Advertisement

- Hong Kong

- /

- Capital Markets

- /

- SEHK:290

GoFintech Quantum Innovation (SEHK:290): Profitability Achieved, One-Off Gain Sparks Margin Sustainability Debate

Simply Wall St

Reviewed by Simply Wall St

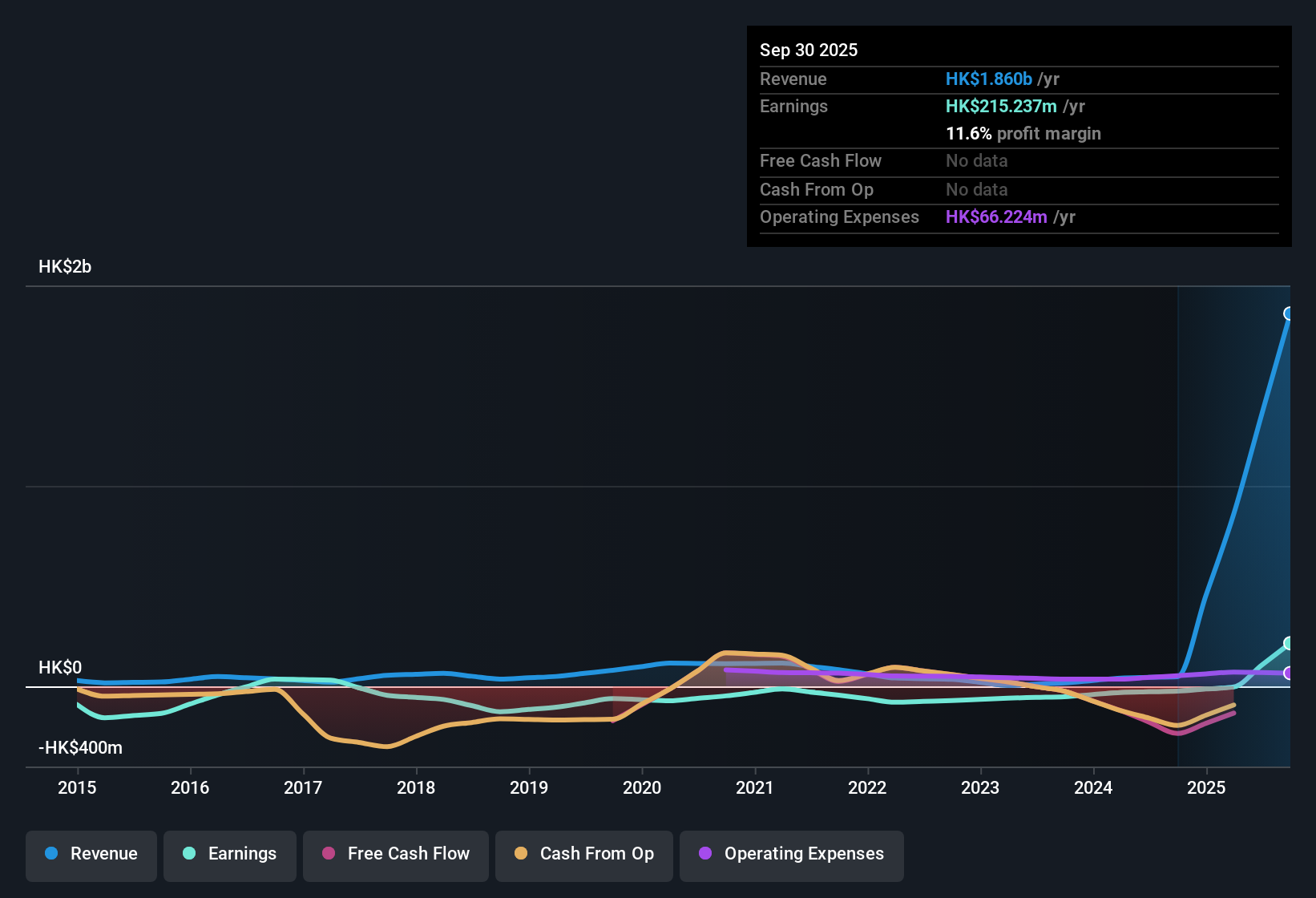

GoFintech Quantum Innovation (SEHK:290) just published its H1 2026 results, reporting revenue of HK$838.9 million and basic EPS of HK$0.001213. Looking back, the company has seen revenue grow from HK$21.3 million in H1 2025 to HK$838.9 million in H2 2025, with basic EPS turning from negative to positive over these periods. With annualized earnings growth of 44.8% over the past five years and a recent transition to profitability, investors are watching to see if margins will hold up given the impact of one-off items this past year.

See our full analysis for GoFintech Quantum Innovation.Next, we will see how the latest financial figures match up against the major themes in the market narrative. Some themes may be confirmed, while others could face significant questions.

Curious how numbers become stories that shape markets? Explore Community Narratives

One-Off Gain Lifts Net Income

- Trailing 12-month net income reached HK$215.2 million. This figure includes a significant HK$188.0 million one-off gain, so core profitability may not be as strong if this non-recurring item is excluded.

- The latest annualized profit growth of 44.8% highlights impressive momentum. However, consensus narrative analysis points out that such rapid profit acceleration may be unsustainable in coming periods if similar one-off gains do not recur.

- Consensus narrative notes management faces higher expectations after this exceptional gain, and future results will be scrutinized for repeatability.

- Recent numbers underscore the importance of distinguishing underlying business trends from temporary windfalls, as a large one-off can mask true margin progress or setbacks.

- To see how bulls and bears interpret margin sustainability, check out the full range of consensus opinion in our community narrative resource. 📊 Read the full GoFintech Quantum Innovation Consensus Narrative.

Premium Price-to-Earnings Signals High Expectations

- GoFintech’s Price-to-Earnings ratio stands at 94.7x. This is far above both the peer average of 69.2x and the Hong Kong Capital Markets industry average of 20.9x, indicating investors are paying a steep premium for current and future profits.

- Prevailing market analysis sees this level as a confidence marker in GoFintech’s growth trajectory, but also flags that the premium makes shares particularly sensitive to any disappointment in profitability trends.

- At HK$2.24 per share, even moderate misses in future net income could prompt outsized price swings because of the lofty earnings multiple.

- Bulls may find optimism in the valuation, but the current premium means upside relies heavily on sustained improvements beyond one-off gains.

Dilution and Ownership: Navigating Recent Changes

- Shareholders experienced dilution during the past year, reducing proportional ownership per share despite the company turning profitable.

- Consensus narrative draws attention to this dilution risk, emphasizing that while profitability is a milestone, new or existing investors should weigh the impact of recent and potential future equity raises on their long-term returns.

- The magnitude of dilution, seen alongside margin shifts, sets a different investment calculus for those prioritizing per-share growth.

- This dynamic forces investors to examine not just headline profit, but how it translates into actual shareholder value in a changing capital structure.

Next Steps

Don't just look at this quarter; the real story is in the long-term trend. We've done an in-depth analysis on GoFintech Quantum Innovation's growth and its valuation to see if today's price is a bargain. Add the company to your watchlist or portfolio now so you don't miss the next big move.

See What Else Is Out There

GoFintech Quantum Innovation’s premium valuation and reliance on one-off gains signal that core earnings strength and long-term margin growth remain unproven. If you’d prefer companies with more attractive pricing and fundamentals underpinning their potential, zero in on these 921 undervalued stocks based on cash flows to discover investment ideas with stronger value credentials today.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:290

GoFintech Quantum Innovation

An investment holding company, provides securities and insurance brokerage, equity investment, asset management, margin and corporate finance, money lending, and supply chain operation services in Hong Kong and the People’s Republic of China.

Adequate balance sheet with questionable track record.

Market Insights

Advertisement

Community Narratives

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value US$60|98.4% undervalued

TH

Community Contributor

The Indispensable Artery for a New North American Economy

Fair Value CA$132.87|0.7% overvalued

TI

Community Contributor

Recently Updated Narratives

CO

composite32 on Astor Enerji ·

Astor Enerji will surge with a fair value of $140.43 in the next 3 years

Fair Value:₺140.4335.5% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

RE

RecMag on Proximus ·

Proximus: The State-Backed Backup Plan with 7% Gross Yield and 15% Currency Upside.

Fair Value:€17.1356.7% undervalued

30 followersusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

AG

Agricola on IMPACT Silver ·

A case for for IMPACT Silver Corp (TSXV:IPT) to reach USD $4.52 (CAD $6.16) in 2026 (23 bagger in 1 year) and USD $5.76 (CAD $7.89) by 2030

Fair Value:CA$7.8996.2% undervalued

1 followerusers have followed this narrative

0 commentsusers have commented on this narrative

0 likesusers have liked this narrative

Popular Narratives

TH

TheWallstreetKing on MicroVision ·

MicroVision will explode future revenue by 380.37% with a vision towards success

Fair Value:US$6098.4% undervalued

101 followersusers have followed this narrative

10 commentsusers have commented on this narrative

20 likesusers have liked this narrative

OS

oscargarcia on Alphabet ·

The company that turned a verb into a global necessity and basically runs the modern internet, digital ads, smartphones, maps, and AI.

Fair Value:US$3405.8% undervalued

139 followersusers have followed this narrative

6 commentsusers have commented on this narrative

18 likesusers have liked this narrative

AN

AnalystConsensusTarget on NVIDIA ·

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Fair Value:US$250.3929.3% undervalued

931 followersusers have followed this narrative

6 commentsusers have commented on this narrative

23 likesusers have liked this narrative