As global markets react to the recent U.S. election results, major indices like the S&P 500 and Nasdaq Composite have reached record highs, driven by investor optimism over potential tax cuts and deregulation under a new administration. Amid this backdrop of economic anticipation, growth companies with high insider ownership are drawing attention for their potential resilience and alignment of interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership

| Name | Insider Ownership | Earnings Growth |

| On Holding (NYSE:ONON) | 31% | 29.7% |

| GPS Participações e Empreendimentos (BOVESPA:GGPS3) | 24% | 38.3% |

| Seojin SystemLtd (KOSDAQ:A178320) | 31.1% | 49.1% |

| Pharma Mar (BME:PHM) | 11.8% | 56.4% |

| Findi (ASX:FND) | 34.8% | 64.8% |

| Alkami Technology (NasdaqGS:ALKT) | 11.2% | 98.6% |

| EHang Holdings (NasdaqGM:EH) | 32.8% | 81.4% |

| Credo Technology Group Holding (NasdaqGS:CRDO) | 13.9% | 95% |

| Brightstar Resources (ASX:BTR) | 16.2% | 84.6% |

| UTI (KOSDAQ:A179900) | 33.1% | 134.6% |

Let's uncover some gems from our specialized screener.

Al Masane Al Kobra Mining (SASE:1322)

Simply Wall St Growth Rating: ★★★★★☆

Overview: Al Masane Al Kobra Mining Company operates in the Kingdom of Saudi Arabia, focusing on the production of non-ferrous metal ores and precious metals, with a market cap of SAR6.12 billion.

Operations: The company's revenue segments comprise SAR353.54 million from Al Masane Mine and SAR190.02 million from Mount Guyan Mine.

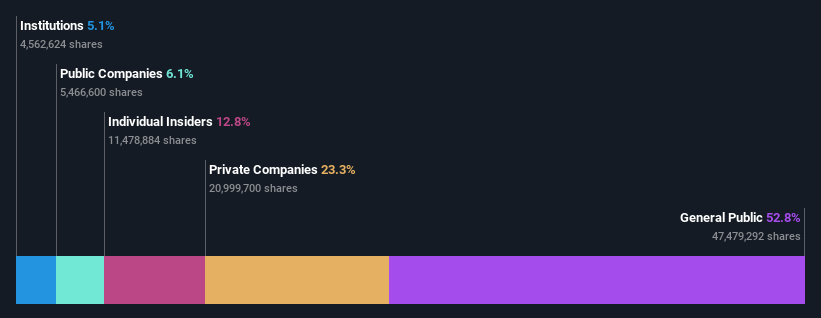

Insider Ownership: 12.8%

Earnings Growth Forecast: 41.4% p.a.

Al Masane Al Kobra Mining's recent earnings report highlights significant growth, with third-quarter sales reaching SAR 215.96 million, nearly doubling from a year ago. Net income surged to SAR 59.75 million, reflecting strong operational performance. The company's earnings are forecast to grow at an impressive rate of 41.41% annually, outpacing the broader Saudi Arabian market's growth expectations. However, its dividend yield of 2.33% is not well covered by free cash flows, indicating potential sustainability concerns despite robust insider ownership levels supporting long-term alignment with shareholders' interests.

- Navigate through the intricacies of Al Masane Al Kobra Mining with our comprehensive analyst estimates report here.

- Our valuation report unveils the possibility Al Masane Al Kobra Mining's shares may be trading at a premium.

Sichuan Shudao Equipment & TechnologyLtd (SZSE:300540)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Sichuan Shudao Equipment & Technology Co., Ltd. operates in the manufacturing sector, focusing on equipment and technology solutions, with a market cap of CN¥4.40 billion.

Operations: The company's revenue is primarily derived from its General Equipment Manufacturing segment, which generated CN¥818.07 million.

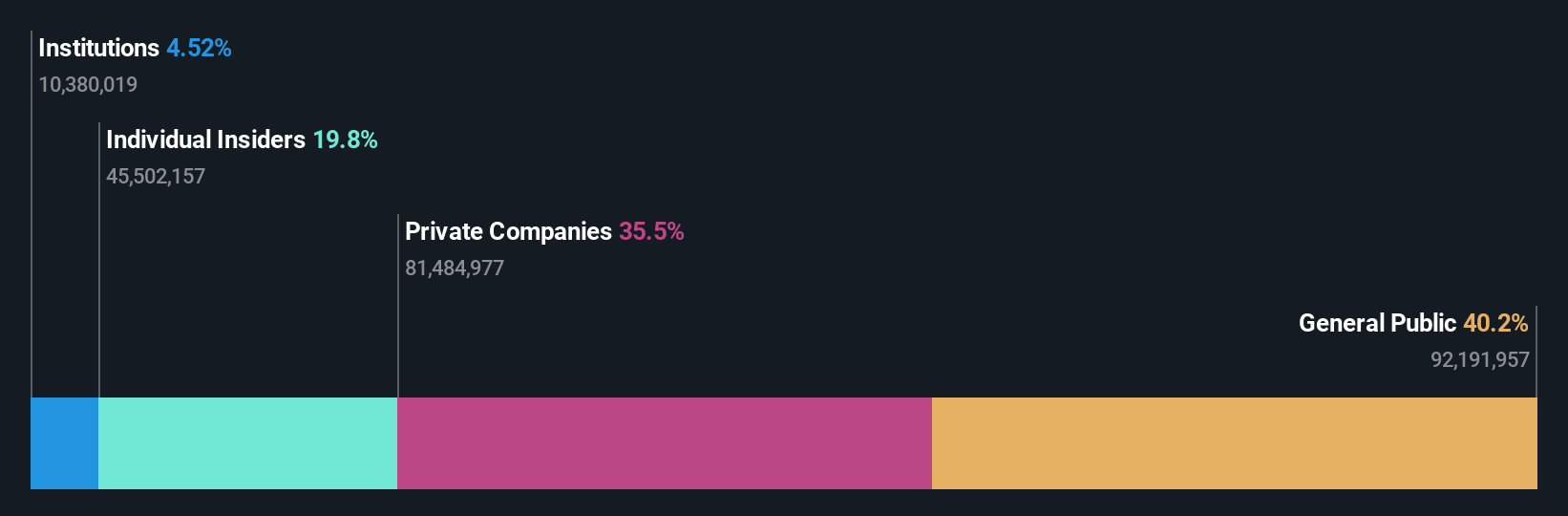

Insider Ownership: 19.8%

Earnings Growth Forecast: 41.9% p.a.

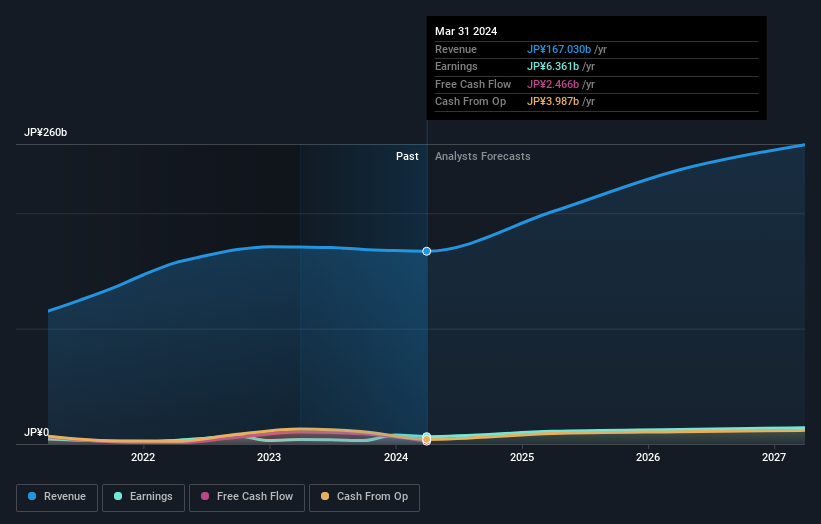

Sichuan Shudao Equipment & Technology's recent earnings report shows robust growth, with sales rising to CNY 496.7 million from CNY 346.98 million a year ago, and net income increasing to CNY 23.19 million from CNY 13.87 million. The company's earnings are expected to grow significantly at over 41% annually, surpassing the broader Chinese market's growth expectations, though its return on equity is forecasted to remain low at 8.1%, and share price volatility persists.

- Delve into the full analysis future growth report here for a deeper understanding of Sichuan Shudao Equipment & TechnologyLtd.

- The valuation report we've compiled suggests that Sichuan Shudao Equipment & TechnologyLtd's current price could be inflated.

UT GroupLtd (TSE:2146)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: UT Group Co., Ltd. is involved in the dispatch and outsourcing of permanent employees across various sectors including manufacturing, design and development, and construction in Japan, with a market cap of ¥105.08 billion.

Operations: The company's revenue segments include Area Business at ¥66.39 billion, Vietnam Business at ¥11.86 billion, Solution Business at ¥18.89 billion, and Manufacturing Business (Excluding Solution Business) at ¥64.78 billion.

Insider Ownership: 22.7%

Earnings Growth Forecast: 13% p.a.

UT Group Ltd. demonstrates strong growth potential with earnings having increased by 153.5% over the past year and forecasted to grow at 12.99% annually, outpacing the JP market's expected growth rates. The company's price-to-earnings ratio of 9.1x suggests it is trading at a good value compared to peers, although recent dividend guidance was revised downward from ¥164.81 to ¥102.66 per share, reflecting potential cash flow concerns despite high insider ownership stability.

- Click to explore a detailed breakdown of our findings in UT GroupLtd's earnings growth report.

- Our expertly prepared valuation report UT GroupLtd implies its share price may be lower than expected.

Seize The Opportunity

- Navigate through the entire inventory of 1519 Fast Growing Companies With High Insider Ownership here.

- Already own these companies? Bring clarity to your investment decisions by linking up your portfolio with Simply Wall St, where you can monitor all the vital signs of your stocks effortlessly.

- Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Contemplating Other Strategies?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SZSE:300540

Sichuan Shudao Equipment & TechnologyLtd

Sichuan Shudao Equipment & Technology Co.,Ltd.

Reasonable growth potential with adequate balance sheet.