- Hong Kong

- /

- Consumer Services

- /

- SEHK:1317

Is It Time To Consider Buying China Maple Leaf Educational Systems Limited (HKG:1317)?

China Maple Leaf Educational Systems Limited (HKG:1317), is not the largest company out there, but it saw a double-digit share price rise of over 10% in the past couple of months on the SEHK. With many analysts covering the stock, we may expect any price-sensitive announcements have already been factored into the stock’s share price. But what if there is still an opportunity to buy? Today I will analyse the most recent data on China Maple Leaf Educational Systems’s outlook and valuation to see if the opportunity still exists.

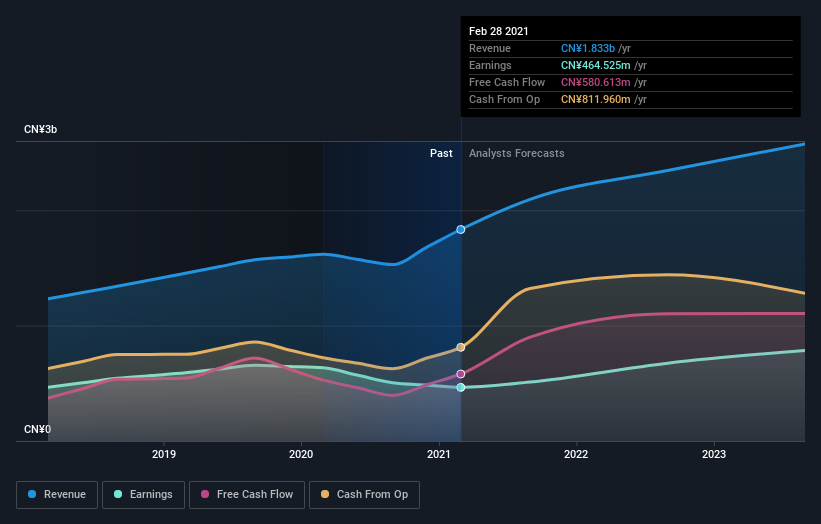

See our latest analysis for China Maple Leaf Educational Systems

Is China Maple Leaf Educational Systems still cheap?

Good news, investors! China Maple Leaf Educational Systems is still a bargain right now according to my price multiple model, which compares the company's price-to-earnings ratio to the industry average. I’ve used the price-to-earnings ratio in this instance because there’s not enough visibility to forecast its cash flows. The stock’s ratio of 6.18x is currently well-below the industry average of 15.17x, meaning that it is trading at a cheaper price relative to its peers. China Maple Leaf Educational Systems’s share price also seems relatively stable compared to the rest of the market, as indicated by its low beta. If you believe the share price should eventually reach its industry peers, a low beta could suggest it is unlikely to rapidly do so anytime soon, and once it’s there, it may be hard to fall back down into an attractive buying range.

Can we expect growth from China Maple Leaf Educational Systems?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Buying a great company with a robust outlook at a cheap price is always a good investment, so let’s also take a look at the company's future expectations. With profit expected to grow by 57% over the next couple of years, the future seems bright for China Maple Leaf Educational Systems. It looks like higher cash flow is on the cards for the stock, which should feed into a higher share valuation.

What this means for you:

Are you a shareholder? Since 1317 is currently trading below the industry PE ratio, it may be a great time to accumulate more of your holdings in the stock. With an optimistic profit outlook on the horizon, it seems like this growth has not yet been fully factored into the share price. However, there are also other factors such as capital structure to consider, which could explain the current price multiple.

Are you a potential investor? If you’ve been keeping an eye on 1317 for a while, now might be the time to enter the stock. Its prosperous future profit outlook isn’t fully reflected in the current share price yet, which means it’s not too late to buy 1317. But before you make any investment decisions, consider other factors such as the track record of its management team, in order to make a well-informed assessment.

With this in mind, we wouldn't consider investing in a stock unless we had a thorough understanding of the risks. In terms of investment risks, we've identified 3 warning signs with China Maple Leaf Educational Systems, and understanding them should be part of your investment process.

If you are no longer interested in China Maple Leaf Educational Systems, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

The New Payments ETF Is Live on NASDAQ:

Money is moving to real-time rails, and a newly listed ETF now gives investors direct exposure. Fast settlement. Institutional custody. Simple access.

Explore how this launch could reshape portfolios

Sponsored ContentNew: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:1317

China Maple Leaf Educational Systems

Operates bilingual private and preschools in the People’s Republic of China, Malaysia, Singapore, and internationally.

Good value with proven track record.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Meta’s Bold Bet on AI Pays Off

ADP Stock: Solid Fundamentals, But AI Investments Test Its Margin Resilience

Visa Stock: The Toll Booth at the Center of Global Commerce

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

The AI Infrastructure Giant Grows Into Its Valuation

Trending Discussion