Advertisement

- Hong Kong

- /

- Real Estate

- /

- SEHK:119

Undiscovered Gems In Hong Kong To Watch This October 2024

Simply Wall St

Reviewed by Simply Wall St

As global markets react to China's robust stimulus measures, the Hang Seng Index in Hong Kong has seen a significant uptick, reflecting renewed investor optimism. This positive sentiment presents an opportune moment to explore some lesser-known stocks that could benefit from these economic tailwinds. In this dynamic environment, identifying stocks with strong fundamentals and growth potential becomes crucial for investors looking to capitalize on market movements.

Top 10 Undiscovered Gems With Strong Fundamentals In Hong Kong

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Lion Rock Group | 16.91% | 14.33% | 10.15% | ★★★★★★ |

| Changjiu Holdings | NA | 11.84% | 2.46% | ★★★★★★ |

| Sundart Holdings | 0.92% | -2.32% | -3.94% | ★★★★★★ |

| China Leon Inspection Holding | 8.55% | 21.36% | 22.77% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| S.A.S. Dragon Holdings | 60.96% | 4.62% | 10.02% | ★★★★★☆ |

| Lvji Technology Holdings | 3.06% | 4.56% | -1.87% | ★★★★★☆ |

| Billion Industrial Holdings | 3.63% | 18.00% | -11.38% | ★★★★★☆ |

| Time Interconnect Technology | 151.14% | 24.74% | 19.78% | ★★★★☆☆ |

| Chongqing Machinery & Electric | 27.77% | 8.82% | 11.12% | ★★★★☆☆ |

Let's review some notable picks from our screened stocks.

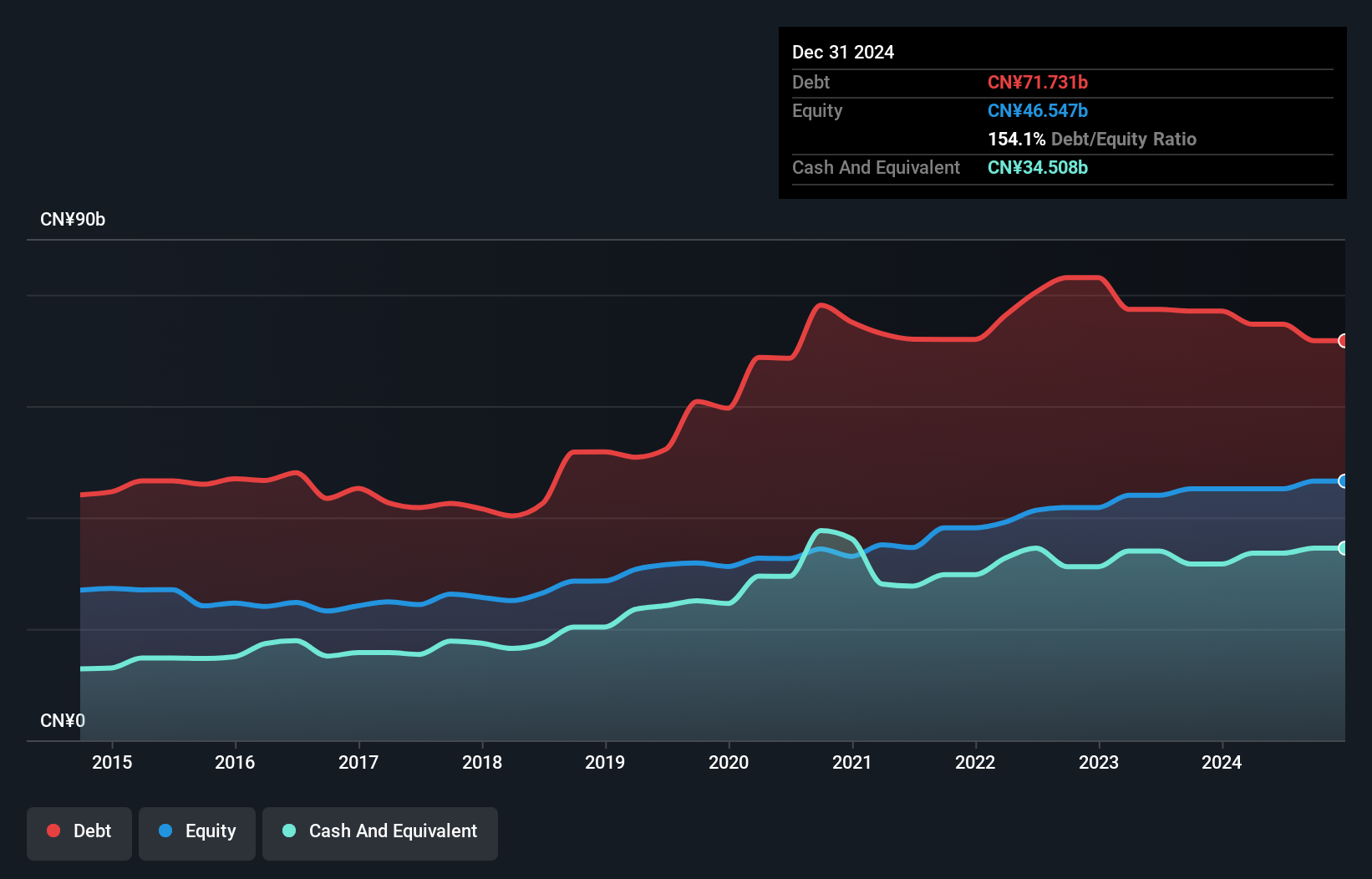

Poly Property Group (SEHK:119)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Poly Property Group Co., Limited is an investment holding company that engages in property investment, development, and management in Hong Kong, the People’s Republic of China, and internationally, with a market cap of HK$6.80 billion.

Operations: Poly Property Group generates revenue primarily from its property development business (CN¥35.59 billion) and property investment and management (CN¥1.87 billion), with additional income from hotel operations (CN¥377.21 million).

Poly Property Group's earnings surged 531% last year, outpacing the real estate sector's -11%. However, its debt-to-equity ratio remains high at 91.1%, and operating cash flow doesn't cover its debt well. Recently, the company reported a net income of CNY 373 million for H1 2024, down from CNY 639 million a year ago. Contracted sales value reached RMB36.8 billion by August 2024 with an average selling price of RMB25,628 per sq.m., reflecting robust market activity despite profit challenges.

- Take a closer look at Poly Property Group's potential here in our health report.

Explore historical data to track Poly Property Group's performance over time in our Past section.

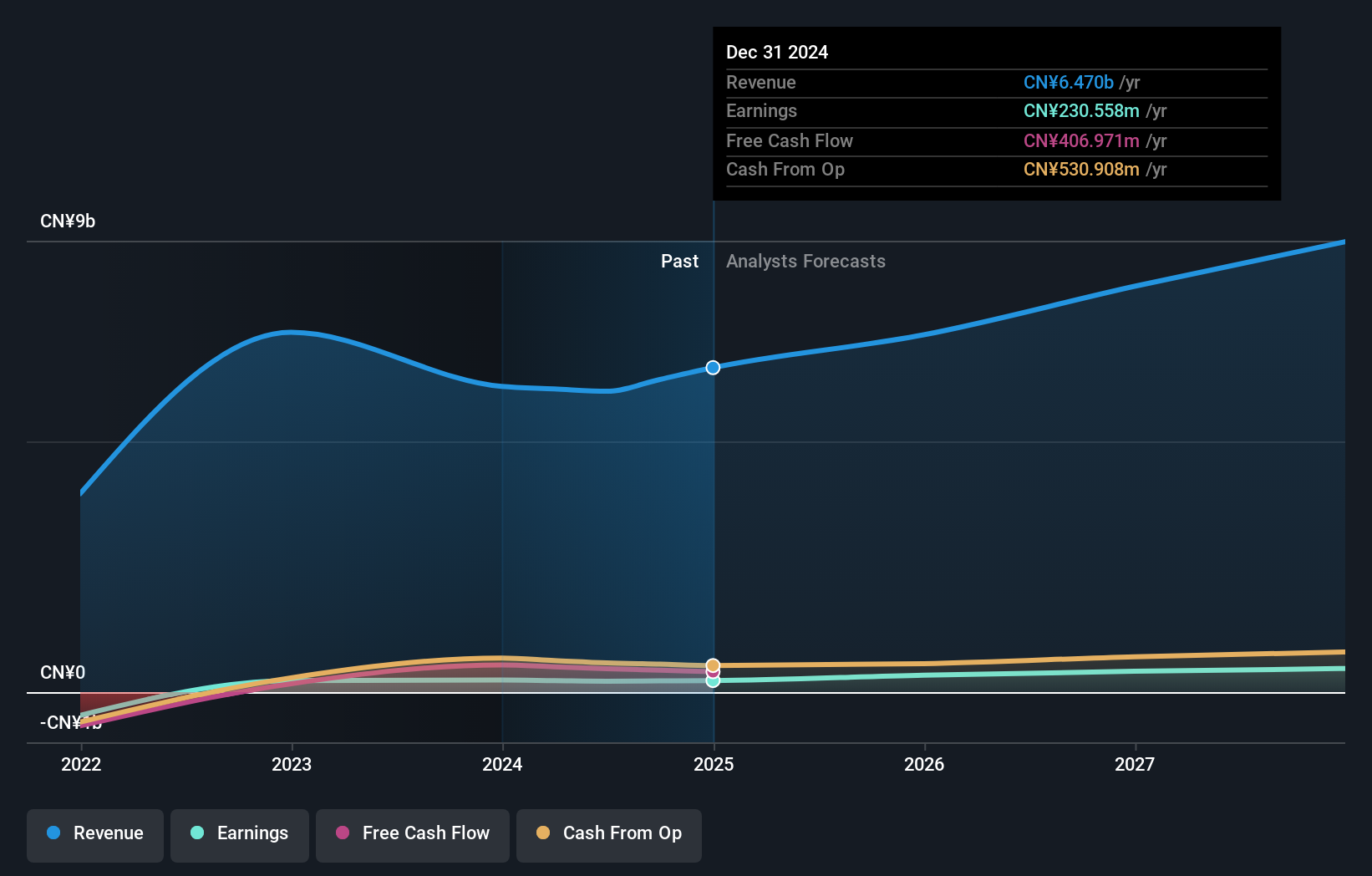

Guoquan Food (Shanghai) (SEHK:2517)

Simply Wall St Value Rating: ★★★★★☆

Overview: Guoquan Food (Shanghai) Co., Ltd. operates as a home meal products company in China with a market cap of HK$10.47 billion.

Operations: Guoquan Food (Shanghai) Co., Ltd. generates revenue primarily from retail grocery stores, amounting to CN¥5.998 billion.

Guoquan Food (Shanghai) saw a mixed first half of 2024, with sales reaching CNY 2.67 billion, down from CNY 2.76 billion the previous year. Net income also dipped to CNY 86 million from CNY 108 million. Basic earnings per share fell to CNY 0.0313 compared to last year's CNY 0.0403, reflecting some challenges in performance. The company held a board meeting on August 28, approving interim results and considering an interim dividend amidst executive changes and market volatility.

- Unlock comprehensive insights into our analysis of Guoquan Food (Shanghai) stock in this health report.

Learn about Guoquan Food (Shanghai)'s historical performance.

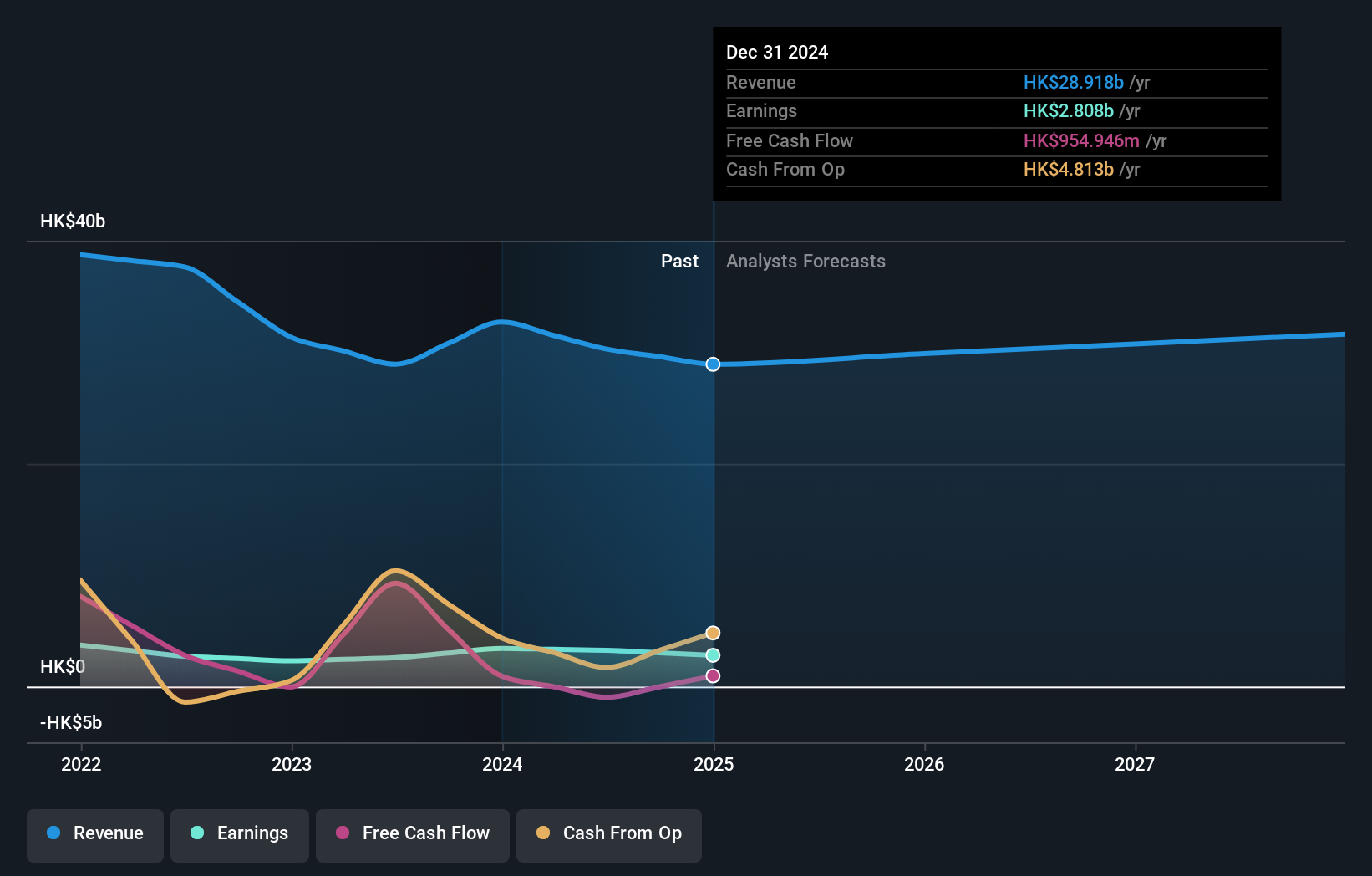

Shanghai Industrial Holdings (SEHK:363)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Shanghai Industrial Holdings Limited is an investment holding company that operates in infrastructure and environmental protection, real estate, consumer products, and comprehensive healthcare across Hong Kong, China, the rest of Asia, and internationally with a market cap of HK$13.18 billion.

Operations: The company's revenue streams are primarily derived from real estate (HK$17.26 billion), infrastructure and environmental protection (HK$9.42 billion), and consumer products (HK$3.59 billion).

Shanghai Industrial Holdings, a small-cap player in the Hong Kong market, has shown robust performance with earnings growth of 25.6% over the past year, outpacing the Industrials industry at 4.1%. The company's net debt to equity ratio stands at 43.3%, indicating high leverage but manageable interest payments covered by EBIT (6.3x). Recent half-year results reported HK$10.37b in sales and HK$1.2b in net income, alongside an interim dividend of HK$0.42 per share for shareholders on record as of September 24, 2024.

Taking Advantage

- Explore the 167 names from our SEHK Undiscovered Gems With Strong Fundamentals screener here.

- Already own these companies? Link your portfolio to Simply Wall St and get alerts on any new warning signs to your stocks.

- Maximize your investment potential with Simply Wall St, the comprehensive app that offers global market insights for free.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:119

Poly Property Group

An investment holding company, engages in the property investment, development, and management business in Hong Kong, the People’s Republic of China, and internationally.

Adequate balance sheet and slightly overvalued.

Market Insights

Advertisement

Community Narratives

For the Emperor: Why Games Workshop Could Be a Star Investment

Fair Value UK£160.00|0.5% overvalued

RO

Community Contributor

Securitas will boost margins with AI and tech-driven services

Fair Value SEK 260.91|44.5% undervalued

UN

Community Contributor

A Leader in EV Charging with Growth Potential

Fair Value €27.00|18.7% undervalued

TI

Community Contributor