Sun Art Retail Group (SEHK:6808) has seen its shares fluctuate in recent weeks, drawing attention from investors curious about the company’s current value. Recent performance trends raise some interesting points as market participants reassess their outlook.

Sun Art Retail Group’s share price has drifted lower in recent months, reflecting some hesitation from investors despite pockets of positive news around earnings. Over the past year, the total shareholder return has been modestly positive, suggesting momentum is steady but not surging.

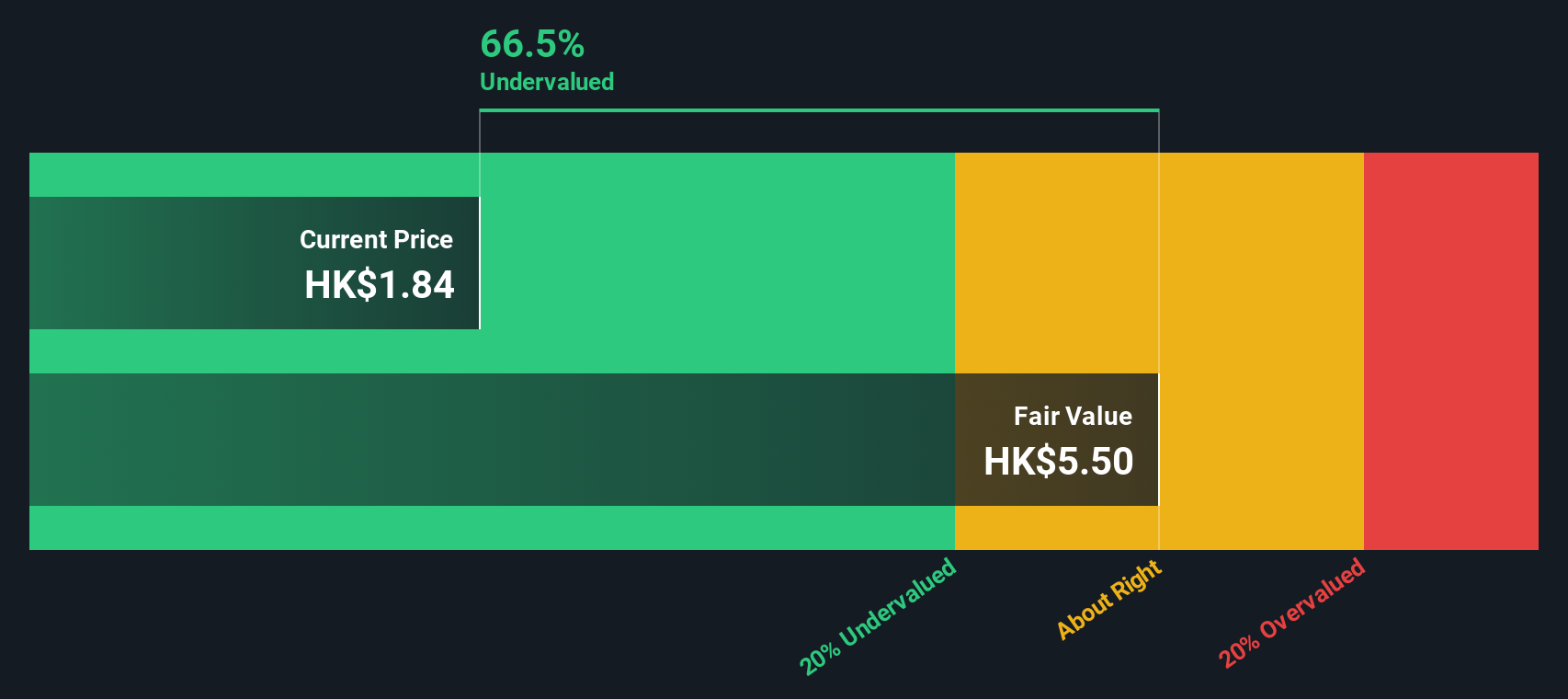

With shares trading at a notable discount to analyst targets but showing steady, if unspectacular, growth, the key question is whether Sun Art Retail Group is undervalued at these levels or if the market has already accounted for its future prospects.

Advertisement

Price-to-Earnings of 40.1: Is it justified?

Sun Art Retail Group is currently trading at a price-to-earnings ratio of 40.1, which is significantly above both the industry and peer group averages. This suggests that the market is assigning a much higher valuation to its earnings compared to similar retailers.

The price-to-earnings ratio (PE) reflects what investors are willing to pay now for each dollar of future earnings. For a consumer retailing company like Sun Art Retail Group, a high PE can indicate expectations of rapid future profit growth, but it may also reflect market optimism that is not fully supported by fundamentals.

Currently, Sun Art Retail Group’s PE is more than double the industry average of 16.1 and is higher than the peer average of 25.7. This sharp premium signals strong confidence in the company’s comeback and future profitability. However, when compared to an estimated fair PE ratio of 24.5 based on regression models, the current valuation appears stretched and may not be sustainable without exceptional earnings growth to match.

While the market’s high price-to-earnings ratio signals some optimism, our DCF model shows the shares trading around 66% below their estimated fair value. This alternate perspective suggests a potentially significant undervaluation. Could the current market be overlooking Sun Art Retail Group’s true worth?

If you see things differently or want to dive deeper into the numbers, it only takes a few minutes to build your own perspective. So why not Do it your way?

A great starting point for your Sun Art Retail Group research is our analysis highlighting 4 key rewards and 2 important warning signs that could impact your investment decision.

Ready for More Smart Investment Ideas?

Smart investors know there’s always a next move. Don’t let opportunity pass you by and amplify your portfolio’s potential with targeted strategies you won’t want to overlook.

Seize the possibilities of transformative technology and get ahead with these 24 AI penny stocks, built for rapid growth in artificial intelligence and automation.

This article by Simply Wall St is general in nature. We provide commentary based on historical data

and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your

financial situation. We aim to bring you long-term focused analysis driven by fundamental data.

Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency • Be alerted to new Warning Signs or Risks via email or mobile • Track the Fair Value of your stocks