Advertisement

- Hong Kong

- /

- Food and Staples Retail

- /

- SEHK:759

Returns Are Gaining Momentum At CEC International Holdings (HKG:759)

What are the early trends we should look for to identify a stock that could multiply in value over the long term? In a perfect world, we'd like to see a company investing more capital into its business and ideally the returns earned from that capital are also increasing. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. With that in mind, we've noticed some promising trends at CEC International Holdings (HKG:759) so let's look a bit deeper.

Understanding Return On Capital Employed (ROCE)

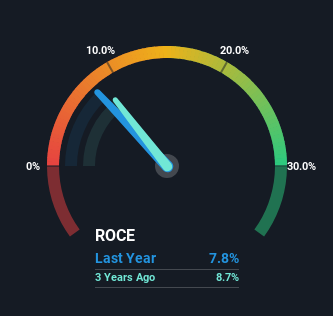

For those who don't know, ROCE is a measure of a company's yearly pre-tax profit (its return), relative to the capital employed in the business. The formula for this calculation on CEC International Holdings is:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.078 = HK$50m ÷ (HK$917m - HK$271m) (Based on the trailing twelve months to April 2023).

So, CEC International Holdings has an ROCE of 7.8%. In absolute terms, that's a low return but it's around the Consumer Retailing industry average of 9.4%.

Check out our latest analysis for CEC International Holdings

While the past is not representative of the future, it can be helpful to know how a company has performed historically, which is why we have this chart above. If you want to delve into the historical earnings, revenue and cash flow of CEC International Holdings, check out these free graphs here.

What Can We Tell From CEC International Holdings' ROCE Trend?

The fact that CEC International Holdings is now generating some pre-tax profits from its prior investments is very encouraging. About five years ago the company was generating losses but things have turned around because it's now earning 7.8% on its capital. In addition to that, CEC International Holdings is employing 40% more capital than previously which is expected of a company that's trying to break into profitability. This can indicate that there's plenty of opportunities to invest capital internally and at ever higher rates, both common traits of a multi-bagger.

On a related note, the company's ratio of current liabilities to total assets has decreased to 30%, which basically reduces it's funding from the likes of short-term creditors or suppliers. This tells us that CEC International Holdings has grown its returns without a reliance on increasing their current liabilities, which we're very happy with.

What We Can Learn From CEC International Holdings' ROCE

To the delight of most shareholders, CEC International Holdings has now broken into profitability. And since the stock has fallen 45% over the last five years, there might be an opportunity here. So researching this company further and determining whether or not these trends will continue seems justified.

One more thing, we've spotted 3 warning signs facing CEC International Holdings that you might find interesting.

While CEC International Holdings may not currently earn the highest returns, we've compiled a list of companies that currently earn more than 25% return on equity. Check out this free list here.

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:759

CEC International Holdings

An investment holding company, retails food and beverage, and household and personal care products in the People’s Republic of China and internationally.

Excellent balance sheet and good value.

Market Insights

Advertisement

Community Narratives

Finding The True Value Of A Logistics Powerhouse

Fair Value US$95.21|8.4% undervalued

NV

Community Contributor

Paradigm Biopharmaceuticals Will Lead Osteoarthritis Treatment with Zilosul's FDA Success

Fair Value AU$5.50|91.9% undervalued

AM

Community Contributor

Barrick Mining (ABX:CA): A Gold Hedge against a U.S. Shutdown

Fair Value CA$60.00|24.2% undervalued

GM

Community Contributor