Advertisement

We Think Pegasus International Holdings (HKG:676) Can Easily Afford To Drive Business Growth

There's no doubt that money can be made by owning shares of unprofitable businesses. For example, although software-as-a-service business Salesforce.com lost money for years while it grew recurring revenue, if you held shares since 2005, you'd have done very well indeed. But while history lauds those rare successes, those that fail are often forgotten; who remembers Pets.com?

So, the natural question for Pegasus International Holdings (HKG:676) shareholders is whether they should be concerned by its rate of cash burn. For the purpose of this article, we'll define cash burn as the amount of cash the company is spending each year to fund its growth (also called its negative free cash flow). Let's start with an examination of the business' cash, relative to its cash burn.

View our latest analysis for Pegasus International Holdings

How Long Is Pegasus International Holdings' Cash Runway?

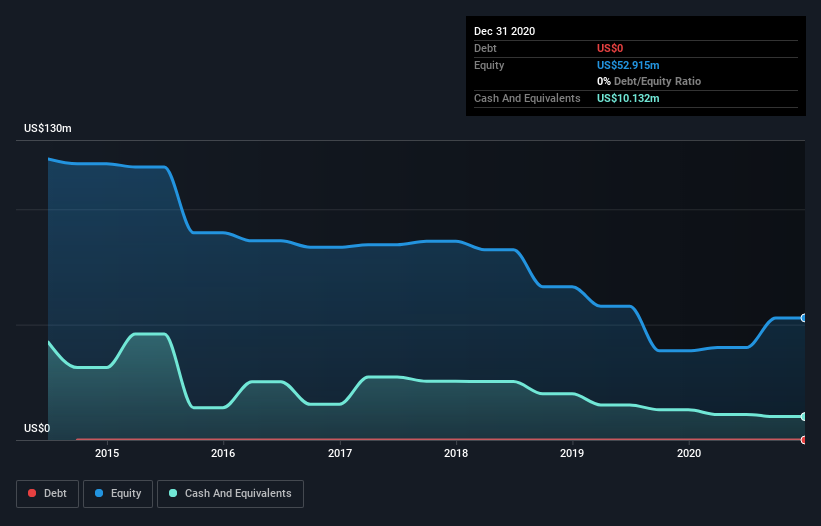

A company's cash runway is the amount of time it would take to burn through its cash reserves at its current cash burn rate. In December 2020, Pegasus International Holdings had US$10m in cash, and was debt-free. Importantly, its cash burn was US$3.5m over the trailing twelve months. So it had a cash runway of about 2.9 years from December 2020. Arguably, that's a prudent and sensible length of runway to have. The image below shows how its cash balance has been changing over the last few years.

How Is Pegasus International Holdings' Cash Burn Changing Over Time?

Whilst it's great to see that Pegasus International Holdings has already begun generating revenue from operations, last year it only produced US$3.4m, so we don't think it is generating significant revenue, at this point. As a result, we think it's a bit early to focus on the revenue growth, so we'll limit ourselves to looking at how the cash burn is changing over time. The 56% reduction in its cash burn over the last twelve months may be good for protecting the balance sheet but it hardly points to imminent growth. Pegasus International Holdings makes us a little nervous due to its lack of substantial operating revenue. So we'd generally prefer stocks from this list of stocks that have analysts forecasting growth.

How Easily Can Pegasus International Holdings Raise Cash?

While we're comforted by the recent reduction evident from our analysis of Pegasus International Holdings' cash burn, it is still worth considering how easily the company could raise more funds, if it wanted to accelerate spending to drive growth. Companies can raise capital through either debt or equity. Many companies end up issuing new shares to fund future growth. We can compare a company's cash burn to its market capitalisation to get a sense for how many new shares a company would have to issue to fund one year's operations.

Pegasus International Holdings' cash burn of US$3.5m is about 5.0% of its US$69m market capitalisation. Given that is a rather small percentage, it would probably be really easy for the company to fund another year's growth by issuing some new shares to investors, or even by taking out a loan.

Is Pegasus International Holdings' Cash Burn A Worry?

It may already be apparent to you that we're relatively comfortable with the way Pegasus International Holdings is burning through its cash. In particular, we think its cash runway stands out as evidence that the company is well on top of its spending. But it's fair to say that its cash burn reduction was also very reassuring. After taking into account the various metrics mentioned in this report, we're pretty comfortable with how the company is spending its cash. On another note, Pegasus International Holdings has 3 warning signs (and 1 which is concerning) we think you should know about.

If you would prefer to check out another company with better fundamentals, then do not miss this free list of interesting companies, that have HIGH return on equity and low debt or this list of stocks which are all forecast to grow.

When trading stocks or any other investment, use the platform considered by many to be the Professional's Gateway to the Worlds Market, Interactive Brokers. You get the lowest-cost* trading on stocks, options, futures, forex, bonds and funds worldwide from a single integrated account. Promoted

New: Manage All Your Stock Portfolios in One Place

We've created the ultimate portfolio companion for stock investors, and it's free.

• Connect an unlimited number of Portfolios and see your total in one currency

• Be alerted to new Warning Signs or Risks via email or mobile

• Track the Fair Value of your stocks

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:676

Pegasus International Holdings

An investment holding company, manufactures, trades, markets, and sells of footwear products in the United States, Morocco, and internationally.

Mediocre balance sheet minimal.

Market Insights

Advertisement

Community Narratives

BMW cruising ahead with new EVs and premium models to boost revenue 5%

Fair Value €135.07|44.5% undervalued

UN

Community Contributor

EU#2 - From Humble Beginnings to Global Powerhouse

Fair Value DKK 851.04|46.1% undervalued

TO

Community Contributor