Advertisement

- Hong Kong

- /

- Energy Services

- /

- SEHK:1960

TBK & Sons Holdings's (HKG:1960) Earnings Are Growing But Is There More To The Story?

It might be old fashioned, but we really like to invest in companies that make a profit, each and every year. Having said that, sometimes statutory profit levels are not a good guide to ongoing profitability, because some short term one-off factor has impacted profit levels. In this article, we'll look at how useful this year's statutory profit is, when analysing TBK & Sons Holdings (HKG:1960).

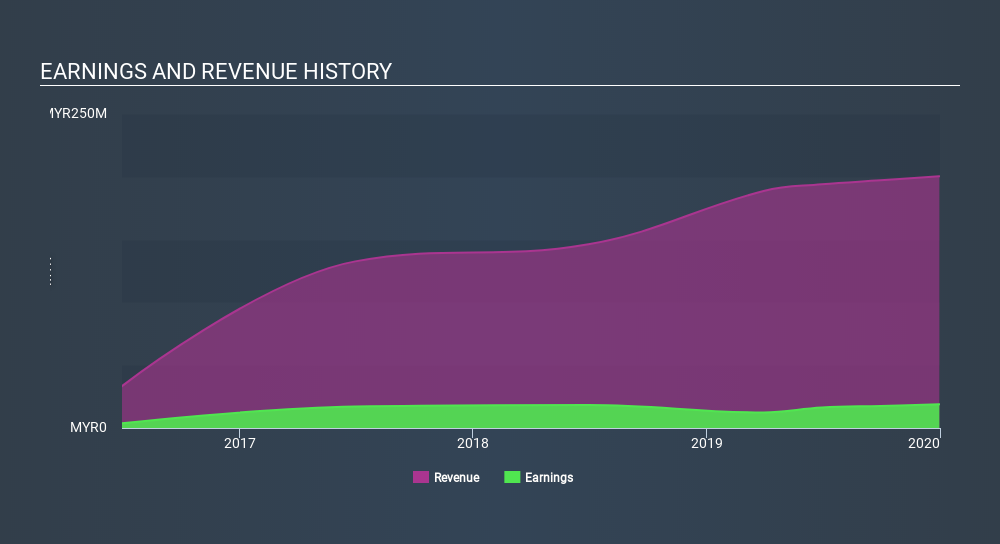

We like the fact that TBK & Sons Holdings made a profit of RM18.8m on its revenue of RM200.4m, in the last year. One positive is that it has grown both its profit and its revenue, over the last few years.

Check out our latest analysis for TBK & Sons Holdings

Importantly, statutory profits are not always the best tool for understanding a company's true earnings power, so it's well worth examining profits in a little more detail. This article will focus on the impact unusual items have had on TBK & Sons Holdings's statutory earnings. Note: we always recommend investors check balance sheet strength. Click here to be taken to our balance sheet analysis of TBK & Sons Holdings.

The Impact Of Unusual Items On Profit

To properly understand TBK & Sons Holdings's profit results, we need to consider the RM8.2m expense attributed to unusual items. It's never great to see unusual items costing the company profits, but on the upside, things might improve sooner rather than later. When we analysed the vast majority of listed companies worldwide, we found that significant unusual items are often not repeated. And that's hardly a surprise given these line items are considered unusual. Assuming those unusual expenses don't come up again, we'd therefore expect TBK & Sons Holdings to produce a higher profit next year, all else being equal.

Our Take On TBK & Sons Holdings's Profit Performance

Because unusual items detracted from TBK & Sons Holdings's earnings over the last year, you could argue that we can expect an improved result in the current quarter. Because of this, we think TBK & Sons Holdings's earnings potential is at least as good as it seems, and maybe even better! Unfortunately, though, its earnings per share actually fell back over the last year. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. You'd be interested to know, that we found 3 warning signs for TBK & Sons Holdings and you'll want to know about these.

Today we've zoomed in on a single data point to better understand the nature of TBK & Sons Holdings's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. For example, many people consider a high return on equity as an indication of favorable business economics, while others like to 'follow the money' and search out stocks that insiders are buying. While it might take a little research on your behalf, you may find this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying to be useful.

Love or hate this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned. Thank you for reading.

About SEHK:1960

TBK & Sons Holdings

An investment holding company, undertakes civil and structural works in the oil and gas industry in Malaysia and the People’s Republic of China.

Excellent balance sheet with low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor