Advertisement

- Hong Kong

- /

- Consumer Services

- /

- SEHK:1769

Discovering Hong Kong's Undiscovered Gems In August 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate volatility and mixed economic signals, the Hong Kong market has shown resilience, with the Hang Seng Index gaining 0.85% amidst broader concerns about deflationary pressures in China. This backdrop presents a unique opportunity to explore lesser-known stocks that could offer potential growth despite uncertain times. In such an environment, identifying promising stocks involves looking for companies with strong fundamentals and solid growth prospects that can withstand market fluctuations.

Top 10 Undiscovered Gems With Strong Fundamentals In Hong Kong

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| E-Commodities Holdings | 23.22% | 6.87% | 31.81% | ★★★★★★ |

| PW Medtech Group | NA | 17.93% | -2.70% | ★★★★★★ |

| China Leon Inspection Holding | 17.06% | 24.06% | 27.08% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| JiaXing Gas Group | 17.72% | 26.04% | 22.07% | ★★★★★☆ |

| Xin Point Holdings | 2.03% | 9.80% | 15.04% | ★★★★★☆ |

| Hung Hing Printing Group | 3.97% | -2.51% | 33.57% | ★★★★★☆ |

| Changjiu Holdings | 14.09% | 12.87% | -4.74% | ★★★★★☆ |

| Time Interconnect Technology | 212.50% | 27.21% | 15.01% | ★★★★☆☆ |

| Pizu Group Holdings | 48.34% | -4.53% | -19.78% | ★★★★☆☆ |

Let's explore several standout options from the results in the screener.

YiChang HEC ChangJiang Pharmaceutical (SEHK:1558)

Simply Wall St Value Rating: ★★★★★☆

Overview: YiChang HEC ChangJiang Pharmaceutical Co., Ltd. (SEHK:1558) focuses on the research, development, manufacturing, and sale of pharmaceutical products with a market cap of approximately HK$8.61 billion.

Operations: YiChang HEC ChangJiang Pharmaceutical generates revenue primarily from the sales of pharmaceutical products, amounting to CN¥6.29 billion. The net profit margin for the company is 16.50%.

YiChang HEC ChangJiang Pharmaceutical, a notable player in the Hong Kong market, has demonstrated robust financial health with a net debt to equity ratio of 9.2%, which is considered satisfactory. The company's interest payments are well covered by EBIT at 16.9x coverage, indicating strong profitability. Its price-to-earnings ratio stands at an attractive 4x compared to the market's 9x. Despite earnings declining annually by 15.7% over five years, last year's earnings surged by an impressive 2501.2%.

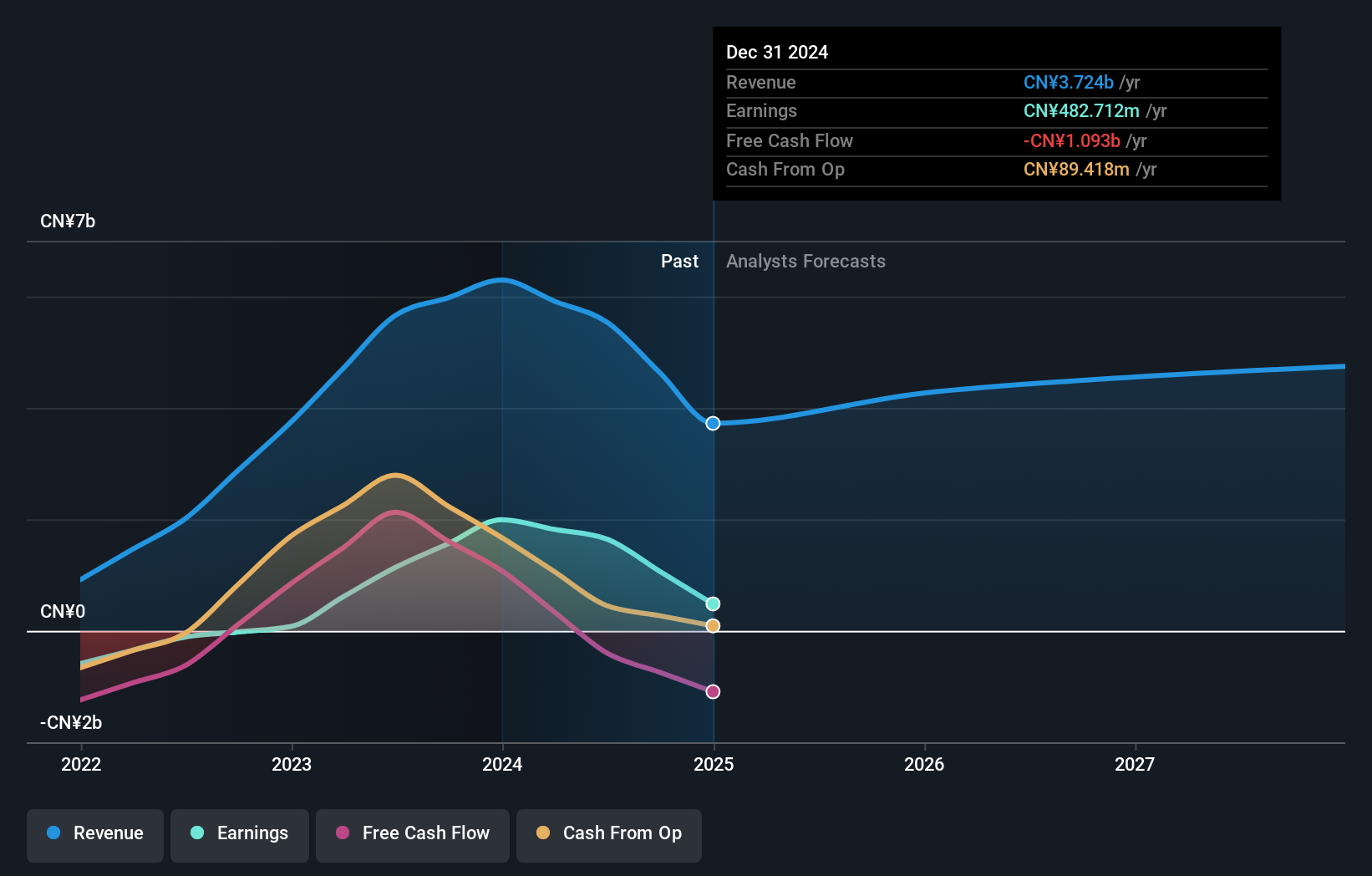

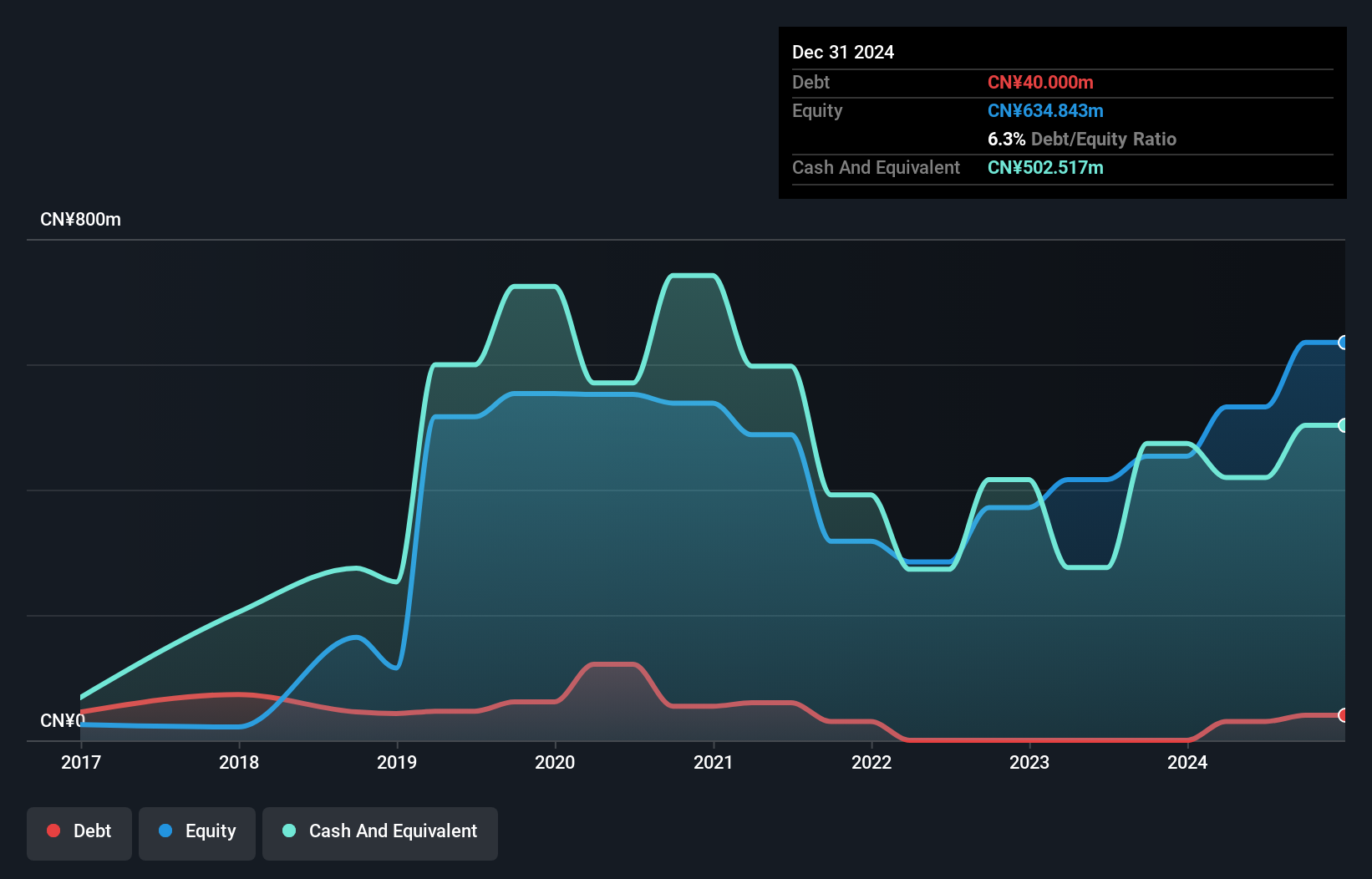

Scholar Education Group (SEHK:1769)

Simply Wall St Value Rating: ★★★★★★

Overview: Scholar Education Group, an investment holding company, provides K-12 after-school education services in the People’s Republic of China and has a market cap of HK$2.73 billion.

Operations: Scholar Education Group generates revenue primarily from its private education services, amounting to CN¥570.61 million.

Scholar Education Group, trading at 73.2% below its estimated fair value, has seen earnings decline by 8.5% annually over the past five years but grew by 58% last year. The company is debt-free, a notable improvement from a debt-to-equity ratio of 37.1% five years ago. Recent guidance indicates an expected revenue of RMB 380 million for H1 2024, up over 51%, and a net profit of RMB 80 million, reflecting an increase exceeding 86%.

Inspur Digital Enterprise Technology (SEHK:596)

Simply Wall St Value Rating: ★★★★★☆

Overview: Inspur Digital Enterprise Technology Limited, an investment holding company with a market cap of HK$3.93 billion, provides software development, other software services, and cloud services in the People’s Republic of China.

Operations: Inspur Digital Enterprise Technology generates revenue from three primary segments: Cloud Services (CN¥2.00 billion), Management Software (CN¥2.47 billion), and Internet of Things (IoT) Solutions (CN¥3.83 billion). The company's net profit margin is %.

Inspur Digital Enterprise Technology, a small cap in Hong Kong, is trading at 39.4% below its estimated fair value and shows good relative value compared to peers. The company has more cash than total debt and maintains high-quality earnings. Despite a 69.9% earnings growth last year not surpassing the software industry average, it remains profitable with interest payments well-covered by profits. Earnings are forecasted to grow at 38.02% annually, indicating strong future potential.

Seize The Opportunity

- Reveal the 175 hidden gems among our SEHK Undiscovered Gems With Strong Fundamentals screener with a single click here.

- Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

- Discover a world of investment opportunities with Simply Wall St's free app and access unparalleled stock analysis across all markets.

Want To Explore Some Alternatives?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1769

Scholar Education Group

An investment holding company, engages in the provision of private education services in the People’s Republic of China and Hong Kong.

Outstanding track record with flawless balance sheet.

Market Insights

Advertisement

Community Narratives

MicroStrategy: Volatile Gamble or Golden Opportunity?

Fair Value US$663.00|36.2% undervalued

BL

Community Contributor

Emerging Markets and Debt Reduction Will Propel Bath & Body Works Forward

Fair Value US$40.73|22.0% undervalued

ZW

Community Contributor

An amazing opportunity to potentially get a 100 bagger

Fair Value US$10.00|46.4% overvalued

DA

Community Contributor