Improved Earnings Required Before WH Group Limited (HKG:288) Shares Find Their Feet

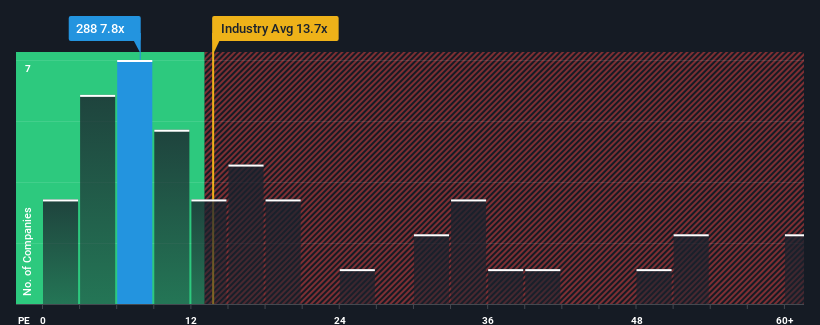

With a price-to-earnings (or "P/E") ratio of 7.8x WH Group Limited (HKG:288) may be sending bullish signals at the moment, given that almost half of all companies in Hong Kong have P/E ratios greater than 11x and even P/E's higher than 23x are not unusual. Although, it's not wise to just take the P/E at face value as there may be an explanation why it's limited.

We've discovered 2 warning signs about WH Group. View them for free.With earnings growth that's superior to most other companies of late, WH Group has been doing relatively well. One possibility is that the P/E is low because investors think this strong earnings performance might be less impressive moving forward. If you like the company, you'd be hoping this isn't the case so that you could potentially pick up some stock while it's out of favour.

View our latest analysis for WH Group

What Are Growth Metrics Telling Us About The Low P/E?

WH Group's P/E ratio would be typical for a company that's only expected to deliver limited growth, and importantly, perform worse than the market.

Taking a look back first, we see that the company grew earnings per share by an impressive 156% last year. The strong recent performance means it was also able to grow EPS by 51% in total over the last three years. So we can start by confirming that the company has done a great job of growing earnings over that time.

Turning to the outlook, the next three years should bring diminished returns, with earnings decreasing 1.3% per annum as estimated by the analysts watching the company. That's not great when the rest of the market is expected to grow by 15% each year.

With this information, we are not surprised that WH Group is trading at a P/E lower than the market. Nonetheless, there's no guarantee the P/E has reached a floor yet with earnings going in reverse. Even just maintaining these prices could be difficult to achieve as the weak outlook is weighing down the shares.

What We Can Learn From WH Group's P/E?

We'd say the price-to-earnings ratio's power isn't primarily as a valuation instrument but rather to gauge current investor sentiment and future expectations.

We've established that WH Group maintains its low P/E on the weakness of its forecast for sliding earnings, as expected. Right now shareholders are accepting the low P/E as they concede future earnings probably won't provide any pleasant surprises. Unless these conditions improve, they will continue to form a barrier for the share price around these levels.

Don't forget that there may be other risks. For instance, we've identified 2 warning signs for WH Group (1 can't be ignored) you should be aware of.

You might be able to find a better investment than WH Group. If you want a selection of possible candidates, check out this free list of interesting companies that trade on a low P/E (but have proven they can grow earnings).

Valuation is complex, but we're here to simplify it.

Discover if WH Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:288

WH Group

An investment holding company, produces and sells packaged meats and pork in China, North America, and Europe.

Flawless balance sheet and undervalued.

Similar Companies

Market Insights

Community Narratives