Advertisement

- Hong Kong

- /

- Energy Services

- /

- SEHK:1960

We Think Shareholders Are Less Likely To Approve A Large Pay Rise For TBK & Sons Holdings Limited's (HKG:1960) CEO For Now

Key Insights

- TBK & Sons Holdings will host its Annual General Meeting on 15th of December

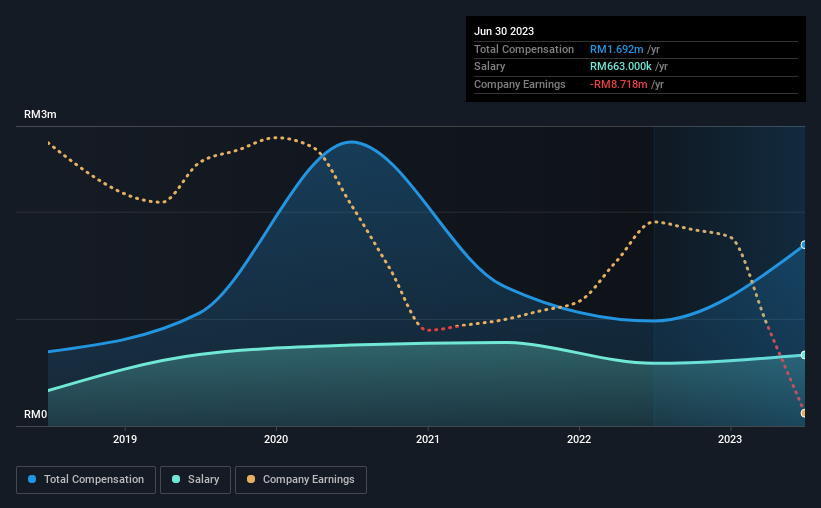

- CEO Han Tan's total compensation includes salary of RM663.0k

- Total compensation is 49% above industry average

- Over the past three years, TBK & Sons Holdings' EPS fell by 29% and over the past three years, the total shareholder return was 71%

The share price of TBK & Sons Holdings Limited (HKG:1960) has increased significantly over the past few years. However, the earnings growth has not kept up with the share price momentum, suggesting that some other factors may be driving the price direction. These concerns will be at the front of shareholders' minds as they go into the AGM coming up on 15th of December. One way that shareholders can influence managerial decisions is through voting on CEO and executive remuneration packages, which studies show could impact company performance. From the data that we gathered, we think that shareholders should hold off on a raise on CEO compensation until performance starts to show some improvement.

See our latest analysis for TBK & Sons Holdings

How Does Total Compensation For Han Tan Compare With Other Companies In The Industry?

According to our data, TBK & Sons Holdings Limited has a market capitalization of HK$360m, and paid its CEO total annual compensation worth RM1.7m over the year to June 2023. That's a notable increase of 73% on last year. We think total compensation is more important but our data shows that the CEO salary is lower, at RM663k.

For comparison, other companies in the Hong Kong Energy Services industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of RM1.1m. Hence, we can conclude that Han Tan is remunerated higher than the industry median.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | RM663k | RM585k | 39% |

| Other | RM1.0m | RM395k | 61% |

| Total Compensation | RM1.7m | RM980k | 100% |

Talking in terms of the industry, salary represented approximately 76% of total compensation out of all the companies we analyzed, while other remuneration made up 24% of the pie. It's interesting to note that TBK & Sons Holdings allocates a smaller portion of compensation to salary in comparison to the broader industry. If total compensation is slanted towards non-salary benefits, it indicates that CEO pay is linked to company performance.

TBK & Sons Holdings Limited's Growth

TBK & Sons Holdings Limited has reduced its earnings per share by 29% a year over the last three years. It saw its revenue drop 55% over the last year.

The decline in EPS is a bit concerning. And the fact that revenue is down year on year arguably paints an ugly picture. So given this relatively weak performance, shareholders would probably not want to see high compensation for the CEO. Although we don't have analyst forecasts, you might want to assess this data-rich visualization of earnings, revenue and cash flow.

Has TBK & Sons Holdings Limited Been A Good Investment?

Most shareholders would probably be pleased with TBK & Sons Holdings Limited for providing a total return of 71% over three years. So they may not be at all concerned if the CEO were to be paid more than is normal for companies around the same size.

In Summary...

Although shareholders would be quite happy with the returns they have earned on their initial investment, earnings have failed to grow and this could mean returns may be hard to keep up. The upcoming AGM will provide shareholders the opportunity to revisit the company’s remuneration policies and evaluate if the board’s judgement and decision-making is aligned with that of the company’s shareholders.

CEO compensation is an important area to keep your eyes on, but we've also need to pay attention to other attributes of the company. That's why we did our research, and identified 3 warning signs for TBK & Sons Holdings (of which 2 are a bit concerning!) that you should know about in order to have a holistic understanding of the stock.

Important note: TBK & Sons Holdings is an exciting stock, but we understand investors may be looking for an unencumbered balance sheet and blockbuster returns. You might find something better in this list of interesting companies with high ROE and low debt.

Valuation is complex, but we're here to simplify it.

Discover if TBK & Sons Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1960

TBK & Sons Holdings

An investment holding company, undertakes civil and structural works in the oil and gas industry in Malaysia and the People’s Republic of China.

Excellent balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

932 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative