Advertisement

- Hong Kong

- /

- Consumer Durables

- /

- SEHK:2127

We Think The Compensation For Huisen Shares Group Limited's (HKG:2127) CEO Looks About Right

Key Insights

- Huisen Shares Group to hold its Annual General Meeting on 31st of May

- Total pay for CEO Runlu Wu includes CN¥840.0k salary

- Total compensation is 61% below industry average

- Huisen Shares Group's EPS declined by 38% over the past three years while total shareholder loss over the past three years was 92%

Performance at Huisen Shares Group Limited (HKG:2127) has been rather uninspiring recently and shareholders may be wondering how CEO Runlu Wu plans to fix this. One way they can exercise their influence on management is through voting on resolutions, such as executive remuneration at the next AGM, coming up on 31st of May. It has been shown that setting appropriate executive remuneration incentivises the management to act in the interests of shareholders. We have prepared some analysis below to show that CEO compensation looks to be reasonable.

Check out our latest analysis for Huisen Shares Group

How Does Total Compensation For Runlu Wu Compare With Other Companies In The Industry?

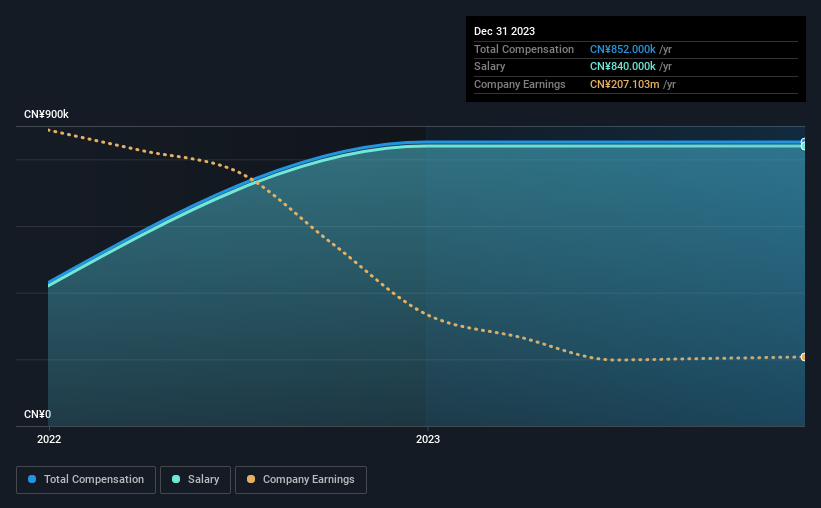

Our data indicates that Huisen Shares Group Limited has a market capitalization of HK$597m, and total annual CEO compensation was reported as CN¥852k for the year to December 2023. This was the same amount the CEO received in the prior year. In particular, the salary of CN¥840.0k, makes up a huge portion of the total compensation being paid to the CEO.

For comparison, other companies in the Hong Kong Consumer Durables industry with market capitalizations below HK$1.6b, reported a median total CEO compensation of CN¥2.2m. In other words, Huisen Shares Group pays its CEO lower than the industry median.

| Component | 2023 | 2022 | Proportion (2023) |

| Salary | CN¥840k | CN¥840k | 99% |

| Other | CN¥12k | CN¥12k | 1% |

| Total Compensation | CN¥852k | CN¥852k | 100% |

On an industry level, around 89% of total compensation represents salary and 11% is other remuneration. Huisen Shares Group has gone down a largely traditional route, paying Runlu Wu a high salary, giving it preference over non-salary benefits. If salary is the major component in total compensation, it suggests that the CEO receives a higher fixed proportion of the total compensation, regardless of performance.

Huisen Shares Group Limited's Growth

Over the last three years, Huisen Shares Group Limited has shrunk its earnings per share by 38% per year. In the last year, its revenue is up 21%.

The reduction in EPS, over three years, is arguably concerning. But in contrast the revenue growth is strong, suggesting future potential for EPS growth. In conclusion we can't form a strong opinion about business performance yet; but it's one worth watching. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has Huisen Shares Group Limited Been A Good Investment?

Few Huisen Shares Group Limited shareholders would feel satisfied with the return of -92% over three years. Therefore, it might be upsetting for shareholders if the CEO were paid generously.

To Conclude...

Runlu receives almost all of their compensation through a salary. The fact that shareholders are sitting on a loss is certainly disheartening. The fact that earnings growth has gone backwards could be a factor for the downward trend in the share price. In the upcoming AGM, shareholders will get the opportunity to discuss these concerns with the board and assess if the board's plan is likely to improve company performance.

CEO pay is simply one of the many factors that need to be considered while examining business performance. We identified 5 warning signs for Huisen Shares Group (2 shouldn't be ignored!) that you should be aware of before investing here.

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Valuation is complex, but we're here to simplify it.

Discover if Huisen Shares Group might be undervalued or overvalued with our detailed analysis, featuring fair value estimates, potential risks, dividends, insider trades, and its financial condition.

Access Free AnalysisHave feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

About SEHK:2127

Huisen Shares Group

Designs, manufactures, develops, and sells furniture products in the United States, the People’s Republic of China, Singapore, Malaysia, Vietnam, Canada, and internationally.

Adequate balance sheet low.

Market Insights

Advertisement

Community Narratives

Groundbreaking therapies that could change the treatment landscape for PTSD, fibromyalgia, MS & Alzheimer’s

Fair Value US$6.20|86.9% undervalued

CM

Community Contributor

DigitalOcean Will Grow 14% by Embracing AI with Paperspace Acquisition

Fair Value US$50.00|41.7% undervalued

NE

Community Contributor

Viant Technology: A Rising AdTech Challenger in the AI-Powered CTV Market

Fair Value US$38.61|63.2% undervalued

BL

Community Contributor

Volvo will Accelerate Forward into Electric and Autonomous Leadership in Five Years

Fair Value SEK 438.80|39.7% undervalued

UN

Community Contributor