Advertisement

- Hong Kong

- /

- Consumer Services

- /

- SEHK:2138

Further weakness as EC Healthcare (HKG:2138) drops 14% this week, taking five-year losses to 85%

We're definitely into long term investing, but some companies are simply bad investments over any time frame. It hits us in the gut when we see fellow investors suffer a loss. For example, we sympathize with anyone who was caught holding EC Healthcare (HKG:2138) during the five years that saw its share price drop a whopping 86%. And we doubt long term believers are the only worried holders, since the stock price has declined 21% over the last twelve months. More recently, the share price has dropped a further 19% in a month. While a drop like that is definitely a body blow, money isn't as important as health and happiness.

Since EC Healthcare has shed HK$119m from its value in the past 7 days, let's see if the longer term decline has been driven by the business' economics.

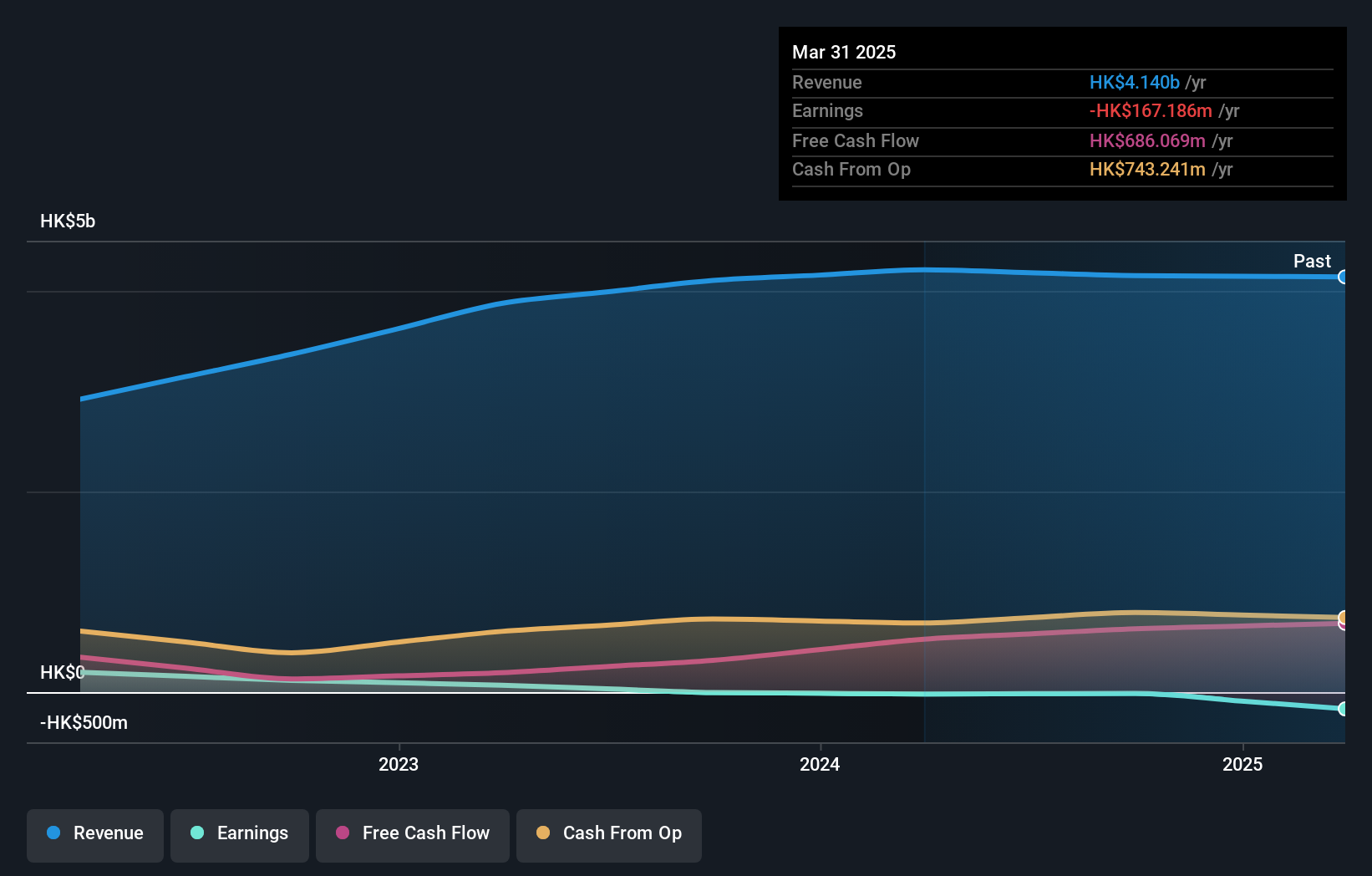

EC Healthcare wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. As you can imagine, fast revenue growth, when maintained, often leads to fast profit growth.

In the last half decade, EC Healthcare saw its revenue increase by 18% per year. That's well above most other pre-profit companies. So on the face of it we're really surprised to see the share price has averaged a fall of 13% each year, in the same time period. It could be that the stock was over-hyped before. While there might be an opportunity here, you'd want to take a close look at the balance sheet strength.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

This free interactive report on EC Healthcare's balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

While the broader market gained around 38% in the last year, EC Healthcare shareholders lost 20% (even including dividends). Even the share prices of good stocks drop sometimes, but we want to see improvements in the fundamental metrics of a business, before getting too interested. However, the loss over the last year isn't as bad as the 13% per annum loss investors have suffered over the last half decade. We would want clear information suggesting the company will grow, before taking the view that the share price will stabilize. It's always interesting to track share price performance over the longer term. But to understand EC Healthcare better, we need to consider many other factors. For example, we've discovered 3 warning signs for EC Healthcare (1 makes us a bit uncomfortable!) that you should be aware of before investing here.

But note: EC Healthcare may not be the best stock to buy. So take a peek at this free list of interesting companies with past earnings growth (and further growth forecast).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on Hong Kong exchanges.

Valuation is complex, but we're here to simplify it.

Discover if EC Healthcare might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2138

EC Healthcare

Provides medical and healthcare services in Hong Kong, Macau, Mainland China, and Taiwan.

Good value with mediocre balance sheet.

Market Insights

Advertisement

Community Narratives

Kodiak AI - a potential 100 bagger opportunity?

Fair Value US$14.00|44.7% undervalued

DA

Community Contributor

A Fair Price for a Great Business Facing Real Threats

Fair Value US$383.06|13.0% undervalued

IM

Community Contributor

AXON And Shopify Integration Will Unlock Global Mobile Advertising

Fair Value US$613.59|2.3% undervalued

AN

Based on Analyst Price Targets