Advertisement

- Hong Kong

- /

- Hospitality

- /

- SEHK:1128

We Think Wynn Macau's (HKG:1128) Profit Is Only A Baseline For What They Can Achieve

Even though Wynn Macau, Limited's (HKG:1128) recent earnings release was robust, the market didn't seem to notice. Our analysis suggests that investors might be missing some promising details.

View our latest analysis for Wynn Macau

Zooming In On Wynn Macau's Earnings

One key financial ratio used to measure how well a company converts its profit to free cash flow (FCF) is the accrual ratio. In plain english, this ratio subtracts FCF from net profit, and divides that number by the company's average operating assets over that period. This ratio tells us how much of a company's profit is not backed by free cashflow.

As a result, a negative accrual ratio is a positive for the company, and a positive accrual ratio is a negative. While having an accrual ratio above zero is of little concern, we do think it's worth noting when a company has a relatively high accrual ratio. That's because some academic studies have suggested that high accruals ratios tend to lead to lower profit or less profit growth.

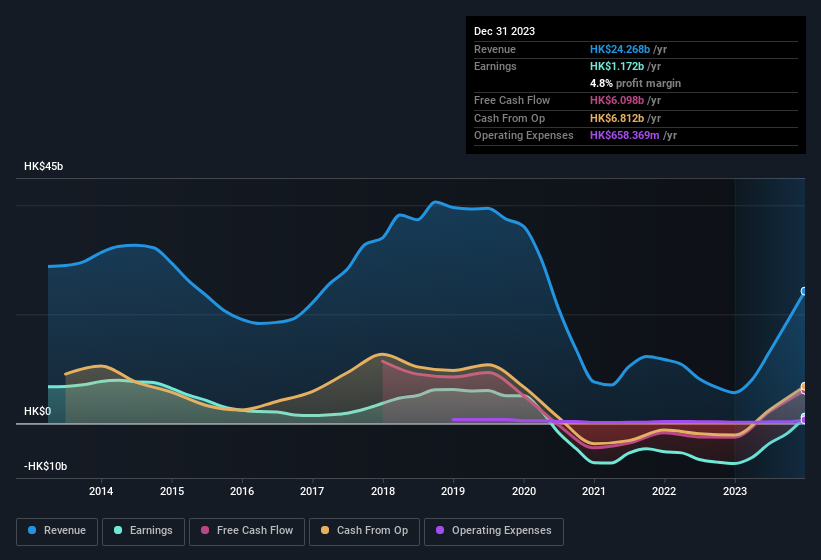

For the year to December 2023, Wynn Macau had an accrual ratio of -0.22. Therefore, its statutory earnings were very significantly less than its free cashflow. Indeed, in the last twelve months it reported free cash flow of HK$6.1b, well over the HK$1.17b it reported in profit. Given that Wynn Macau had negative free cash flow in the prior corresponding period, the trailing twelve month resul of HK$6.1b would seem to be a step in the right direction.

That might leave you wondering what analysts are forecasting in terms of future profitability. Luckily, you can click here to see an interactive graph depicting future profitability, based on their estimates.

Our Take On Wynn Macau's Profit Performance

Happily for shareholders, Wynn Macau produced plenty of free cash flow to back up its statutory profit numbers. Based on this observation, we consider it possible that Wynn Macau's statutory profit actually understates its earnings potential! And one can definitely find a positive in the fact that it made a profit this year, despite losing money last year. At the end of the day, it's essential to consider more than just the factors above, if you want to understand the company properly. In light of this, if you'd like to do more analysis on the company, it's vital to be informed of the risks involved. Case in point: We've spotted 2 warning signs for Wynn Macau you should be aware of.

Today we've zoomed in on a single data point to better understand the nature of Wynn Macau's profit. But there is always more to discover if you are capable of focussing your mind on minutiae. Some people consider a high return on equity to be a good sign of a quality business. So you may wish to see this free collection of companies boasting high return on equity, or this list of stocks that insiders are buying.

Valuation is complex, but we're here to simplify it.

Discover if Wynn Macau might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:1128

Wynn Macau

Owns, develops, and operates integrated destination casino resorts in the People’s Republic of China.

Low risk and slightly overvalued.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|11.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|23.3% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|13.8% undervalued

EA

Community Contributor