Advertisement

- Hong Kong

- /

- Consumer Services

- /

- SEHK:6966

Here's What's Concerning About China Wan Tong Yuan (Holdings)'s (HKG:6966) Returns On Capital

What are the early trends we should look for to identify a stock that could multiply in value over the long term? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Put simply, these types of businesses are compounding machines, meaning they are continually reinvesting their earnings at ever-higher rates of return. However, after investigating China Wan Tong Yuan (Holdings) (HKG:6966), we don't think it's current trends fit the mold of a multi-bagger.

Understanding Return On Capital Employed (ROCE)

If you haven't worked with ROCE before, it measures the 'return' (pre-tax profit) a company generates from capital employed in its business. Analysts use this formula to calculate it for China Wan Tong Yuan (Holdings):

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

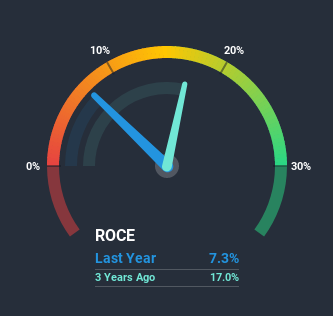

0.073 = CN¥17m ÷ (CN¥253m - CN¥18m) (Based on the trailing twelve months to December 2020).

Thus, China Wan Tong Yuan (Holdings) has an ROCE of 7.3%. In absolute terms, that's a low return but it's around the Consumer Services industry average of 7.7%.

View our latest analysis for China Wan Tong Yuan (Holdings)

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you're interested in investigating China Wan Tong Yuan (Holdings)'s past further, check out this free graph of past earnings, revenue and cash flow.

What The Trend Of ROCE Can Tell Us

In terms of China Wan Tong Yuan (Holdings)'s historical ROCE movements, the trend isn't fantastic. To be more specific, ROCE has fallen from 19% over the last five years. And considering revenue has dropped while employing more capital, we'd be cautious. If this were to continue, you might be looking at a company that is trying to reinvest for growth but is actually losing market share since sales haven't increased.

On a related note, China Wan Tong Yuan (Holdings) has decreased its current liabilities to 7.1% of total assets. Since the ratio used to be 61%, that's a significant reduction and it no doubt explains the drop in ROCE. What's more, this can reduce some aspects of risk to the business because now the company's suppliers or short-term creditors are funding less of its operations. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.

In Conclusion...

From the above analysis, we find it rather worrisome that returns on capital and sales for China Wan Tong Yuan (Holdings) have fallen, meanwhile the business is employing more capital than it was five years ago. Yet despite these concerning fundamentals, the stock has performed strongly with a 88% return over the last three years, so investors appear very optimistic. Regardless, we don't feel too comfortable with the fundamentals so we'd be steering clear of this stock for now.

One more thing, we've spotted 2 warning signs facing China Wan Tong Yuan (Holdings) that you might find interesting.

If you want to search for solid companies with great earnings, check out this free list of companies with good balance sheets and impressive returns on equity.

When trading China Wan Tong Yuan (Holdings) or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:6966

China Wan Tong Yuan (Holdings)

An investment holding company, engages in the sale of burial plots and columbarium units in the People’s Republic of China.

Flawless balance sheet with low risk.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor