Advertisement

- Hong Kong

- /

- Consumer Services

- /

- SEHK:1773

Is Tianli International Holdings (HKG:1773) Using Too Much Debt?

Legendary fund manager Li Lu (who Charlie Munger backed) once said, 'The biggest investment risk is not the volatility of prices, but whether you will suffer a permanent loss of capital.' When we think about how risky a company is, we always like to look at its use of debt, since debt overload can lead to ruin. We can see that Tianli International Holdings Limited (HKG:1773) does use debt in its business. But should shareholders be worried about its use of debt?

Why Does Debt Bring Risk?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. If things get really bad, the lenders can take control of the business. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Of course, plenty of companies use debt to fund growth, without any negative consequences. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

See our latest analysis for Tianli International Holdings

How Much Debt Does Tianli International Holdings Carry?

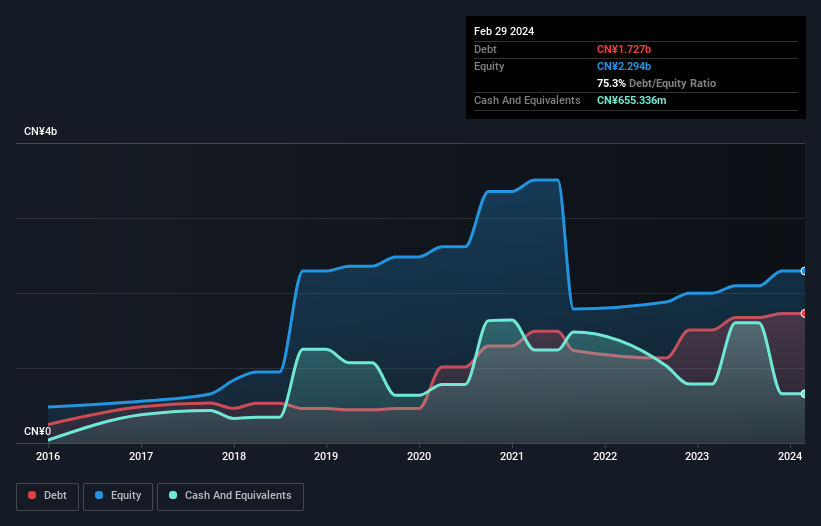

As you can see below, at the end of February 2024, Tianli International Holdings had CN¥1.73b of debt, up from CN¥1.51b a year ago. Click the image for more detail. However, it does have CN¥655.3m in cash offsetting this, leading to net debt of about CN¥1.07b.

How Strong Is Tianli International Holdings' Balance Sheet?

We can see from the most recent balance sheet that Tianli International Holdings had liabilities of CN¥3.82b falling due within a year, and liabilities of CN¥2.80b due beyond that. Offsetting this, it had CN¥655.3m in cash and CN¥718.4m in receivables that were due within 12 months. So its liabilities total CN¥5.24b more than the combination of its cash and short-term receivables.

Tianli International Holdings has a market capitalization of CN¥10.2b, so it could very likely raise cash to ameliorate its balance sheet, if the need arose. But it's clear that we should definitely closely examine whether it can manage its debt without dilution.

We measure a company's debt load relative to its earnings power by looking at its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and by calculating how easily its earnings before interest and tax (EBIT) cover its interest expense (interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Tianli International Holdings has a low net debt to EBITDA ratio of only 1.4. And its EBIT covers its interest expense a whopping 10.0 times over. So you could argue it is no more threatened by its debt than an elephant is by a mouse. On top of that, Tianli International Holdings grew its EBIT by 83% over the last twelve months, and that growth will make it easier to handle its debt. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Tianli International Holdings can strengthen its balance sheet over time. So if you're focused on the future you can check out this free report showing analyst profit forecasts.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So it's worth checking how much of that EBIT is backed by free cash flow. Looking at the most recent three years, Tianli International Holdings recorded free cash flow of 29% of its EBIT, which is weaker than we'd expect. That's not great, when it comes to paying down debt.

Our View

On our analysis Tianli International Holdings's EBIT growth rate should signal that it won't have too much trouble with its debt. However, our other observations weren't so heartening. For instance it seems like it has to struggle a bit to convert EBIT to free cash flow. Considering this range of data points, we think Tianli International Holdings is in a good position to manage its debt levels. But a word of caution: we think debt levels are high enough to justify ongoing monitoring. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. For example - Tianli International Holdings has 1 warning sign we think you should be aware of.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

Valuation is complex, but we're here to simplify it.

Discover if Tianli International Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1773

Tianli International Holdings

An investment holding company, provides education management and diversified services in China.

Exceptional growth potential with outstanding track record.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.6% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.4% undervalued

TO

Community Contributor