- Hong Kong

- /

- Food and Staples Retail

- /

- SEHK:6618

JD Health International (HKG:6618) Is Reinvesting At Lower Rates Of Return

To find a multi-bagger stock, what are the underlying trends we should look for in a business? Firstly, we'll want to see a proven return on capital employed (ROCE) that is increasing, and secondly, an expanding base of capital employed. Basically this means that a company has profitable initiatives that it can continue to reinvest in, which is a trait of a compounding machine. Although, when we looked at JD Health International (HKG:6618), it didn't seem to tick all of these boxes.

What Is Return On Capital Employed (ROCE)?

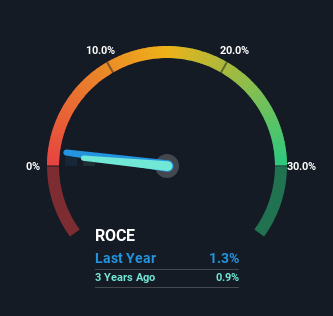

For those that aren't sure what ROCE is, it measures the amount of pre-tax profits a company can generate from the capital employed in its business. Analysts use this formula to calculate it for JD Health International:

Return on Capital Employed = Earnings Before Interest and Tax (EBIT) ÷ (Total Assets - Current Liabilities)

0.013 = CN¥631m ÷ (CN¥64b - CN¥15b) (Based on the trailing twelve months to December 2023).

Therefore, JD Health International has an ROCE of 1.3%. In absolute terms, that's a low return and it also under-performs the Consumer Retailing industry average of 8.6%.

Check out our latest analysis for JD Health International

In the above chart we have measured JD Health International's prior ROCE against its prior performance, but the future is arguably more important. If you're interested, you can view the analysts predictions in our free analyst report for JD Health International .

How Are Returns Trending?

When we looked at the ROCE trend at JD Health International, we didn't gain much confidence. Around five years ago the returns on capital were 40%, but since then they've fallen to 1.3%. Although, given both revenue and the amount of assets employed in the business have increased, it could suggest the company is investing in growth, and the extra capital has led to a short-term reduction in ROCE. If these investments prove successful, this can bode very well for long term stock performance.

On a related note, JD Health International has decreased its current liabilities to 23% of total assets. That could partly explain why the ROCE has dropped. Effectively this means their suppliers or short-term creditors are funding less of the business, which reduces some elements of risk. Since the business is basically funding more of its operations with it's own money, you could argue this has made the business less efficient at generating ROCE.

In Conclusion...

Even though returns on capital have fallen in the short term, we find it promising that revenue and capital employed have both increased for JD Health International. But since the stock has dived 77% in the last three years, there could be other drivers that are influencing the business' outlook. Regardless, reinvestment can pay off in the long run, so we think astute investors may want to look further into this stock.

If you're still interested in JD Health International it's worth checking out our FREE intrinsic value approximation for 6618 to see if it's trading at an attractive price in other respects.

While JD Health International isn't earning the highest return, check out this free list of companies that are earning high returns on equity with solid balance sheets.

If you're looking to trade JD Health International, open an account with the lowest-cost platform trusted by professionals, Interactive Brokers.

With clients in over 200 countries and territories, and access to 160 markets, IBKR lets you trade stocks, options, futures, forex, bonds and funds from a single integrated account.

Enjoy no hidden fees, no account minimums, and FX conversion rates as low as 0.03%, far better than what most brokers offer.

Sponsored ContentNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:6618

JD Health International

An investment holding company, engages in the operation of an online healthcare platform in the People’s Republic of China and internationally.

Flawless balance sheet with solid track record.

Market Insights

Community Narratives