Advertisement

July 2024 Insights Into Three SEHK Stocks Estimated To Be Undervalued

Simply Wall St

Reviewed by Simply Wall St

Amid a backdrop of mixed global economic signals, the Hong Kong market has shown resilience, with the Hang Seng Index posting modest gains. This stability in an otherwise uncertain environment suggests potential opportunities in undervalued stocks within the region. In assessing what makes a stock particularly appealing during these times, investors might look for companies that demonstrate strong fundamentals such as healthy balance sheets and potential for sustainable growth, which may have been overlooked by the broader market.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

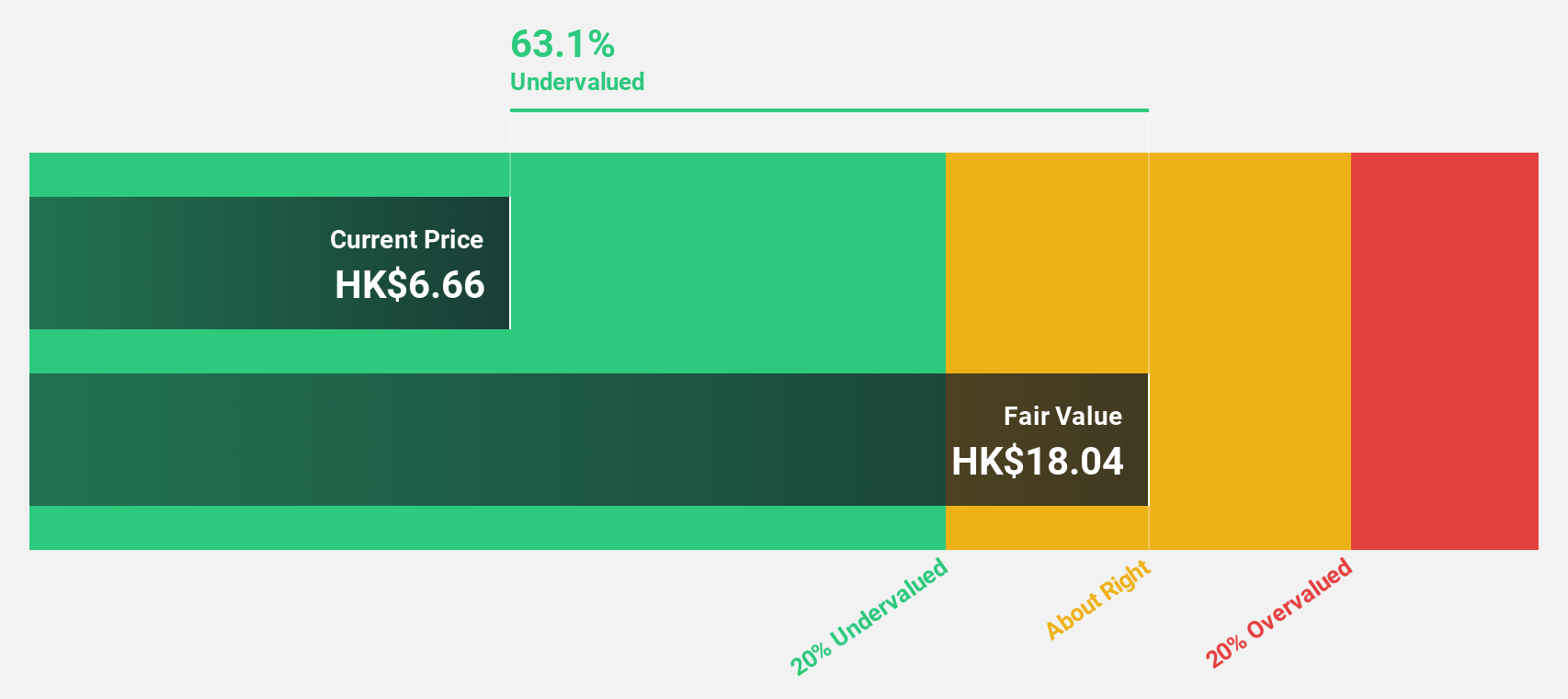

| China Cinda Asset Management (SEHK:1359) | HK$0.66 | HK$1.29 | 48.9% |

| United Energy Group (SEHK:467) | HK$0.31 | HK$0.57 | 46% |

| West China Cement (SEHK:2233) | HK$1.11 | HK$2.16 | 48.6% |

| Super Hi International Holding (SEHK:9658) | HK$13.82 | HK$26.06 | 47% |

| Shanghai INT Medical Instruments (SEHK:1501) | HK$26.10 | HK$48.26 | 45.9% |

| Zijin Mining Group (SEHK:2899) | HK$17.52 | HK$32.07 | 45.4% |

| Genscript Biotech (SEHK:1548) | HK$8.84 | HK$16.26 | 45.6% |

| AK Medical Holdings (SEHK:1789) | HK$4.33 | HK$7.96 | 45.6% |

| Vobile Group (SEHK:3738) | HK$1.17 | HK$2.30 | 49.2% |

| Q Technology (Group) (SEHK:1478) | HK$3.81 | HK$7.30 | 47.8% |

Let's uncover some gems from our specialized screener

COSCO SHIPPING Energy Transportation (SEHK:1138)

Overview: COSCO SHIPPING Energy Transportation Co., Ltd. operates globally, specializing in the transportation of oil, liquefied natural gas (LNG), and chemicals, with a market capitalization of approximately HK$69.01 billion.

Operations: The company primarily generates revenue through the transportation of oil, liquefied natural gas (LNG), and chemicals.

Estimated Discount To Fair Value: 38.1%

COSCO SHIPPING Energy Transportation, priced at HK$9.6, is significantly undervalued with a fair value estimate of HK$15.51, reflecting a 38.1% discount. Despite its high debt levels and unstable dividend history, the company shows robust growth prospects with earnings expected to increase by 24.7% annually, outpacing the Hong Kong market average significantly. Recent corporate actions include reappointing auditors and amending company bylaws to enhance governance, alongside declaring a dividend of RMB 0.35 per share for 2023.

- Insights from our recent growth report point to a promising forecast for COSCO SHIPPING Energy Transportation's business outlook.

- Take a closer look at COSCO SHIPPING Energy Transportation's balance sheet health here in our report.

Global New Material International Holdings (SEHK:6616)

Overview: Global New Material International Holdings Limited engages in the production and sale of pearlescent pigment, functional mica filler, and related products both domestically in the People’s Republic of China and internationally, with a market capitalization of approximately HK$5.17 billion.

Operations: The company generates revenue primarily through its operations in the People’s Republic of China and Korea, with segments reporting revenues of CN¥961.34 million and CN¥103.11 million respectively.

Estimated Discount To Fair Value: 20%

Global New Material International Holdings, valued at HK$4.17, is considered undervalued by more than 20%, with its fair value estimated at HK$5.21. The company's revenue and earnings growth are projected to significantly outpace the Hong Kong market average, with forecasts of 31.1% and 41.85% per year respectively. However, it faces challenges such as shareholder dilution over the past year and a decrease in profit margins from 24.4% to 17.1%.

- Our earnings growth report unveils the potential for significant increases in Global New Material International Holdings' future results.

- Click here and access our complete balance sheet health report to understand the dynamics of Global New Material International Holdings.

China East Education Holdings (SEHK:667)

Overview: China East Education Holdings Limited operates as an investment holding company, offering vocational training education services across the People's Republic of China, with a market capitalization of approximately HK$4.92 billion.

Operations: The company's revenue is primarily generated from New East Culinary Education at CN¥1.87 billion, followed by Wontone Automotive Education at CN¥847.35 million, Xinhua Internet Technology Education at CN¥744.00 million, and smaller contributions from Omick Education of Western Cuisine and Pastry and other segments.

Estimated Discount To Fair Value: 17%

China East Education Holdings, priced at HK$2.26, trades 17% below its estimated fair value of HK$2.72. Its earnings are expected to grow by 20.8% annually, outstripping the Hong Kong market's 11.3%. Revenue growth is also robust at 8.8% per year compared to the market's 7.7%. However, a dividend yield of 8.56% is poorly supported by earnings and cash flows, indicating potential sustainability issues despite strong growth forecasts and recent amendments to its articles of association.

- Our comprehensive growth report raises the possibility that China East Education Holdings is poised for substantial financial growth.

- Dive into the specifics of China East Education Holdings here with our thorough financial health report.

Seize The Opportunity

- Unlock our comprehensive list of 43 Undervalued SEHK Stocks Based On Cash Flows by clicking here.

- Have a stake in these businesses? Integrate your holdings into Simply Wall St's portfolio for notifications and detailed stock reports.

- Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Looking For Alternative Opportunities?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:6616

Global New Material International Holdings

An investment holding company, produces and sells pearlescent pigment, functional mica filler, and related products in the People’s Republic of China and South Korea.

Adequate balance sheet with acceptable track record.

Market Insights

Advertisement

Community Narratives

Suncorp’s Next Chapter: Insurance-Only and Ready to Grow

Fair Value AU$22.83|5.7% undervalued

RO

Community Contributor

Thyssenkrupp Nucera Will Achieve Double-Digit Profits by 2030 Boosted by Hydrogen Growth

Fair Value €14.40|31.6% undervalued

CH

Community Contributor

Tesla’s Nvidia Moment – The AI & Robotics Inflection Point

Fair Value US$384.84|18.0% undervalued

BL

Community Contributor