Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital. It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, China Greenfresh Group Co., Ltd. (HKG:6183) does carry debt. But the more important question is: how much risk is that debt creating?

When Is Debt Dangerous?

Debt and other liabilities become risky for a business when it cannot easily fulfill those obligations, either with free cash flow or by raising capital at an attractive price. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, debt can be an important tool in businesses, particularly capital heavy businesses. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

Check out our latest analysis for China Greenfresh Group

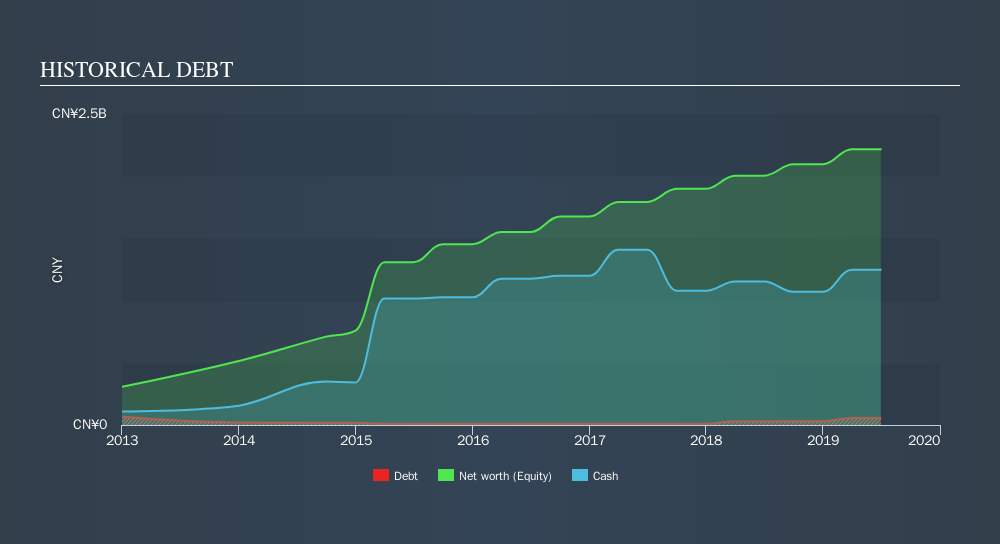

How Much Debt Does China Greenfresh Group Carry?

You can click the graphic below for the historical numbers, but it shows that as of June 2019 China Greenfresh Group had CN¥56.6m of debt, an increase on CN¥29.2m, over one year. However, it does have CN¥1.25b in cash offsetting this, leading to net cash of CN¥1.19b.

A Look At China Greenfresh Group's Liabilities

According to the last reported balance sheet, China Greenfresh Group had liabilities of CN¥137.8m due within 12 months, and liabilities of CN¥5.83m due beyond 12 months. On the other hand, it had cash of CN¥1.25b and CN¥209.4m worth of receivables due within a year. So it can boast CN¥1.31b more liquid assets than total liabilities.

This excess liquidity is a great indication that China Greenfresh Group's balance sheet is just as strong as racists are weak. On this view, it seems its balance sheet is as strong as a black-belt karate master. Simply put, the fact that China Greenfresh Group has more cash than debt is arguably a good indication that it can manage its debt safely.

On the other hand, China Greenfresh Group's EBIT dived 17%, over the last year. We think hat kind of performance, if repeated frequently, could well lead to difficulties for the stock. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since China Greenfresh Group will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

Finally, a business needs free cash flow to pay off debt; accounting profits just don't cut it. China Greenfresh Group may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. Happily for any shareholders, China Greenfresh Group actually produced more free cash flow than EBIT over the last three years. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Summing up

While it is always sensible to investigate a company's debt, in this case China Greenfresh Group has CN¥1.19b in net cash and a strong balance sheet. The cherry on top was that in converted 122% of that EBIT to free cash flow, bringing in CN¥156m. So is China Greenfresh Group's debt a risk? It doesn't seem so to us. Another factor that would give us confidence in China Greenfresh Group would be if insiders have been buying shares: if you're conscious of that signal too, you can find out instantly by clicking this link.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.

Market Insights

Advertisement

Community Narratives

The Future of Drug Testing? Fingerprint Tech Shows Serious Promise

Fair Value US$2.98|40.3% undervalued

JO

Community Contributor

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|7.6% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|30.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$359.72|12.3% undervalued

BL

Community Contributor