Advertisement

- Japan

- /

- Electronic Equipment and Components

- /

- TSE:6961

Undiscovered Gems Three Promising Stocks To Watch In February 2025

Simply Wall St

Reviewed by Simply Wall St

As global markets edge toward record highs, recent inflation data and monetary policy discussions have brought volatility to the forefront, with small-cap stocks underperforming their larger counterparts. In this dynamic environment, identifying promising stocks requires a keen eye for companies that demonstrate resilience and potential growth amidst economic fluctuations.

Top 10 Undiscovered Gems With Strong Fundamentals

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Sugar Terminals | NA | 3.14% | 3.53% | ★★★★★★ |

| Yuen Foong Yu Consumer Products | 27.23% | 0.46% | -3.46% | ★★★★★★ |

| Wilson Bank Holding | NA | 7.87% | 8.22% | ★★★★★★ |

| Ovostar Union | 0.01% | 10.19% | 49.85% | ★★★★★★ |

| Sonix TechnologyLtd | NA | -10.07% | -16.54% | ★★★★★★ |

| Pacific Construction | 21.40% | -3.50% | 26.25% | ★★★★★★ |

| First Copper Technology | 17.03% | 3.07% | 19.66% | ★★★★★★ |

| Ve Wong | 11.84% | 0.61% | 3.56% | ★★★★★☆ |

| Steamships Trading | 33.60% | 4.17% | 3.90% | ★★★★★☆ |

| Huang Hsiang Construction | 266.70% | 13.12% | 15.19% | ★★★★☆☆ |

We'll examine a selection from our screener results.

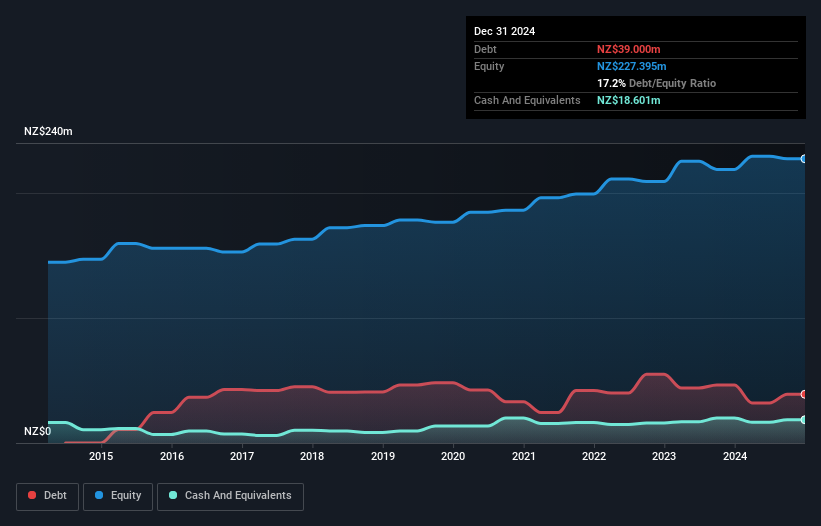

Skellerup Holdings (NZSE:SKL)

Simply Wall St Value Rating: ★★★★★★

Overview: Skellerup Holdings Limited designs, manufactures, and distributes engineered products for specialist industrial and agricultural applications, with a market capitalization of NZ$1.05 billion.

Operations: Skellerup Holdings generates revenue primarily through its Industrial segment, contributing NZ$232.02 million, and its Agri segment, which adds NZ$107.30 million.

Skellerup Holdings, a nimble player in the market, showcases robust financial health with high-quality earnings and a satisfactory net debt to equity ratio of 9%. Over the past five years, it has successfully reduced its debt to equity from 27.3% to 17.2%, reflecting prudent financial management. Trading at 14% below estimated fair value, Skellerup appears undervalued. Recent earnings reveal sales of NZ$165 million and net income of NZ$24 million for the year ending December 2024, indicating growth from previous figures. With an interim dividend increase to 9 cents per share and well-covered interest payments (20x EBIT), the outlook remains positive for this under-the-radar contender.

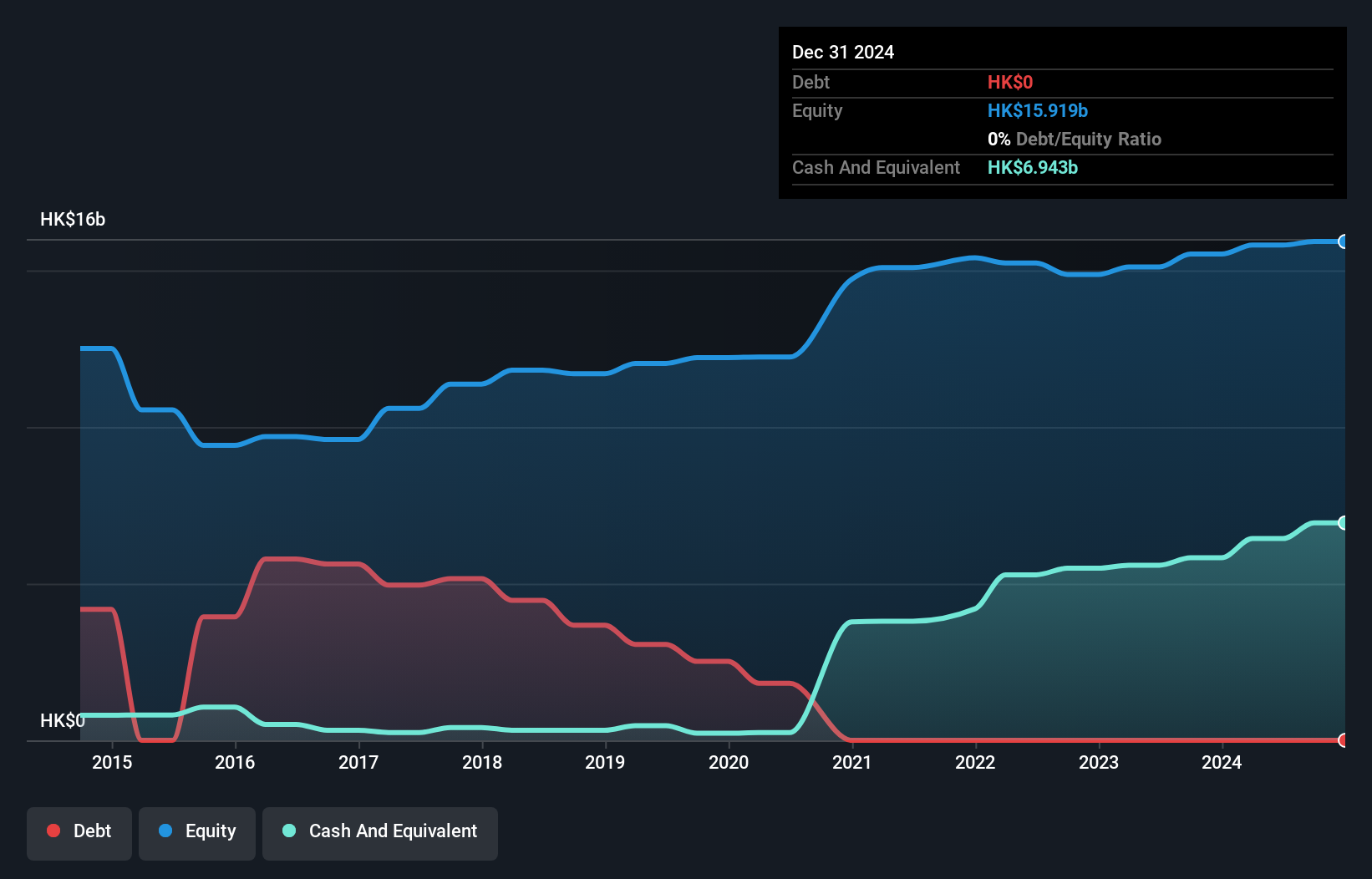

Sinopec Kantons Holdings (SEHK:934)

Simply Wall St Value Rating: ★★★★★★

Overview: Sinopec Kantons Holdings Limited is an investment holding company that offers crude oil jetty services, with a market capitalization of HK$10.91 billion.

Operations: The company's primary revenue stream is from crude oil jetty and storage services, generating HK$632.38 million. The market capitalization stands at HK$10.91 billion.

Sinopec Kantons Holdings, a smaller player in the oil and gas sector, showcases impressive financial health with no debt on its books, a significant improvement from a 25.5% debt-to-equity ratio five years ago. The company is trading at 60.7% below its estimated fair value, suggesting potential undervaluation in the market. Over the past year, earnings have surged by 50.8%, outpacing industry growth of -0.9%. With high-quality earnings and positive free cash flow reported consistently over recent periods, Sinopec Kantons seems well-positioned for continued profitability and stability in an otherwise volatile industry landscape.

- Click here and access our complete health analysis report to understand the dynamics of Sinopec Kantons Holdings.

Learn about Sinopec Kantons Holdings' historical performance.

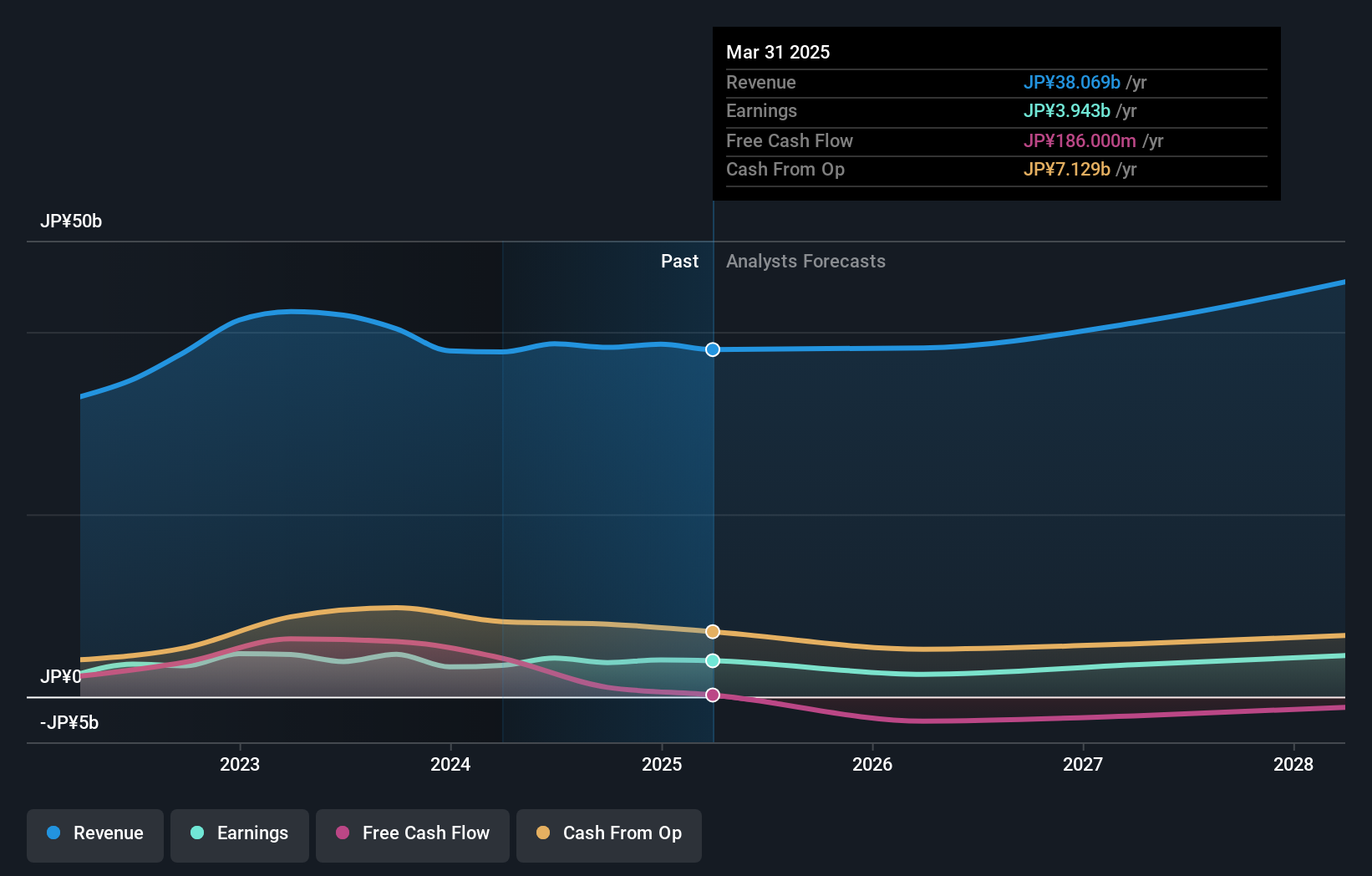

Enplas (TSE:6961)

Simply Wall St Value Rating: ★★★★★★

Overview: Enplas Corporation is a Japanese company that manufactures and sells semiconductor, automobile parts, optical communication devices, and life science-related products both domestically and internationally, with a market cap of ¥41.92 billion.

Operations: Enplas generates revenue primarily from its Semiconductor Business, contributing ¥16.55 billion, and its Energy Saving Solutions Business at ¥14.13 billion. The company also earns from the Digital Communication Business and Life Science Business with revenues of ¥5.35 billion and ¥2.62 billion, respectively.

Enplas, a nimble player in the electronics sector, has shown impressive earnings growth of 23.3% over the past year, outpacing the industry average of 7.2%. The company is debt-free and offers high-quality earnings, making it an attractive proposition for those seeking stability in financial health. Trading at 29.2% below its estimated fair value suggests potential upside for investors looking to capitalize on undervalued opportunities. Despite recent share price volatility, Enplas remains profitable with a positive free cash flow and no debt concerns. Earnings are forecasted to grow by 6.71% annually, indicating promising future prospects.

- Delve into the full analysis health report here for a deeper understanding of Enplas.

Understand Enplas' track record by examining our Past report.

Summing It All Up

- Click this link to deep-dive into the 4712 companies within our Undiscovered Gems With Strong Fundamentals screener.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Invest smarter with the free Simply Wall St app providing detailed insights into every stock market around the globe.

Interested In Other Possibilities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Valuation is complex, but we're here to simplify it.

Discover if Enplas might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About TSE:6961

Enplas

Manufactures and sells semiconductor, automobile parts, optical communication devices, and life science related products in Japan and internationally.

Flawless balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|42.8% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|66.0% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|40.8% undervalued

UN

Community Contributor