with acceptable track record.

Market Insights

Community Narratives