Advertisement

- Hong Kong

- /

- Energy Services

- /

- SEHK:3337

Investors Can Find Comfort In Anton Oilfield Services Group's (HKG:3337) Earnings Quality

Shareholders appeared unconcerned with Anton Oilfield Services Group's (HKG:3337) lackluster earnings report last week. We think that the softer headline numbers might be getting counterbalanced by some positive underlying factors.

See our latest analysis for Anton Oilfield Services Group

Examining Cashflow Against Anton Oilfield Services Group's Earnings

In high finance, the key ratio used to measure how well a company converts reported profits into free cash flow (FCF) is the accrual ratio (from cashflow). In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. You could think of the accrual ratio from cashflow as the 'non-FCF profit ratio'.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. Notably, there is some academic evidence that suggests that a high accrual ratio is a bad sign for near-term profits, generally speaking.

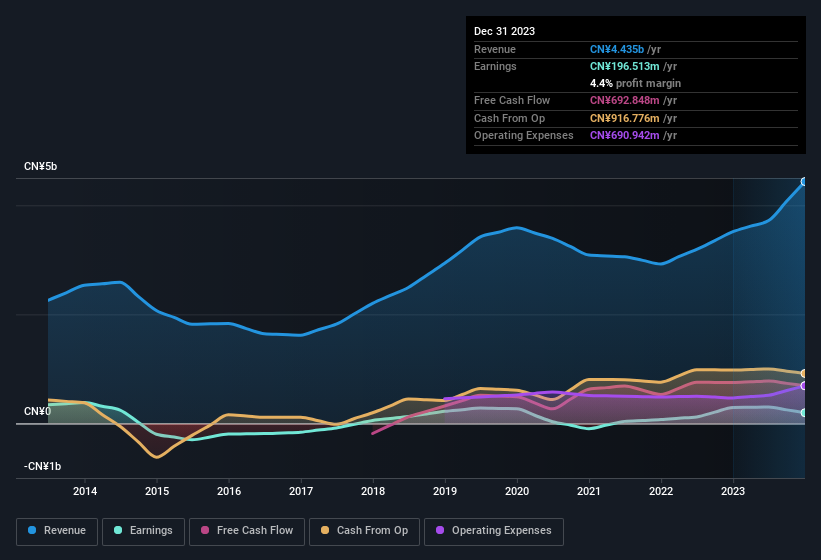

Anton Oilfield Services Group has an accrual ratio of -0.12 for the year to December 2023. That implies it has good cash conversion, and implies that its free cash flow solidly exceeded its profit last year. In fact, it had free cash flow of CN¥693m in the last year, which was a lot more than its statutory profit of CN¥196.5m. Anton Oilfield Services Group did see its free cash flow drop year on year, which is less than ideal, like a Simpson's episode without Groundskeeper Willie.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Anton Oilfield Services Group's Profit Performance

Anton Oilfield Services Group's accrual ratio is solid, and indicates strong free cash flow, as we discussed, above. Based on this observation, we consider it likely that Anton Oilfield Services Group's statutory profit actually understates its earnings potential! On the other hand, its EPS actually shrunk in the last twelve months. Of course, we've only just scratched the surface when it comes to analysing its earnings; one could also consider margins, forecast growth, and return on investment, among other factors. So if you'd like to dive deeper into this stock, it's crucial to consider any risks it's facing. For example, we've discovered 2 warning signs that you should run your eye over to get a better picture of Anton Oilfield Services Group.

This note has only looked at a single factor that sheds light on the nature of Anton Oilfield Services Group's profit. But there are plenty of other ways to inform your opinion of a company. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:3337

Anton Oilfield Services Group

An investment holding company, operates as an integrated oilfield technology services company in the People’s Republic of China, Iraq, and internationally.

Flawless balance sheet with reasonable growth potential.

Similar Companies

Market Insights

Advertisement

Community Narratives

A case for TSXV:USA to reach USD $5.00 - $9.00 (CAD $7.30–$12.29) by 2029.

Fair Value CA$12.29|91.1% undervalued

AG

Community Contributor

DLocal's Future Growth Fueled by 35% Revenue and Profit Margin Boosts

Fair Value US$195.39|94.2% undervalued

WY

Community Contributor

Historically Cheap, but the Margin of Safety Is Still Thin

Fair Value SEK 232.58|13.2% undervalued

MA

Community Contributor