- Hong Kong

- /

- Diversified Financial

- /

- SEHK:9923

July 2024 Insights Into Three SEHK Stocks Estimated As Undervalued

Reviewed by Simply Wall St

As global markets experience varying levels of performance, with notable shifts in indices like the Russell 2000 and S&P 500, investors are keenly watching for opportunities. The Hong Kong market, reflecting a blend of resilience and challenges amid these global trends, presents unique investment avenues in potentially undervalued stocks that could be poised for adjustment. In such an environment, discerning investors might find that stocks deemed undervalued according to fundamental analysis could represent compelling opportunities for portfolio diversification.

Top 10 Undervalued Stocks Based On Cash Flows In Hong Kong

| Name | Current Price | Fair Value (Est) | Discount (Est) |

| China Resources Mixc Lifestyle Services (SEHK:1209) | HK$24.65 | HK$47.49 | 48.1% |

| China Cinda Asset Management (SEHK:1359) | HK$0.68 | HK$1.29 | 47.4% |

| Zhaojin Mining Industry (SEHK:1818) | HK$15.72 | HK$30.33 | 48.2% |

| Zijin Mining Group (SEHK:2899) | HK$16.96 | HK$32.26 | 47.4% |

| Super Hi International Holding (SEHK:9658) | HK$13.72 | HK$25.78 | 46.8% |

| West China Cement (SEHK:2233) | HK$1.16 | HK$2.15 | 46.2% |

| BYD (SEHK:1211) | HK$239.80 | HK$462.54 | 48.2% |

| Mobvista (SEHK:1860) | HK$2.02 | HK$3.72 | 45.7% |

| Vobile Group (SEHK:3738) | HK$1.26 | HK$2.32 | 45.6% |

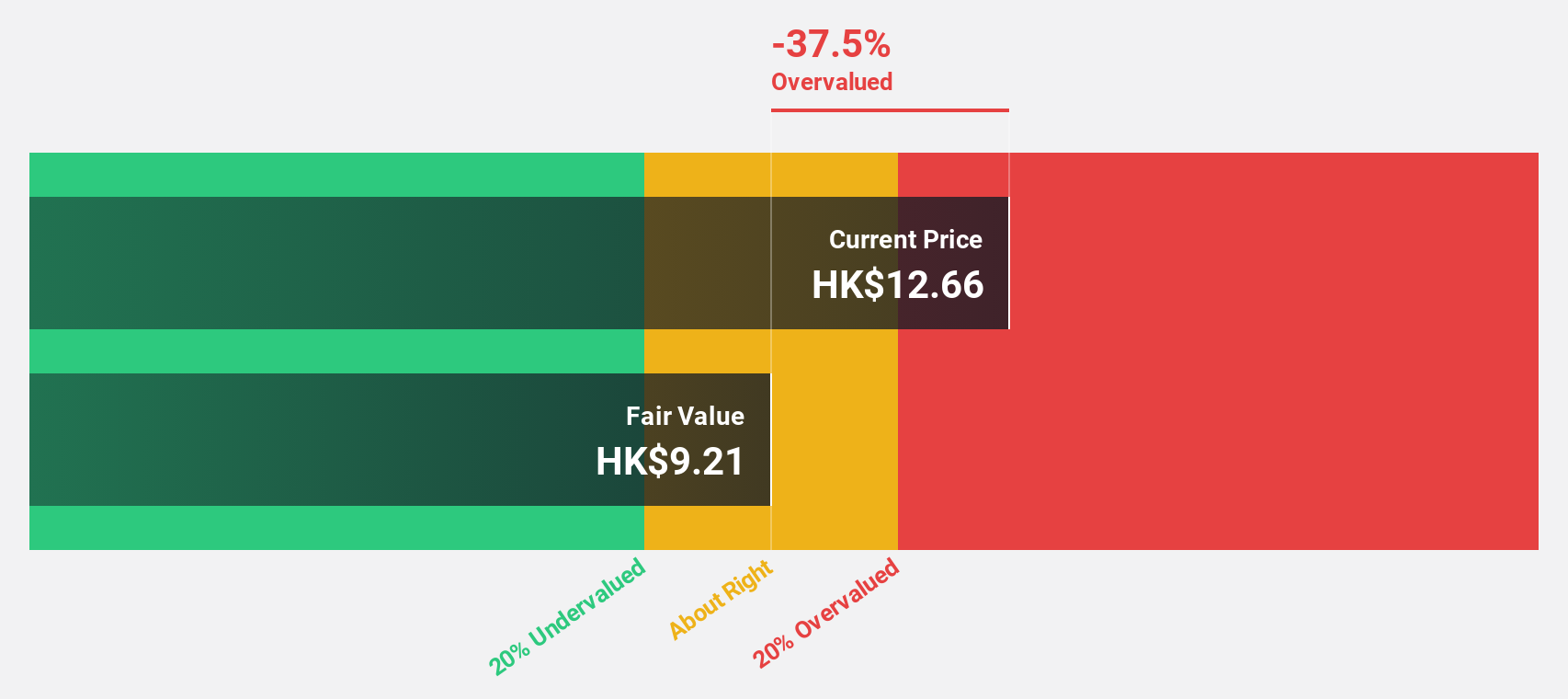

| Kingdee International Software Group (SEHK:268) | HK$6.35 | HK$12.66 | 49.8% |

Let's take a closer look at a couple of our picks from the screened companies.

AK Medical Holdings (SEHK:1789)

Overview: AK Medical Holdings Limited is an investment holding company that specializes in designing, developing, producing, and marketing orthopedic joint implants and related products both in China and internationally, with a market cap of approximately HK$5.26 billion.

Operations: The company generates revenue primarily through the sale of orthopedic implants, totaling CN¥993.59 million in China and CN¥152.49 million in the United Kingdom.

Estimated Discount To Fair Value: 41.2%

AK Medical Holdings is recognized for its robust growth prospects, with earnings expected to increase significantly over the next three years, outpacing the Hong Kong market's average. Currently trading at HK$4.69, the stock is considered undervalued by 41.2% against a fair value estimate of HK$7.98 based on discounted cash flow analysis. Despite a recent dividend decrease and board changes, its forecasted low Return on Equity of 13.7% in three years tempers enthusiasm slightly.

- Our expertly prepared growth report on AK Medical Holdings implies its future financial outlook may be stronger than recent results.

- Navigate through the intricacies of AK Medical Holdings with our comprehensive financial health report here.

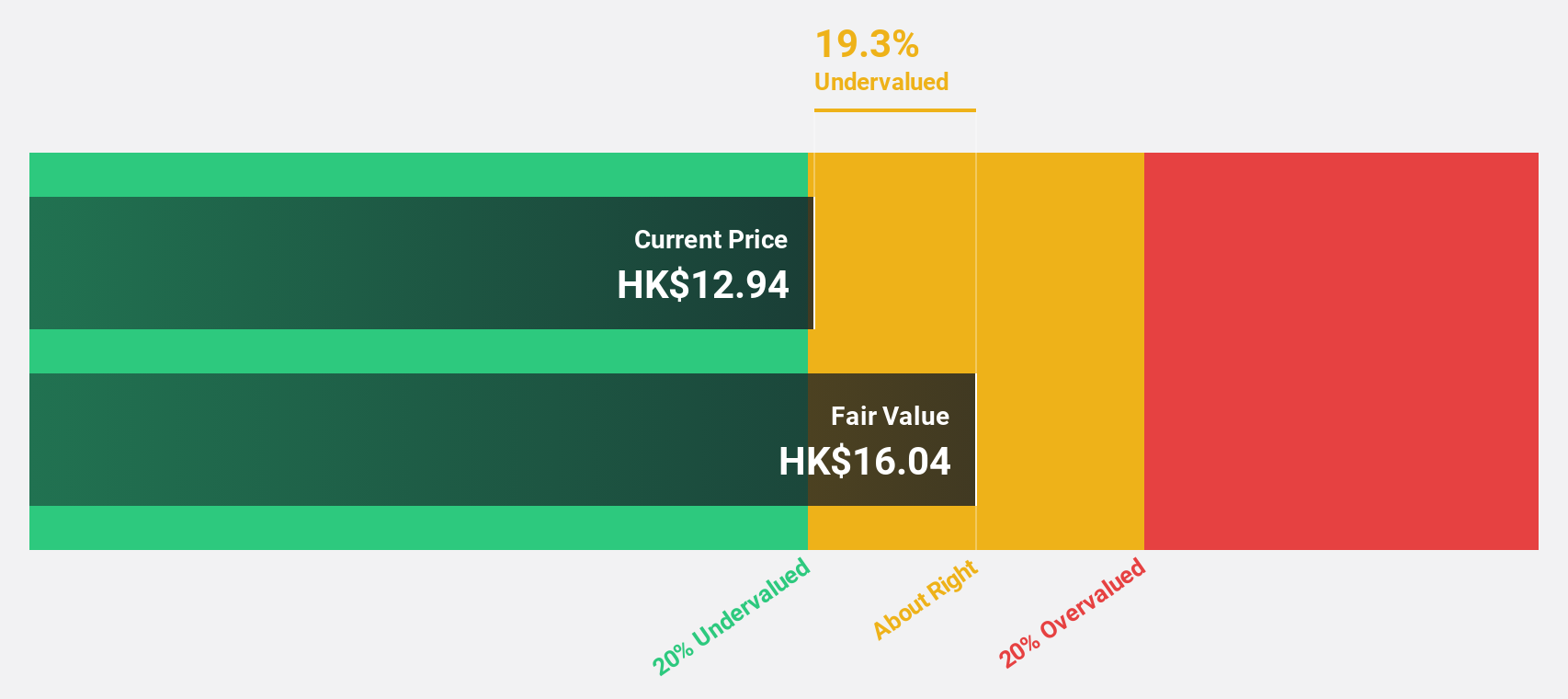

ESR Group (SEHK:1821)

Overview: ESR Group Limited operates in logistics real estate development, leasing, and management across regions including Hong Kong, China, Japan, South Korea, Australia, New Zealand, Southeast Asia, India, and Europe with a market cap of approximately HK$51.23 billion.

Operations: The company's revenue is derived mainly from fund management, which generated HK$774.64 million, and new economy development, contributing HK$105.48 million.

Estimated Discount To Fair Value: 34.4%

ESR Group Limited, currently priced at HK$12.16, appears undervalued by 34.4% compared to our fair value estimate of HK$18.53, reflecting potential underpricing based on discounted cash flow (DCF) analysis. Despite a significant drop in profit margins from 54.8% to 23.9%, earnings are expected to grow by 26.3% annually, outstripping the Hong Kong market's forecast of 11.4%. However, its revenue growth projection of 9.6% lags behind the desired rate of over 20%, and one-off items have impacted its financial results negatively.

- The growth report we've compiled suggests that ESR Group's future prospects could be on the up.

- Click to explore a detailed breakdown of our findings in ESR Group's balance sheet health report.

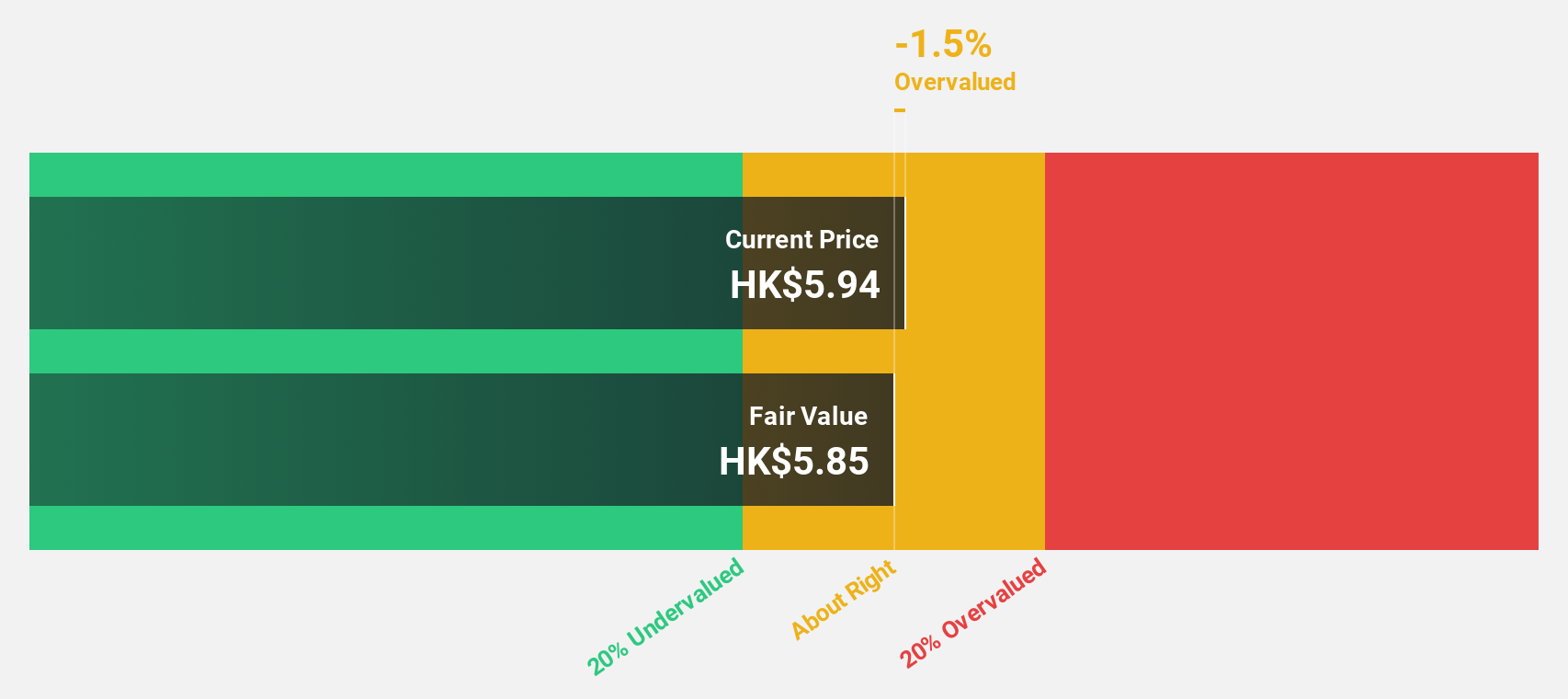

Yeahka (SEHK:9923)

Overview: Yeahka Limited, operating in the People’s Republic of China, is an investment holding company that offers payment and business services to merchants and consumers, with a market capitalization of approximately HK$4.65 billion.

Operations: The company generates CN¥3.95 billion in revenue from its business services segment.

Estimated Discount To Fair Value: 18.7%

Yeahka Limited, trading at HK$10.86, is positioned below its calculated fair value of HK$13.36, indicating an 18.7% undervaluation. Despite a decrease in profit margins from 4.5% to 0.3%, the company's earnings are projected to surge by 51.51% annually, significantly outpacing the Hong Kong market growth rate of 11.4%. Recent executive changes could bolster its fintech sector with Ms. Liang's appointment potentially enhancing risk management and commercial capabilities in its digital ecosystem.

- According our earnings growth report, there's an indication that Yeahka might be ready to expand.

- Get an in-depth perspective on Yeahka's balance sheet by reading our health report here.

Summing It All Up

- Unlock our comprehensive list of 41 Undervalued SEHK Stocks Based On Cash Flows by clicking here.

- Are any of these part of your asset mix? Tap into the analytical power of Simply Wall St's portfolio to get a 360-degree view on how they're shaping up.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:9923

Yeahka

An investment holding company, provides payment and business services to merchants and consumers in the People’s Republic of China.

Undervalued with reasonable growth potential.