Advertisement

China Healthwise Holdings (HKG:348) Has Debt But No Earnings; Should You Worry?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies China Healthwise Holdings Limited (HKG:348) makes use of debt. But is this debt a concern to shareholders?

Why Does Debt Bring Risk?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. In the worst case scenario, a company can go bankrupt if it cannot pay its creditors. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first step when considering a company's debt levels is to consider its cash and debt together.

See our latest analysis for China Healthwise Holdings

What Is China Healthwise Holdings's Debt?

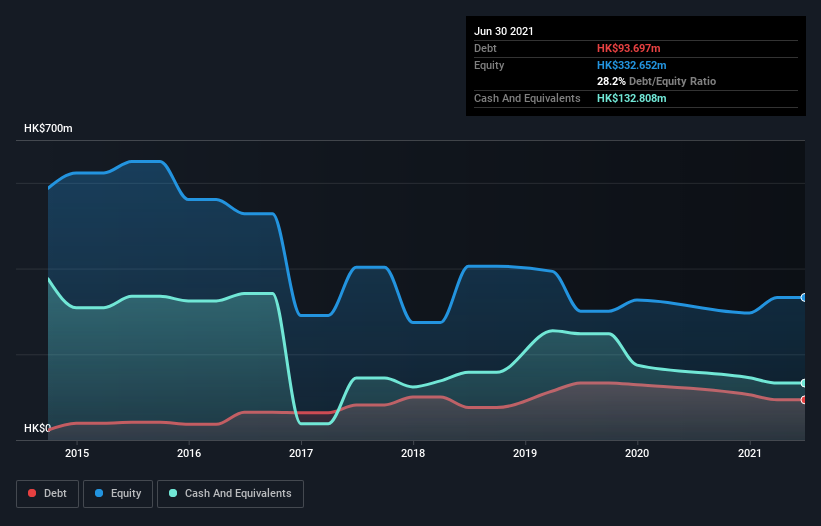

As you can see below, China Healthwise Holdings had HK$93.7m of debt at June 2021, down from HK$128.7m a year prior. But it also has HK$132.8m in cash to offset that, meaning it has HK$39.1m net cash.

How Healthy Is China Healthwise Holdings' Balance Sheet?

According to the last reported balance sheet, China Healthwise Holdings had liabilities of HK$28.8m due within 12 months, and liabilities of HK$88.8m due beyond 12 months. On the other hand, it had cash of HK$132.8m and HK$130.0m worth of receivables due within a year. So it actually has HK$145.3m more liquid assets than total liabilities.

This luscious liquidity implies that China Healthwise Holdings' balance sheet is sturdy like a giant sequoia tree. On this view, lenders should feel as safe as the beloved of a black-belt karate master. Simply put, the fact that China Healthwise Holdings has more cash than debt is arguably a good indication that it can manage its debt safely. There's no doubt that we learn most about debt from the balance sheet. But you can't view debt in total isolation; since China Healthwise Holdings will need earnings to service that debt. So if you're keen to discover more about its earnings, it might be worth checking out this graph of its long term earnings trend.

In the last year China Healthwise Holdings wasn't profitable at an EBIT level, but managed to grow its revenue by 15%, to HK$163m. That rate of growth is a bit slow for our taste, but it takes all types to make a world.

So How Risky Is China Healthwise Holdings?

While China Healthwise Holdings lost money on an earnings before interest and tax (EBIT) level, it actually booked a paper profit of HK$2.2m. So taking that on face value, and considering the cash, we don't think its very risky in the near term. The next few years will be important as the business matures. When analysing debt levels, the balance sheet is the obvious place to start. However, not all investment risk resides within the balance sheet - far from it. We've identified 3 warning signs with China Healthwise Holdings , and understanding them should be part of your investment process.

When all is said and done, sometimes its easier to focus on companies that don't even need debt. Readers can access a list of growth stocks with zero net debt 100% free, right now.

If you're looking for stocks to buy, use the lowest-cost* platform that is rated #1 Overall by Barron’s, Interactive Brokers. Trade stocks, options, futures, forex, bonds and funds on 135 markets, all from a single integrated account. Promoted

New: AI Stock Screener & Alerts

Our new AI Stock Screener scans the market every day to uncover opportunities.

• Dividend Powerhouses (3%+ Yield)

• Undervalued Small Caps with Insider Buying

• High growth Tech and AI Companies

Or build your own from over 50 metrics.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

*Interactive Brokers Rated Lowest Cost Broker by StockBrokers.com Annual Online Review 2020

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

About SEHK:348

China Healthwise Holdings

An investment holding company, engages in the sale of Chinese health products in Hong Kong.

Imperfect balance sheet with very low risk.

Similar Companies

Market Insights

Advertisement

Community Narratives

MINISO's fair value is projected at 26.69 with an anticipated PE ratio shift of 20x

Fair Value US$24.03|12.0% undervalued

BE

Community Contributor

Procter & Gamble: A Dividend Giant Facing Slowing Growth

Fair Value US$119.81|21.7% overvalued

AN

Community Contributor

Eli Lilly's Future Growth Driven by Tirzepatide and Favorable Market Conditions

Fair Value US$1.19k|14.1% undervalued

EA

Community Contributor