Advertisement

- Hong Kong

- /

- Diversified Financial

- /

- SEHK:9923

Yeahka Limited's (HKG:9923) Shares Climb 58% But Its Business Is Yet to Catch Up

Yeahka Limited (HKG:9923) shareholders would be excited to see that the share price has had a great month, posting a 58% gain and recovering from prior weakness. Looking back a bit further, it's encouraging to see the stock is up 25% in the last year.

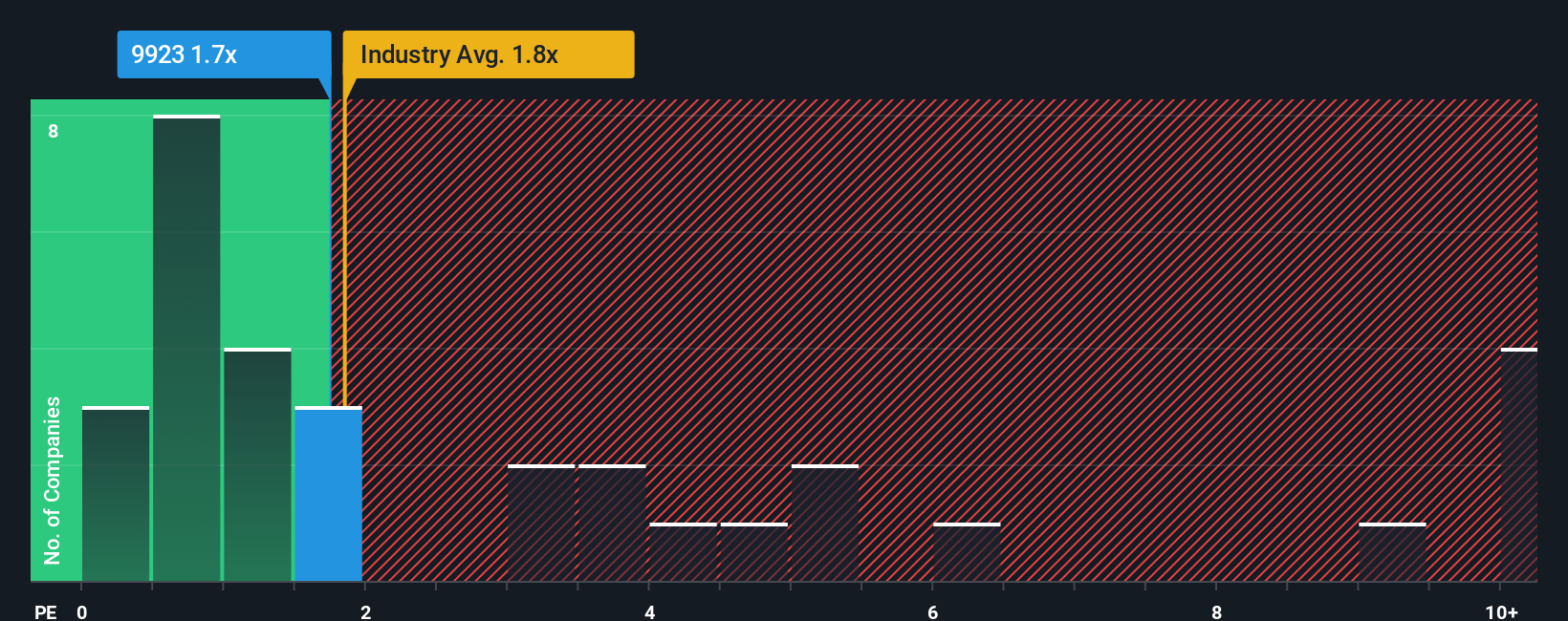

Even after such a large jump in price, you could still be forgiven for feeling indifferent about Yeahka's P/S ratio of 1.7x, since the median price-to-sales (or "P/S") ratio for the Diversified Financial industry in Hong Kong is also close to 1.8x. However, investors might be overlooking a clear opportunity or potential setback if there is no rational basis for the P/S.

View our latest analysis for Yeahka

How Has Yeahka Performed Recently?

Yeahka hasn't been tracking well recently as its declining revenue compares poorly to other companies, which have seen some growth in their revenues on average. Perhaps the market is expecting its poor revenue performance to improve, keeping the P/S from dropping. You'd really hope so, otherwise you're paying a relatively elevated price for a company with this sort of growth profile.

Want the full picture on analyst estimates for the company? Then our free report on Yeahka will help you uncover what's on the horizon.How Is Yeahka's Revenue Growth Trending?

There's an inherent assumption that a company should be matching the industry for P/S ratios like Yeahka's to be considered reasonable.

Retrospectively, the last year delivered a frustrating 22% decrease to the company's top line. Unfortunately, that's brought it right back to where it started three years ago with revenue growth being virtually non-existent overall during that time. So it appears to us that the company has had a mixed result in terms of growing revenue over that time.

Turning to the outlook, the next three years should generate growth of 11% per year as estimated by the seven analysts watching the company. Meanwhile, the rest of the industry is forecast to expand by 14% each year, which is noticeably more attractive.

In light of this, it's curious that Yeahka's P/S sits in line with the majority of other companies. Apparently many investors in the company are less bearish than analysts indicate and aren't willing to let go of their stock right now. These shareholders may be setting themselves up for future disappointment if the P/S falls to levels more in line with the growth outlook.

The Key Takeaway

Yeahka appears to be back in favour with a solid price jump bringing its P/S back in line with other companies in the industry It's argued the price-to-sales ratio is an inferior measure of value within certain industries, but it can be a powerful business sentiment indicator.

When you consider that Yeahka's revenue growth estimates are fairly muted compared to the broader industry, it's easy to see why we consider it unexpected to be trading at its current P/S ratio. At present, we aren't confident in the P/S as the predicted future revenues aren't likely to support a more positive sentiment for long. A positive change is needed in order to justify the current price-to-sales ratio.

You need to take note of risks, for example - Yeahka has 2 warning signs (and 1 which is significant) we think you should know about.

If you're unsure about the strength of Yeahka's business, why not explore our interactive list of stocks with solid business fundamentals for some other companies you may have missed.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:9923

Yeahka

An investment holding company, provides payment and business services to merchants and consumers in the People’s Republic of China.

Reasonable growth potential with proven track record.

Similar Companies

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$646.30|0% overvalued

AN

Based on Analyst Price Targets