- Hong Kong

- /

- Consumer Services

- /

- SEHK:2138

EC Healthcare's (HKG:2138) Dividend Is Being Reduced To HK$0.005

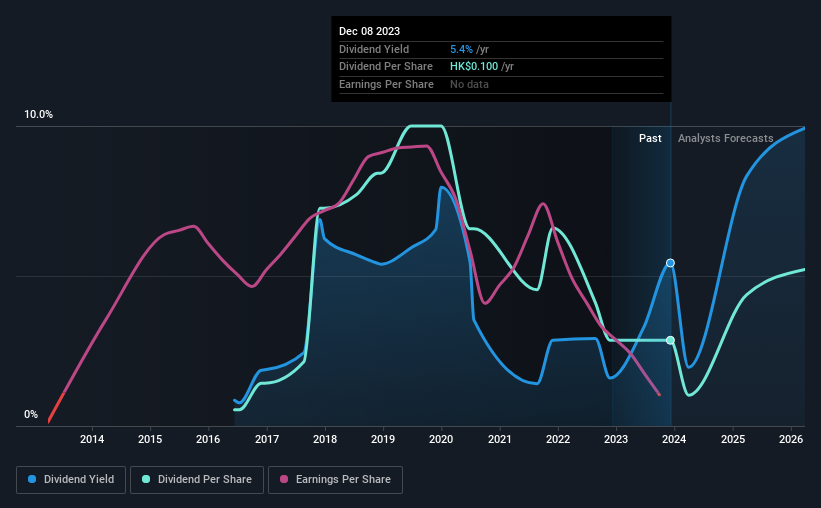

EC Healthcare (HKG:2138) is reducing its dividend to HK$0.005 on the 19th of Januarywhich is 91% less than last year's comparable payment of HK$0.058. However, the dividend yield of 5.4% still remains in a typical range for the industry.

While the dividend yield is important for income investors, it is also important to consider any large share price moves, as this will generally outweigh any gains from distributions. EC Healthcare's stock price has reduced by 49% in the last 3 months, which is not ideal for investors and can explain a sharp increase in the dividend yield.

Check out our latest analysis for EC Healthcare

EC Healthcare Is Paying Out More Than It Is Earning

We aren't too impressed by dividend yields unless they can be sustained over time. While EC Healthcare is not profitable, it is paying out less than 75% of its free cash flow, which means that there is plenty left over for reinvestment into the business. This gives us some comfort about the level of the dividend payments.

EPS is forecast to rise very quickly over the next 12 months. Assuming the dividend continues along recent trends, we could see the payout ratio reach 1,290%, which is on the unsustainable side.

EC Healthcare's Dividend Has Lacked Consistency

Looking back, EC Healthcare's dividend hasn't been particularly consistent. This suggests that the dividend might not be the most reliable. The annual payment during the last 7 years was HK$0.0191 in 2016, and the most recent fiscal year payment was HK$0.10. This means that it has been growing its distributions at 27% per annum over that time. EC Healthcare has grown distributions at a rapid rate despite cutting the dividend at least once in the past. Companies that cut once often cut again, so we would be cautious about buying this stock solely for the dividend income.

The Dividend Has Limited Growth Potential

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. Earnings per share has been sinking by 34% over the last five years. Dividend payments are likely to come under some pressure unless EPS can pull out of the nosedive it is in. On the bright side, earnings are predicted to gain some ground over the next year, but until this turns into a pattern we wouldn't be feeling too comfortable.

EC Healthcare's Dividend Doesn't Look Sustainable

Overall, the dividend looks like it may have been a bit high, which explains why it has now been cut. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We would be a touch cautious of relying on this stock primarily for the dividend income.

Market movements attest to how highly valued a consistent dividend policy is compared to one which is more unpredictable. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. For instance, we've picked out 1 warning sign for EC Healthcare that investors should take into consideration. If you are a dividend investor, you might also want to look at our curated list of high yield dividend stocks.

Valuation is complex, but we're here to simplify it.

Discover if EC Healthcare might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2138

EC Healthcare

An investment holding company, engages in the provision of medical and healthcare services in Hong Kong, Macau, and the People’s Republic of China.

Undervalued with reasonable growth potential.

Market Insights

Community Narratives