Advertisement

- Hong Kong

- /

- Hospitality

- /

- SEHK:341

Café de Coral Holdings (HKG:341) Takes On Some Risk With Its Use Of Debt

Howard Marks put it nicely when he said that, rather than worrying about share price volatility, 'The possibility of permanent loss is the risk I worry about... and every practical investor I know worries about.' So it seems the smart money knows that debt - which is usually involved in bankruptcies - is a very important factor, when you assess how risky a company is. We note that Café de Coral Holdings Limited (HKG:341) does have debt on its balance sheet. But the real question is whether this debt is making the company risky.

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. When we examine debt levels, we first consider both cash and debt levels, together.

See our latest analysis for Café de Coral Holdings

What Is Café de Coral Holdings's Debt?

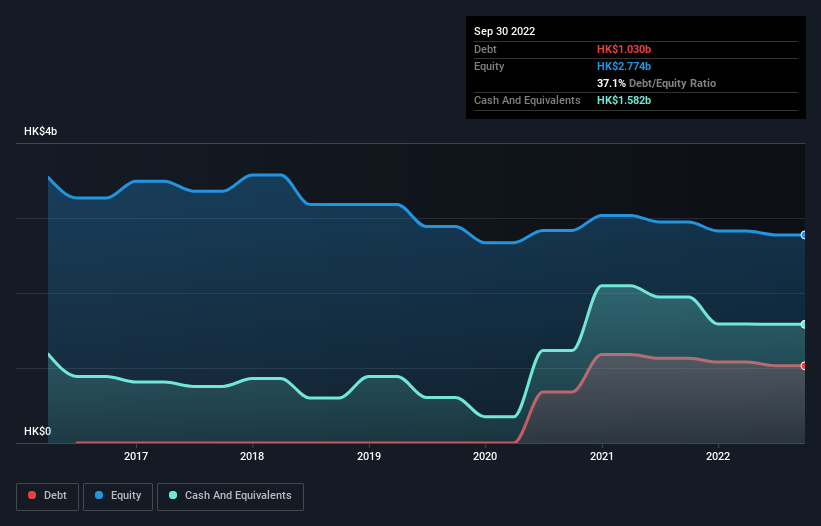

The image below, which you can click on for greater detail, shows that Café de Coral Holdings had debt of HK$1.03b at the end of September 2022, a reduction from HK$1.13b over a year. But on the other hand it also has HK$1.58b in cash, leading to a HK$552.3m net cash position.

How Strong Is Café de Coral Holdings' Balance Sheet?

According to the last reported balance sheet, Café de Coral Holdings had liabilities of HK$2.46b due within 12 months, and liabilities of HK$1.86b due beyond 12 months. On the other hand, it had cash of HK$1.58b and HK$124.9m worth of receivables due within a year. So its liabilities outweigh the sum of its cash and (near-term) receivables by HK$2.61b.

While this might seem like a lot, it is not so bad since Café de Coral Holdings has a market capitalization of HK$6.59b, and so it could probably strengthen its balance sheet by raising capital if it needed to. But we definitely want to keep our eyes open to indications that its debt is bringing too much risk. While it does have liabilities worth noting, Café de Coral Holdings also has more cash than debt, so we're pretty confident it can manage its debt safely.

Shareholders should be aware that Café de Coral Holdings's EBIT was down 57% last year. If that earnings trend continues then paying off its debt will be about as easy as herding cats on to a roller coaster. The balance sheet is clearly the area to focus on when you are analysing debt. But ultimately the future profitability of the business will decide if Café de Coral Holdings can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

Finally, a company can only pay off debt with cold hard cash, not accounting profits. While Café de Coral Holdings has net cash on its balance sheet, it's still worth taking a look at its ability to convert earnings before interest and tax (EBIT) to free cash flow, to help us understand how quickly it is building (or eroding) that cash balance. Over the last two years, Café de Coral Holdings actually produced more free cash flow than EBIT. That sort of strong cash conversion gets us as excited as the crowd when the beat drops at a Daft Punk concert.

Summing Up

While Café de Coral Holdings does have more liabilities than liquid assets, it also has net cash of HK$552.3m. And it impressed us with free cash flow of HK$775m, being 901% of its EBIT. So although we see some areas for improvement, we're not too worried about Café de Coral Holdings's balance sheet. When analysing debt levels, the balance sheet is the obvious place to start. But ultimately, every company can contain risks that exist outside of the balance sheet. Be aware that Café de Coral Holdings is showing 2 warning signs in our investment analysis , you should know about...

At the end of the day, it's often better to focus on companies that are free from net debt. You can access our special list of such companies (all with a track record of profit growth). It's free.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:341

Café de Coral Holdings

An investment holding company, engages in the operation of quick service restaurants and casual dining chains in Hong Kong and Mainland China.

Adequate balance sheet second-rate dividend payer.

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor