Advertisement

- Hong Kong

- /

- Entertainment

- /

- SEHK:1119

SEHK Growth Companies With High Insider Ownership And Up To 104% Earnings Growth

Simply Wall St

Reviewed by Simply Wall St

As global markets navigate through varying economic signals, the Hong Kong market has shown resilience with the Hang Seng Index climbing 2.64% recently, buoyed by positive holiday spending and robust trade data. In this context, growth companies with high insider ownership in Hong Kong could be particularly compelling for investors looking for firms with potentially aligned interests between management and shareholders.

Top 10 Growth Companies With High Insider Ownership In Hong Kong

| Name | Insider Ownership | Earnings Growth |

| iDreamSky Technology Holdings (SEHK:1119) | 20.1% | 104.1% |

| New Horizon Health (SEHK:6606) | 16.6% | 61% |

| Fenbi (SEHK:2469) | 32.1% | 43% |

| Meitu (SEHK:1357) | 38% | 34.3% |

| Adicon Holdings (SEHK:9860) | 22.3% | 29.6% |

| DPC Dash (SEHK:1405) | 38.2% | 91.5% |

| Beijing Airdoc Technology (SEHK:2251) | 26.4% | 83.9% |

| Zhejiang Leapmotor Technology (SEHK:9863) | 14.2% | 74% |

| Biocytogen Pharmaceuticals (Beijing) (SEHK:2315) | 15.7% | 100.1% |

| Ocumension Therapeutics (SEHK:1477) | 17.7% | 93.7% |

Here's a peek at a few of the choices from the screener.

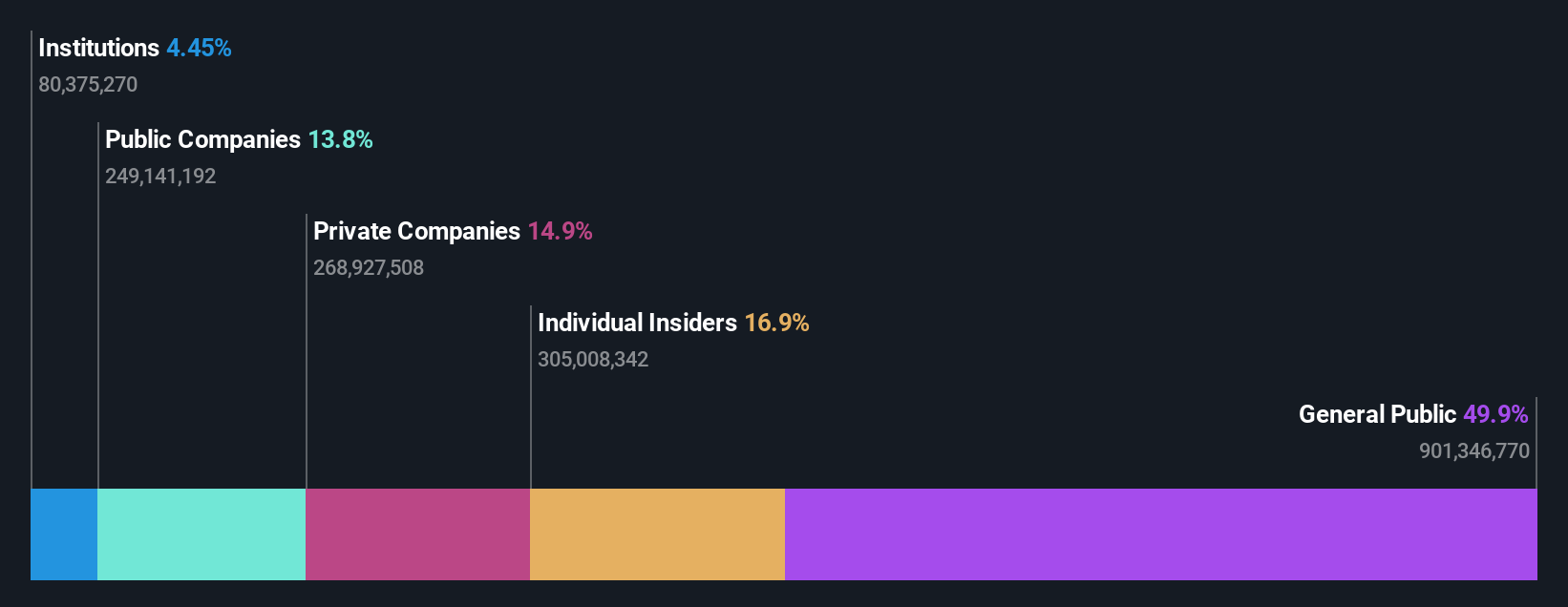

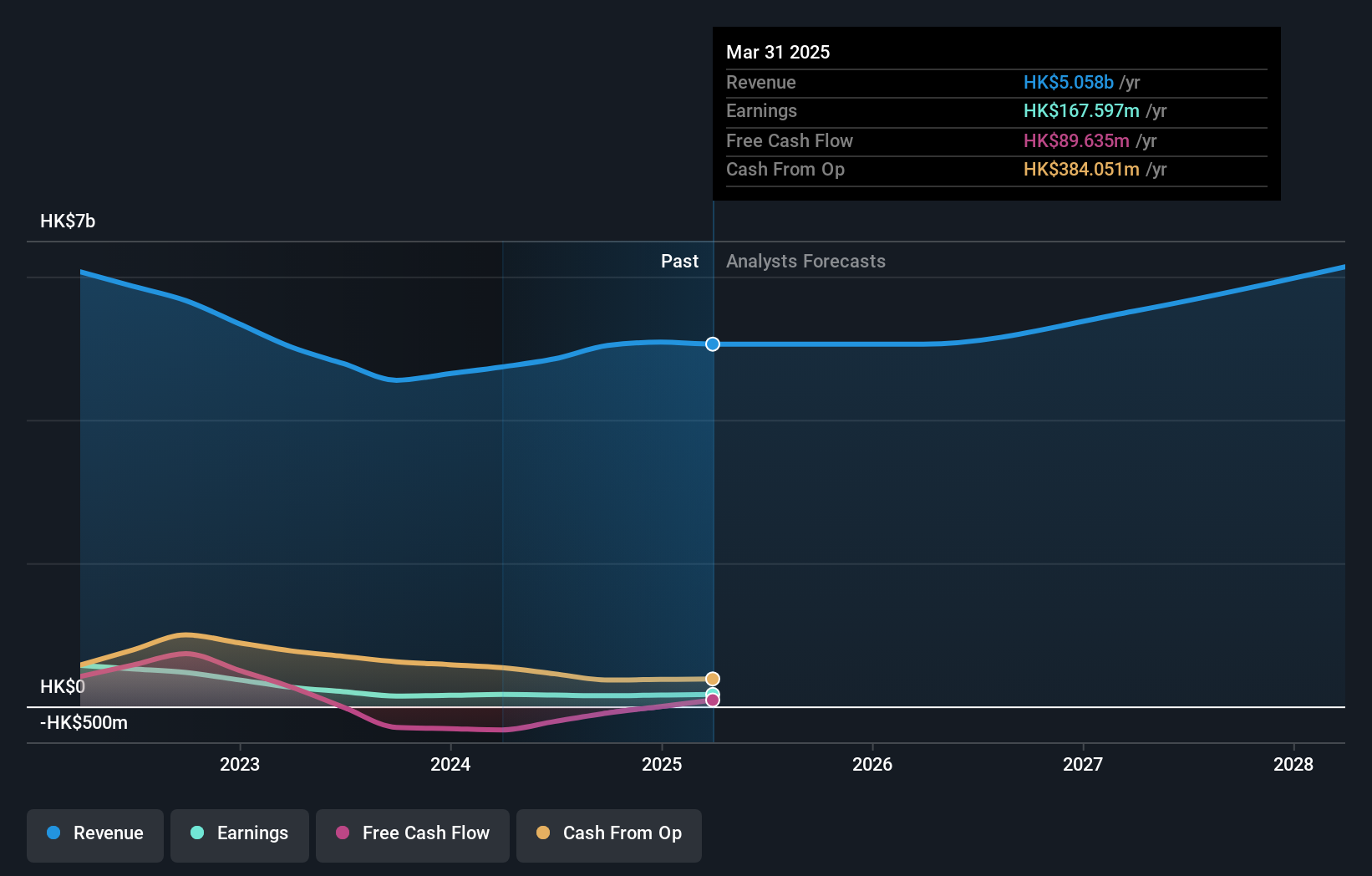

iDreamSky Technology Holdings (SEHK:1119)

Simply Wall St Growth Rating: ★★★★★★

Overview: iDreamSky Technology Holdings Limited, an investment holding company, operates a digital entertainment platform that publishes games through mobile apps and websites in the People’s Republic of China, with a market cap of approximately HK$4.77 billion.

Operations: The company generates revenue primarily from game and information services, including SaaS and related services, totaling CN¥1.92 billion.

Insider Ownership: 20.1%

Earnings Growth Forecast: 104.1% p.a.

iDreamSky Technology Holdings has shown resilience with a significant reduction in net loss from CNY 2.49 billion to CNY 556.35 million year-over-year and a decrease in basic loss per share. Despite recent revenue declines, the company is poised for recovery, underscored by strategic alliances like the one with Saudi Cloud Computing Company to enhance its gaming sector presence. Insider buying trends and expectations of becoming profitable within three years highlight confidence in its growth trajectory, although shareholder dilution remains a concern.

- Delve into the full analysis future growth report here for a deeper understanding of iDreamSky Technology Holdings.

- The analysis detailed in our iDreamSky Technology Holdings valuation report hints at an deflated share price compared to its estimated value.

Pacific Textiles Holdings (SEHK:1382)

Simply Wall St Growth Rating: ★★★★☆☆

Overview: Pacific Textiles Holdings Limited is a company engaged in the manufacturing and trading of textile products, with a market capitalization of approximately HK$2.27 billion.

Operations: The company generates revenue primarily through the manufacturing and trading of textile products, totaling approximately HK$4.55 billion.

Insider Ownership: 11.2%

Earnings Growth Forecast: 27.3% p.a.

Pacific Textiles Holdings is positioned for robust earnings growth, with forecasts suggesting a 27.34% increase per year, outpacing the broader Hong Kong market. However, its revenue growth at 9% annually lags behind the high-growth benchmark of 20%. Challenges include a decline in profit margins from 8.4% to 3.2%, and significant one-off items affecting financial stability. Additionally, its dividends are not adequately covered by earnings or cash flows, raising sustainability concerns despite trading at a substantial discount to estimated fair value.

- Click here and access our complete growth analysis report to understand the dynamics of Pacific Textiles Holdings.

- Our comprehensive valuation report raises the possibility that Pacific Textiles Holdings is priced higher than what may be justified by its financials.

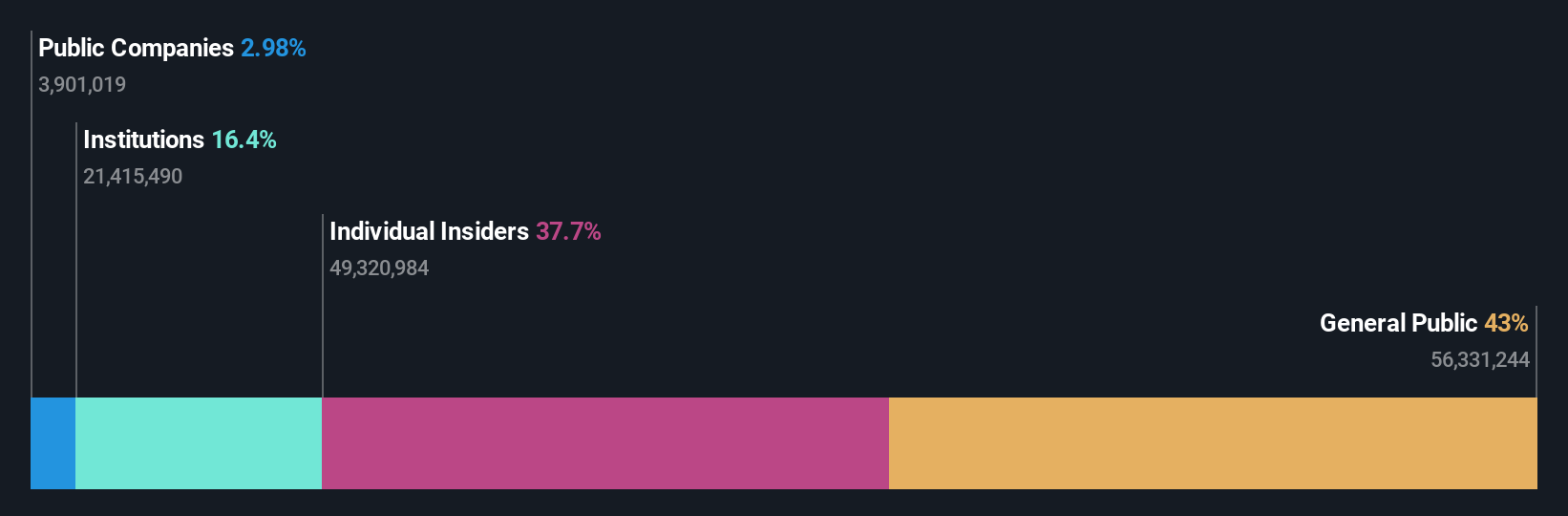

DPC Dash (SEHK:1405)

Simply Wall St Growth Rating: ★★★★★☆

Overview: DPC Dash Ltd operates a chain of fast-food restaurants across the People’s Republic of China, with a market capitalization of approximately HK$7.68 billion.

Operations: The company generates its revenues primarily from its fast-food restaurant operations, totaling CN¥3.05 billion.

Insider Ownership: 38.2%

Earnings Growth Forecast: 91.5% p.a.

DPC Dash Ltd, a growth-oriented firm with high insider ownership, is trading at 64.1% below its fair value and analysts expect a 24.9% price increase. The company has shown a strong revenue uptrend, growing at 24.5% annually and is set to become profitable within three years. Despite recent losses decreasing significantly from CNY 222.63 million to CNY 26.6 million year-over-year, the forecasted return on equity remains modest at 14%. Insiders have been net buyers of shares recently, underscoring their confidence in the company's prospects.

- Click here to discover the nuances of DPC Dash with our detailed analytical future growth report.

- Our expertly prepared valuation report DPC Dash implies its share price may be lower than expected.

Taking Advantage

- Click here to access our complete index of 52 Fast Growing SEHK Companies With High Insider Ownership.

- Have you diversified into these companies? Leverage the power of Simply Wall St's portfolio to keep a close eye on market movements affecting your investments.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Curious About Other Options?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Valuation is complex, but we're here to simplify it.

Discover if iDreamSky Technology Holdings might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:1119

iDreamSky Technology Holdings

An investment holding company, operates a digital entertainment platform that publishes games through mobile apps and websites in the People’s Republic of China.

Slightly overvalued with imperfect balance sheet.

Similar Companies

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.7% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|93.3% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|18.7% undervalued

GM

Community Contributor