Advertisement

Quite a few insiders have dramatically grown their holdings in Kinetic Development Group Limited (HKG:1277) over the past 12 months. An insider's optimism about the company's prospects is a positive sign.

Although we don't think shareholders should simply follow insider transactions, logic dictates you should pay some attention to whether insiders are buying or selling shares.

See our latest analysis for Kinetic Development Group

Kinetic Development Group Insider Transactions Over The Last Year

The insider Li Zhang made the biggest insider purchase in the last 12 months. That single transaction was for HK$11m worth of shares at a price of HK$1.15 each. So it's clear an insider wanted to buy, at around the current price, which is HK$1.21. That means they have been optimistic about the company in the past, though they may have changed their mind. We do always like to see insider buying, but it is worth noting if those purchases were made at well below today's share price, as the discount to value may have narrowed with the rising price. Happily, the Kinetic Development Group insiders decided to buy shares at close to current prices.

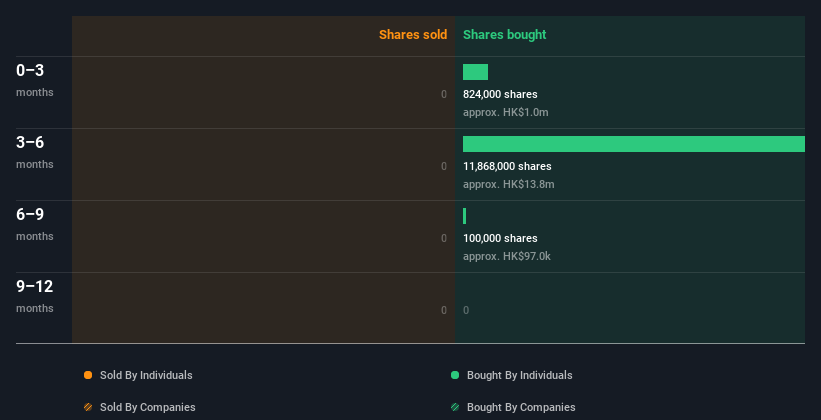

Kinetic Development Group insiders may have bought shares in the last year, but they didn't sell any. The chart below shows insider transactions (by companies and individuals) over the last year. If you want to know exactly who sold, for how much, and when, simply click on the graph below!

Kinetic Development Group is not the only stock that insiders are buying. For those who like to find small cap companies at attractive valuations, this free list of growing companies with recent insider purchasing, could be just the ticket.

Insiders At Kinetic Development Group Have Bought Stock Recently

Over the last three months, we've seen significant insider buying at Kinetic Development Group. Not only was there no selling that we can see, but they collectively bought HK$1.0m worth of shares. That shows some optimism about the company's future.

Insider Ownership

Another way to test the alignment between the leaders of a company and other shareholders is to look at how many shares they own. A high insider ownership often makes company leadership more mindful of shareholder interests. Kinetic Development Group insiders own 74% of the company, currently worth about HK$7.6b based on the recent share price. Most shareholders would be happy to see this sort of insider ownership, since it suggests that management incentives are well aligned with other shareholders.

So What Do The Kinetic Development Group Insider Transactions Indicate?

The recent insider purchases are heartening. We also take confidence from the longer term picture of insider transactions. Along with the high insider ownership, this analysis suggests that insiders are quite bullish about Kinetic Development Group. Nice! So these insider transactions can help us build a thesis about the stock, but it's also worthwhile knowing the risks facing this company. While conducting our analysis, we found that Kinetic Development Group has 1 warning sign and it would be unwise to ignore this.

Of course, you might find a fantastic investment by looking elsewhere. So take a peek at this free list of interesting companies.

For the purposes of this article, insiders are those individuals who report their transactions to the relevant regulatory body. We currently account for open market transactions and private dispositions of direct interests only, but not derivative transactions or indirect interests.

Valuation is complex, but we're here to simplify it.

Discover if Kinetic Development Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1277

Kinetic Development Group

An investment holding company, engages in the extraction and sale of coal products in the People’s Republic of China.

Good value with adequate balance sheet.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|9.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.5% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.4% undervalued

EA

Community Contributor