- Hong Kong

- /

- Food and Staples Retail

- /

- SEHK:2517

Exploring Poly Property Group And 2 Other Hidden Small Caps with Solid Financials

Reviewed by Simply Wall St

Amid a surge in Chinese stocks driven by robust stimulus measures from Beijing, the Hong Kong market has experienced renewed investor interest, with the Hang Seng Index gaining 13%. This positive sentiment creates an opportune moment to explore small-cap companies with solid financials that may benefit from these macroeconomic developments. In this context, identifying stocks like Poly Property Group and other hidden gems can provide unique opportunities for investors seeking stability and potential growth within the dynamic landscape of Hong Kong's equity market.

Top 10 Undiscovered Gems With Strong Fundamentals In Hong Kong

| Name | Debt To Equity | Revenue Growth | Earnings Growth | Health Rating |

|---|---|---|---|---|

| Lion Rock Group | 16.91% | 14.33% | 10.15% | ★★★★★★ |

| E-Commodities Holdings | 21.33% | 9.04% | 28.46% | ★★★★★★ |

| C&D Property Management Group | 1.32% | 37.15% | 41.55% | ★★★★★★ |

| COSCO SHIPPING International (Hong Kong) | NA | -3.84% | 16.33% | ★★★★★★ |

| Sundart Holdings | 0.92% | -2.32% | -3.94% | ★★★★★★ |

| Tianyun International Holdings | 10.09% | -5.59% | -9.92% | ★★★★★★ |

| S.A.S. Dragon Holdings | 60.96% | 4.62% | 10.02% | ★★★★★☆ |

| Time Interconnect Technology | 151.14% | 24.74% | 19.78% | ★★★★☆☆ |

| Chongqing Machinery & Electric | 27.77% | 8.82% | 11.12% | ★★★★☆☆ |

| Pizu Group Holdings | 48.34% | -4.53% | -19.78% | ★★★★☆☆ |

Let's uncover some gems from our specialized screener.

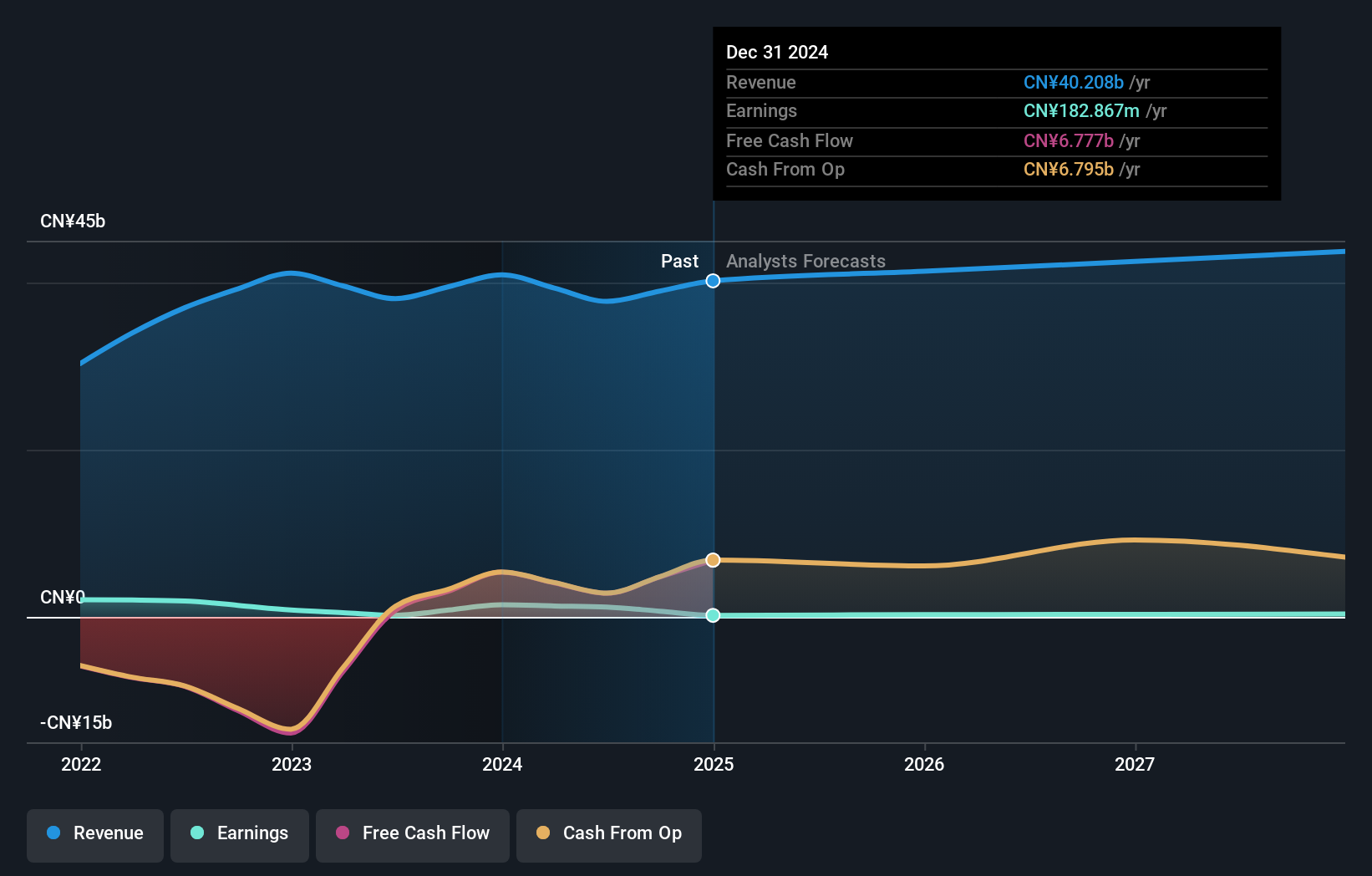

Poly Property Group (SEHK:119)

Simply Wall St Value Rating: ★★★★☆☆

Overview: Poly Property Group Co., Limited is an investment holding company involved in property investment, development, and management across Hong Kong, the People's Republic of China, and internationally, with a market cap of approximately HK$8.06 billion.

Operations: Poly Property Group generates revenue primarily from its property development business, contributing CN¥35.59 billion, and property investment and management, adding CN¥1.87 billion. The hotel operations segment provides an additional CN¥377.21 million in revenue.

Poly Property Group stands out with its high-quality earnings and impressive 531% earnings growth over the past year, significantly outperforming the real estate industry's -11.2%. Despite trading at a substantial discount of 92.7% below estimated fair value, challenges persist with a high net debt to equity ratio of 91.1%, indicating financial leverage concerns. Recent sales figures highlight robust activity, achieving RMB 36.8 billion in contracted sales by August 2024, reflecting strong market engagement despite a downturn impacting gross profit margins.

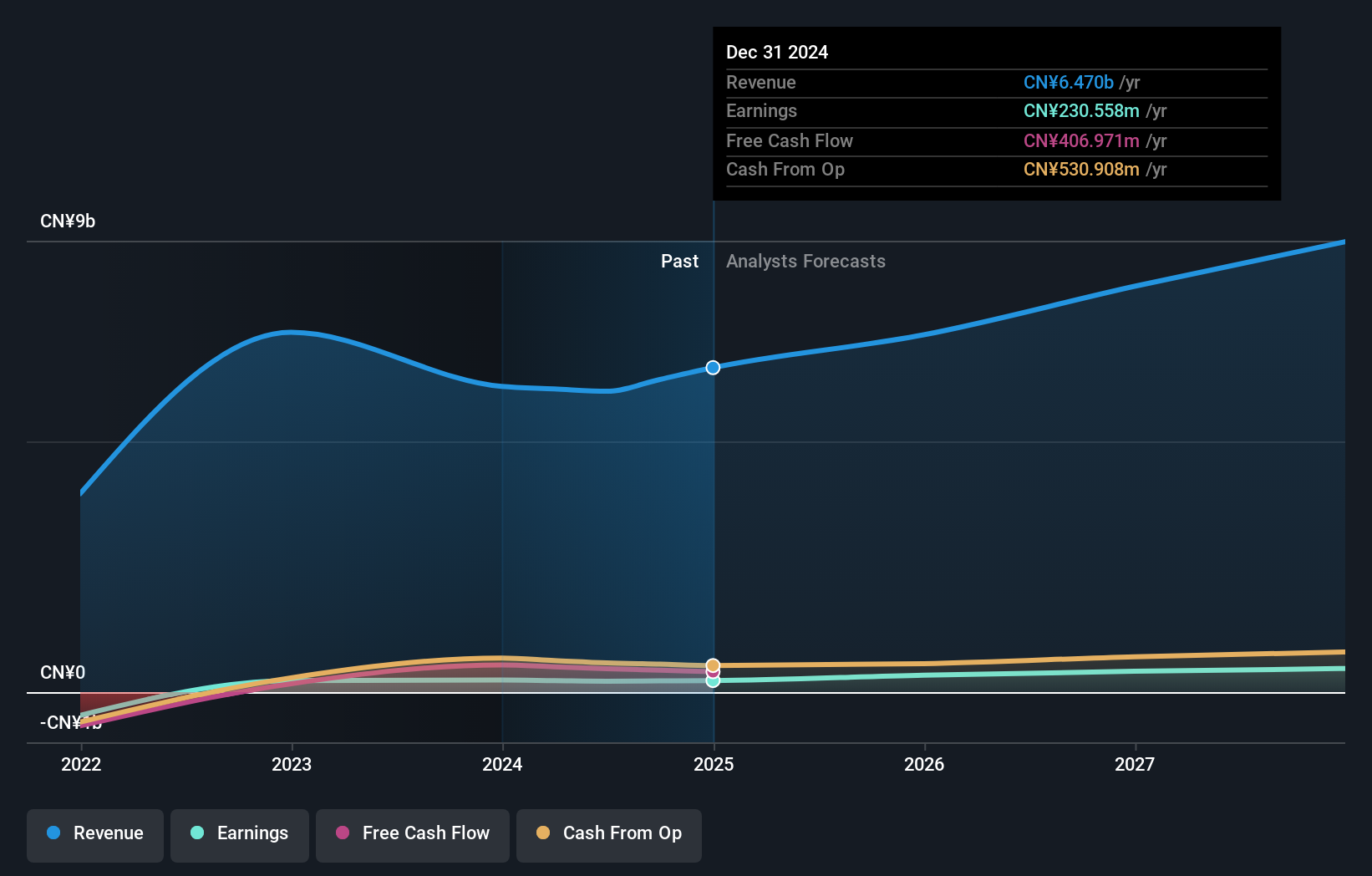

Guoquan Food (Shanghai) (SEHK:2517)

Simply Wall St Value Rating: ★★★★★☆

Overview: Guoquan Food (Shanghai) Co., Ltd. is a Chinese company specializing in home meal products with a market capitalization of approximately HK$9.48 billion.

Operations: Guoquan Food generates revenue primarily from its retail segment, specifically grocery stores, amounting to CN¥5.99 billion.

Guoquan Food, a small player in the market, reported half-year sales of CNY 2.67 billion, down from CNY 2.76 billion the previous year. Net income also saw a dip to CNY 86 million from CNY 108 million. Despite these figures, it trades at a significant discount of 55% below its estimated fair value and maintains high-quality earnings with positive free cash flow of CNY 467.84 million as of June 2024.

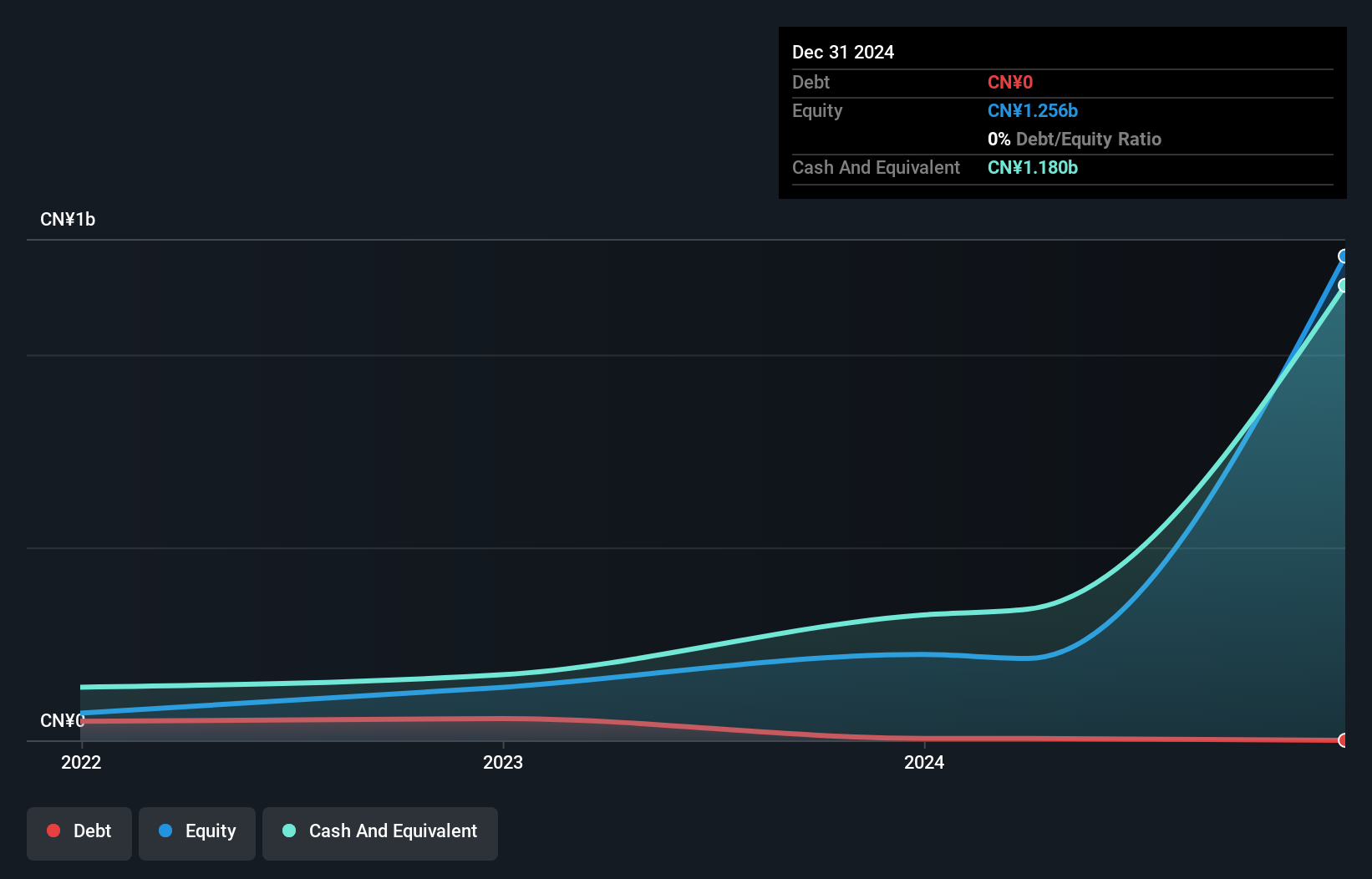

Carote (SEHK:2549)

Simply Wall St Value Rating: ★★★★★☆

Overview: Carote Ltd is an investment holding company that supplies kitchenware products to brand-owners and retailers under the CAROTE brand, with a market cap of HK$4.90 billion.

Operations: Carote Ltd generates revenue primarily through its Branded Business segment, which accounts for CN¥1.58 billion, significantly overshadowing the ODM Business segment at CN¥210.80 million.

Carote recently made waves with its HKD 750.62 million IPO, offering shares at HKD 5.78 each, highlighting its potential in the market. The company shows a promising trajectory with earnings growth of 92% over the past year, outpacing the Consumer Durables industry’s 20%. Trading at a significant discount of 72% below estimated fair value suggests untapped potential. Carote's high-quality earnings and positive free cash flow further bolster confidence in its financial health and future prospects.

- Click here to discover the nuances of Carote with our detailed analytical health report.

Gain insights into Carote's past trends and performance with our Past report.

Seize The Opportunity

- Click through to start exploring the rest of the 169 SEHK Undiscovered Gems With Strong Fundamentals now.

- Are you invested in these stocks already? Keep abreast of every twist and turn by setting up a portfolio with Simply Wall St, where we make it simple for investors like you to stay informed and proactive.

- Elevate your portfolio with Simply Wall St, the ultimate app for investors seeking global market coverage.

Ready For A Different Approach?

- Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

- Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

- Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Mobile Infrastructure for Defense and Disaster

The next wave in robotics isn't humanoid. Its fully autonomous towers delivering 5G, ISR, and radar in under 30 minutes, anywhere.

Get the investor briefing before the next round of contracts

Sponsored On Behalf of CiTechNew: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

About SEHK:2517

Guoquan Food (Shanghai)

Operates as a home meal products company in Mainland China.

Solid track record with excellent balance sheet.

Market Insights

Weekly Picks

Early mover in a fast growing industry. Likely to experience share price volatility as they scale

A case for CA$31.80 (undiluted), aka 8,616% upside from CA$0.37 (an 86 bagger!).

Moderation and Stabilisation: HOLD: Fair Price based on a 4-year Cycle is $12.08

Recently Updated Narratives

Title: Market Sentiment Is Dead Wrong — Here's Why PSEC Deserves a Second Look

An amazing opportunity to potentially get a 100 bagger

Amazon: Why the World’s Biggest Platform Still Runs on Invisible Economics

Popular Narratives

Crazy Undervalued 42 Baggers Silver Play (Active & Running Mine)

MicroVision will explode future revenue by 380.37% with a vision towards success

NVDA: Expanding AI Demand Will Drive Major Data Center Investments Through 2026

Trending Discussion