Advertisement

The external fund manager backed by Berkshire Hathaway's Charlie Munger, Li Lu, makes no bones about it when he says 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. We note that Kaisun Holdings Limited (HKG:8203) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

When Is Debt A Problem?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we think about a company's use of debt, we first look at cash and debt together.

See our latest analysis for Kaisun Holdings

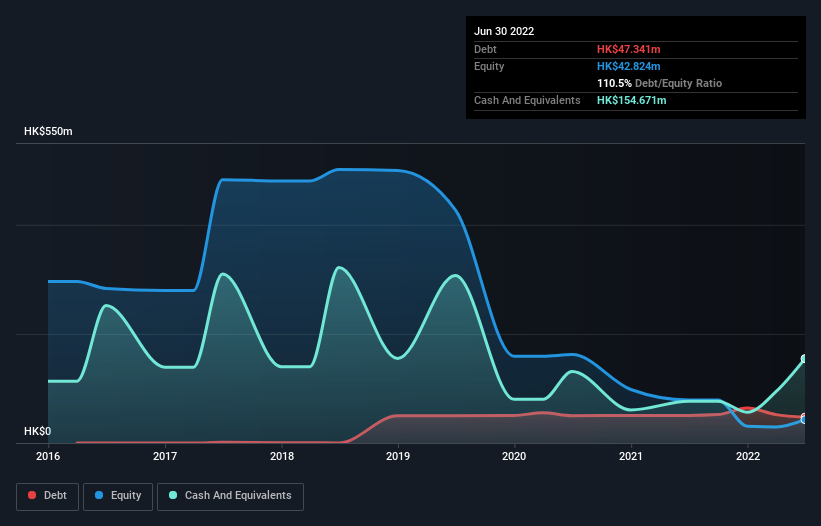

What Is Kaisun Holdings's Debt?

The image below, which you can click on for greater detail, shows that Kaisun Holdings had debt of HK$47.3m at the end of June 2022, a reduction from HK$50.5m over a year. However, it does have HK$154.7m in cash offsetting this, leading to net cash of HK$107.3m.

How Healthy Is Kaisun Holdings' Balance Sheet?

The latest balance sheet data shows that Kaisun Holdings had liabilities of HK$377.9m due within a year, and liabilities of HK$39.8m falling due after that. Offsetting this, it had HK$154.7m in cash and HK$53.1m in receivables that were due within 12 months. So its liabilities total HK$210.0m more than the combination of its cash and short-term receivables.

Given this deficit is actually higher than the company's market capitalization of HK$141.8m, we think shareholders really should watch Kaisun Holdings's debt levels, like a parent watching their child ride a bike for the first time. Hypothetically, extremely heavy dilution would be required if the company were forced to pay down its liabilities by raising capital at the current share price. Given that Kaisun Holdings has more cash than debt, we're pretty confident it can handle its debt, despite the fact that it has a lot of liabilities in total. There's no doubt that we learn most about debt from the balance sheet. But it is Kaisun Holdings's earnings that will influence how the balance sheet holds up in the future. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year Kaisun Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 243%, to HK$241m. That's virtually the hole-in-one of revenue growth!

So How Risky Is Kaisun Holdings?

We have no doubt that loss making companies are, in general, riskier than profitable ones. And in the last year Kaisun Holdings had an earnings before interest and tax (EBIT) loss, truth be told. And over the same period it saw negative free cash outflow of HK$3.0m and booked a HK$32m accounting loss. With only HK$107.3m on the balance sheet, it would appear that its going to need to raise capital again soon. The good news for shareholders is that Kaisun Holdings has dazzling revenue growth, so there's a very good chance it can boost its free cash flow in the years to come. High growth pre-profit companies may well be risky, but they can also offer great rewards. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. Case in point: We've spotted 3 warning signs for Kaisun Holdings you should be aware of, and 1 of them doesn't sit too well with us.

Of course, if you're the type of investor who prefers buying stocks without the burden of debt, then don't hesitate to discover our exclusive list of net cash growth stocks, today.

Valuation is complex, but we're here to simplify it.

Discover if Kaisun Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:8203

Kaisun Holdings

An investment holding company, engages in the mining, exploitation, processing, production, and sale of coal in Hong Kong, the People’s Republic of China, Vietnam, and internationally.

Slight and slightly overvalued.

Market Insights

Advertisement

Community Narratives

Vita Life Sciences Set for a 12.72% Revenue Growth While Tackling Operational Challenges

Fair Value AU$2.42|9.1% undervalued

RO

Community Contributor

Vossloh rides a €500 billion wave to boost growth and earnings in the next decade

Fair Value €78.41|6.3% undervalued

CH

Community Contributor

Intuitive Surgical Will Transform Healthcare with 12% Revenue Growth

Fair Value US$325.55|56.5% overvalued

UN

Community Contributor