- Hong Kong

- /

- Consumer Services

- /

- SEHK:2138

EC Healthcare (HKG:2138) Has Announced That It Will Be Increasing Its Dividend To HK$0.10

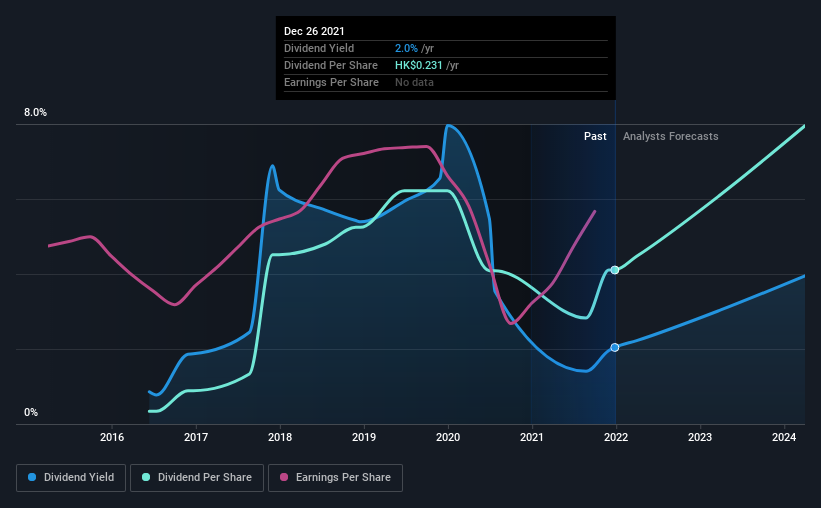

EC Healthcare's (HKG:2138) dividend will be increasing to HK$0.10 on 21st of January. Despite this raise, the dividend yield of 2.0% is only a modest boost to shareholder returns.

See our latest analysis for EC Healthcare

EC Healthcare's Dividend Is Well Covered By Earnings

While yield is important, another factor to consider about a company's dividend is whether the current payout levels are feasible. Prior to this announcement, EC Healthcare's dividend made up quite a large proportion of earnings but only 57% of free cash flows. In general, cash flows are more important than earnings, so we are comfortable that the dividend will be sustainable going forward, especially with so much cash left over for reinvestment.

Over the next year, EPS is forecast to expand by 42.6%. If the dividend continues growing along recent trends, we estimate the payout ratio could reach 78%, which is on the higher side, but certainly still feasible.

EC Healthcare's Dividend Has Lacked Consistency

Even in its relatively short history, the company has reduced the dividend at least once. Due to this, we are a little bit cautious about the dividend consistency over a full economic cycle. Since 2015, the dividend has gone from HK$0.019 to HK$0.23. This implies that the company grew its distributions at a yearly rate of about 52% over that duration. Dividends have grown rapidly over this time, but with cuts in the past we are not certain that this stock will be a reliable source of income in the future.

Dividend Growth Could Be Constrained

Given that the dividend has been cut in the past, we need to check if earnings are growing and if that might lead to stronger dividends in the future. We are encouraged to see that EC Healthcare has grown earnings per share at 11% per year over the past five years. Past earnings growth has been decent, but unless this is one of those rare businesses that can grow without additional capital investment or marketing spend, we'd generally expect the higher payout ratio to limit its future growth prospects.

The company has also been raising capital by issuing stock equal to 13% of shares outstanding in the last 12 months. Regularly doing this can be detrimental - it's hard to grow dividends per share when new shares are regularly being created.

In Summary

Overall, this is probably not a great income stock, even though the dividend is being raised at the moment. The company is generating plenty of cash, which could maintain the dividend for a while, but the track record hasn't been great. We would be a touch cautious of relying on this stock primarily for the dividend income.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. Still, investors need to consider a host of other factors, apart from dividend payments, when analysing a company. As an example, we've identified 2 warning signs for EC Healthcare that you should be aware of before investing. Looking for more high-yielding dividend ideas? Try our curated list of strong dividend payers.

Valuation is complex, but we're here to simplify it.

Discover if EC Healthcare might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2138

EC Healthcare

An investment holding company, engages in the provision of medical and healthcare services in Hong Kong, Macau, and the People’s Republic of China.

Undervalued with reasonable growth potential.

Market Insights

Community Narratives