In the wake of recent U.S. election results and a subsequent rally in major stock indices, global markets are witnessing heightened investor optimism fueled by expectations of economic growth and regulatory changes. As investors navigate this evolving landscape, identifying growth stocks with high insider ownership can be particularly appealing, as such ownership often signals strong confidence from those most familiar with the company's prospects.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| On Holding (NYSE:ONON) | 31% | 29.7% |

| GPS Participações e Empreendimentos (BOVESPA:GGPS3) | 24% | 38.3% |

| Seojin SystemLtd (KOSDAQ:A178320) | 31.1% | 49.1% |

| Pharma Mar (BME:PHM) | 11.8% | 56.4% |

| Findi (ASX:FND) | 34.8% | 64.8% |

| Alkami Technology (NasdaqGS:ALKT) | 11.2% | 98.6% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.6% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

Here's a peek at a few of the choices from the screener.

Ambu (CPSE:AMBU B)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Ambu A/S is a medical technology company that develops, produces, and sells medical devices to hospitals, clinics, and rescue services worldwide with a market cap of DKK31.59 billion.

Operations: The company's revenue primarily comes from its Disposable Medical Products segment, which generated DKK5.39 billion.

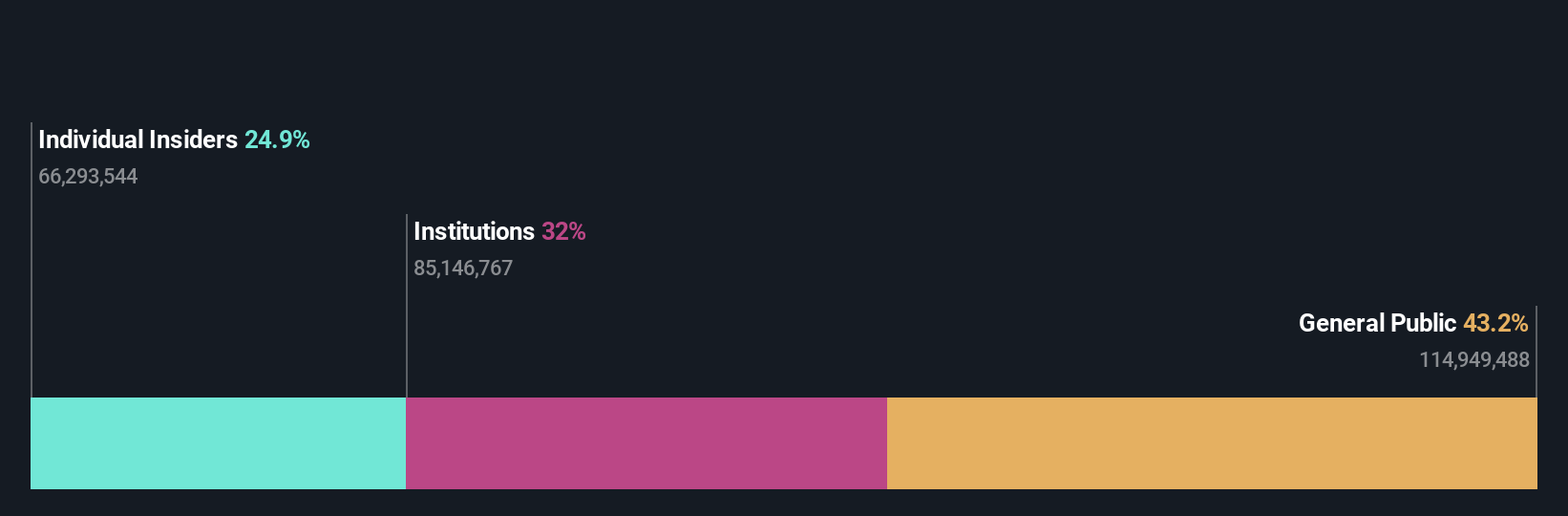

Insider Ownership: 24.9%

Revenue Growth Forecast: 11.1% p.a.

Ambu shows a mix of growth potential and challenges. Despite recent insider buying, volumes were not substantial. Earnings are forecast to grow significantly at 32% annually, outpacing the Danish market's 11.7%. However, revenue growth is expected to be moderate at 11.1%. Recent earnings reports show improved annual sales but a fourth-quarter net loss due to one-off items. The company trades below its estimated fair value but has faced share price volatility recently.

- Click here and access our complete growth analysis report to understand the dynamics of Ambu.

- Our valuation report here indicates Ambu may be overvalued.

Lianlian DigiTech (SEHK:2598)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Lianlian DigiTech Co., Ltd. offers digital payment and value-added services to small and midsized merchants and enterprises in China, with a market cap of HK$10.15 billion.

Operations: The company's revenue is derived from Global Payment (CN¥722.95 million), Domestic Payment (CN¥309.92 million), and Value-Added Services (CN¥153.01 million).

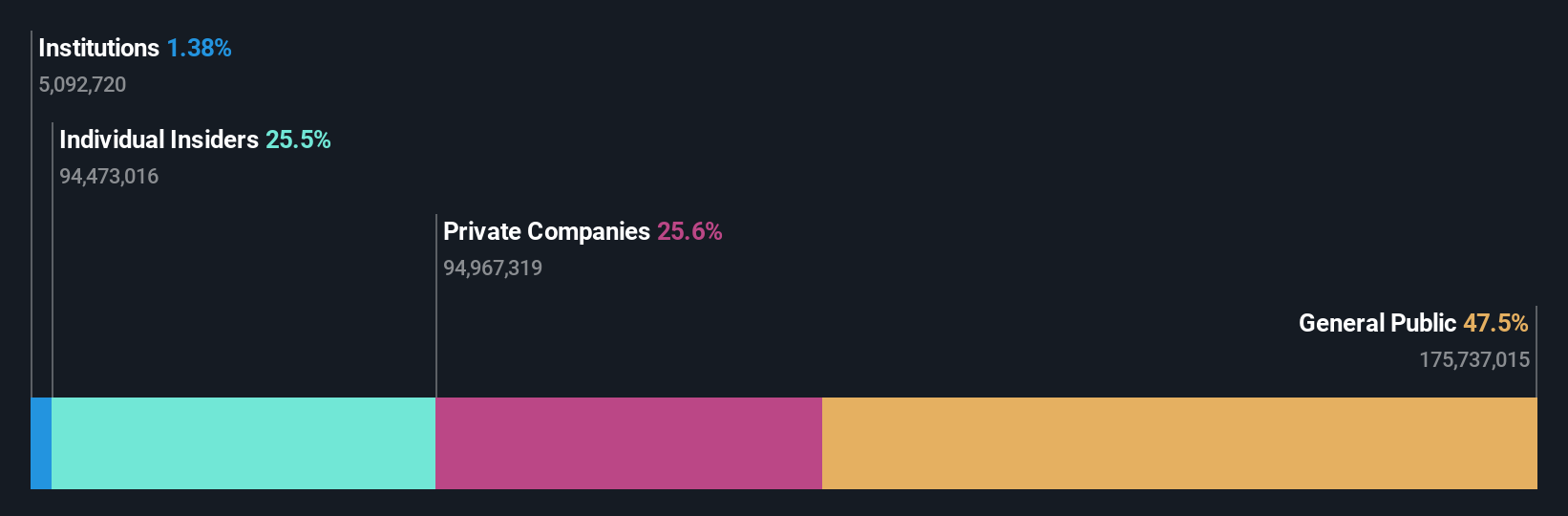

Insider Ownership: 19.7%

Revenue Growth Forecast: 18.9% p.a.

Lianlian DigiTech demonstrates growth potential with its revenue for H1 2024 increasing to CNY 617.39 million from CNY 440.59 million a year earlier, although it remains unprofitable with a net loss of CNY 351.29 million. The company is expected to become profitable within three years, with earnings forecasted to grow by 95.65% annually, surpassing the Hong Kong market's average growth rate. Despite trading below analyst price targets, no significant insider trading activity was reported recently.

- Click here to discover the nuances of Lianlian DigiTech with our detailed analytical future growth report.

- In light of our recent valuation report, it seems possible that Lianlian DigiTech is trading beyond its estimated value.

Jiangsu Canlon Building Materials (SZSE:300715)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Jiangsu Canlon Building Materials Co., Ltd. (SZSE:300715) operates in the building materials industry with a market capitalization of CN¥2.92 billion.

Operations: I'm sorry, but it appears that the revenue segment information is missing from the text provided. If you can supply those details, I would be happy to help summarize them for you.

Insider Ownership: 27.2%

Revenue Growth Forecast: 16.7% p.a.

Jiangsu Canlon Building Materials faces challenges with declining revenue, reporting CNY 1.81 billion in sales for the first nine months of 2024, down from CNY 2.08 billion a year ago, and a net loss of CNY 32.15 million. Despite this, it is expected to become profitable within three years with earnings growth forecasted at 115.74% annually. The company trades at good value compared to peers but has low return on equity projections and insufficient debt coverage by operating cash flow.

- Dive into the specifics of Jiangsu Canlon Building Materials here with our thorough growth forecast report.

- In light of our recent valuation report, it seems possible that Jiangsu Canlon Building Materials is trading behind its estimated value.

Seize The Opportunity

- Reveal the 1519 hidden gems among our Fast Growing Companies With High Insider Ownership screener with a single click here.

- Got skin in the game with these stocks? Elevate how you manage them by using Simply Wall St's portfolio, where intuitive tools await to help optimize your investment outcomes.

- Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300715

Jiangsu Canlon Building Materials

Jiangsu Canlon Building Materials Co., Ltd.

Reasonable growth potential and fair value.